Shipping navigates towards transparency amidst rise in alternative fuels

November 20, 2023

The opacity and uncertainty that plagues the maritime industry may finally start to shift thanks to the requirement for Proof of Sustainability (PoS) in alternative fuels. Read More

The shipping sector has come under increased scrutiny due to its environmental impact and lack of transparency in recent years. But it may “finally shift from the opacity (and endemic mistrust) of the past to a more professional, transparent and traceable future,” Integr8 Fuels bunker quality and claims manager Chris Turner writes in the company’s latest bunker quality report.

Need for change

Shipowners are turning to alternative fuels with significantly lower emissions than fossil fuels to reduce the greenhouse gas (GHG) emissions of their vessels. As technology advances, ships may eventually run on fuels with zero-emission potential such as ammonia or methanol.

For now though, biofuels and liquefied natural gas (LNG) are the most promising conventional fuel alternatives to meet upcoming emission intensity-reduction targets in the European Union’s FuelEU Maritime regulation and the International Maritime Organisations’ (IMO) revised GHG strategy. As conventional diesel engines do not require any modifications to run on biofuels, they have a competitive edge over LNG. For biofuel suppliers, however, this power comes with great responsibility.

Encouraging a culture of responsibility

With the EU’s Emissions Trading System including shipping from next year, and with FuelEU Maritime coming into effect from 2025, shipowners will have to report their fleets’ verified emissions to, from and between EU ports. Turner explains that alternative fuel suppliers must show that the bio-components in their fuels are sustainable and provide proof of that to their customers.

“If this is not possible then the alternative fuels, which are generally bought at premiums to conventional fuels, would not be counted in any emissions saving, counting the same as mineral fuels,” he says.

As a result, alternative fuel bunker buyers – especially biofuel consumers – will pay close attention to the feedstocks and well-to-wake emissions associated with these fuels. This is likely to compel suppliers to maintain and encourage transparency and traceability through their product supply chain.

“Of course, not all suppliers will embrace alternative fuels or mandatory mass flow meters (as recently announced in Rotterdam, Antwerp and Brugge ports),” Turner argues, “but those who do will quickly realise their tried and tested practices will be challenged by the end users who will demand they demonstrate and certify sustainability.”

Navigating towards transparency

Documentation will be paramount in the evolving alternative fuels regime, Turner argues.

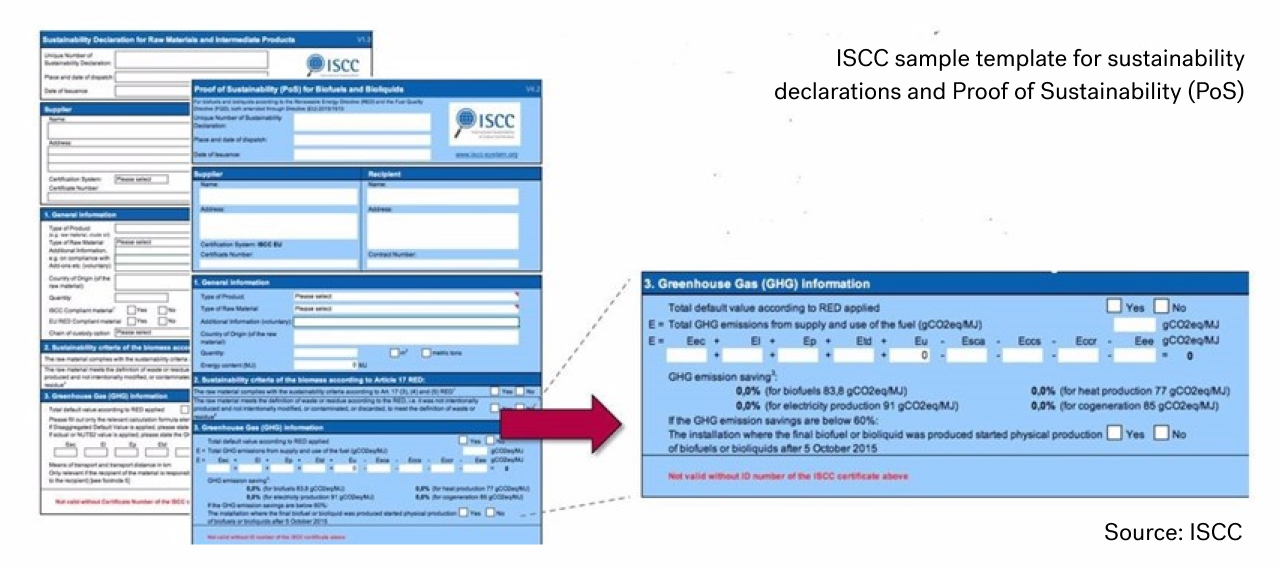

The Bunker Delivery Note (BDN) issued by the marine fuel supplier must include the alternative fuel product and grade. For biofuels, bunker suppliers and operators will have to provide PoS or similar documentation to verify the sustainability of feedstock and energy inputs. The International Sustainability & Carbon Certification (ISCC) is globally recognised as an approved sustainability certificate.

ISCC is a global certification system that sets standards for sustainable production, sourcing and trade of all kinds of bio-based feedstocks and biofuels. A PoS will be passed on throughout the whole supply chain – from initial producer to end consumer. It evaluates the sourcing of raw materials, supply chain management, land use, GHG emissions and social aspects of various companies’ activities.

This could all lead to a “changing of the guard” in the bunker industry, Turner suggests. Stakeholders “from barge deck hand to buyer, and beyond” will need to be retrained to avoid ambiguity on the BDN for the verifier, according to Turner.

Unlike IMO 2020, which was an overnight shift to mostly low-sulphur fuels, the gradual shift to alternative fuels will give suppliers time to realign their efforts to meet evolving industry standards for transparency and sustainability.

Turner discusses this subject, and assesses trends related to biofuels and all conventional grades of marine fuels in the free Bunker Quality Trends Report (Q3-2023).

Press Contact: Angela Freeth

Email: Angela.f@integr8fuels.com

Tel: +44 207 467 5877

Bunker Quality Trends Report Q3 2023

November 7, 2023

Integr8 Fuels’ third bi-annual report analyses data from 120 million metric tons of supply, to reveal key trends relating to fuel quality and availability. In this issue, we add biofuels data into the mix. Read More

Integr8 Fuels’ third bi-annual report analyses data from 120 million metric tons of supply, to reveal key trends relating to fuel quality and availability. In this issue, we add biofuels data into the mix.

This report (first published November 2023) covers the previous six months of supplies globally where we dissect and compare the likelihood of hidden losses and off specification issues across all commercial grades of bunkers and key ports.

Finally, given the context of the incoming changes we will consider some of the challenges that decarbonisation and verification of emissions will bring to the industry.

Topics covered include:

- The supply landscape as it relates to availability and specifications

- Biofuel quality and distribution

- Off-specification trends and problematic parameters

- Geographical variances and “hot spots”

- ISO 8217:2024 and the importance of incorporating new specifications

- MARPOL & SOLAS compliance challenges

- The risk of non-homogenous VLSFO blends and the impact to the end user

- Hidden losses caused by density short lifting

- Considerations when purchasing winter fuel grades

- The impact of new regulations on various elements within the supply chain

Integr8 Fuels launches Brazil office to service an increasingly dynamic South American market

October 26, 2023

Global marine fuel trading company, Integr8 Fuels, has this week opened a new office in Rio de Janeiro, Brazil. Integr8, which previously serviced South America from its US offices, says now is an ideal time to establish a local trading desk as the market is becoming increasingly dynamic following the sale of state-owned refineries in recent years. Read More

Integr8 Fuels has this week opened a new office in Rio de Janeiro, Brazil. Integr8, which previously serviced South America from its US offices, says now is an ideal time to establish a local trading desk as the market is becoming increasingly dynamic following the sale of state-owned refineries in recent years.

Until two years ago, Petrobras owned the largest and almost all other local refineries in Brazil. It was the only physical bunker fuel oil supplier in the country, alongside other players that supplied the market exclusively with Marine Gas Oil (MGO).

The market has since evolved, and a year ago the first non-Petrobras bunker fuel oil delivery was made. Several physical bunker suppliers have made recent entries and brought fresh dynamism, more pricing opportunities and greater delivery flexibility to Brazil’s bunker market.

A more diverse field of fuel producers and bunker suppliers has unlocked new opportunities that buyers in the know stand to benefit from. The types of fuels available has expanded to include most of the top fuel oil and gasoil grades, and a selection of lower-carbon products. These supply chain developments are expected to help Brazilian ports compete with long-established bunkering ports worldwide.

Integr8 Fuels’ new trading desk is led by Lucas Oliveira, a Brazilian industrial engineer with a background in marine sales, trading, fuels distribution, new business development, and the commercial aviation market. With an MBA degree in Oil and Gas Management from Fundação Getulio Vargas and representing the 4th generation in his family to work in shipping, Lucas is excited to witness the latest developments in the sector.

“We are pleased to be closer to our clients in South America, offering on the ground support as they navigate a more complex and vibrant supply chain. With Integr8’s local and international market intelligence and expertise alongside them, clients will be well-supported to make the best of these new opportunities. And as the landscape continues to evolve, we’ll be strengthening both new and existing supplier relationships.” Lucas said.

In addition to providing access to all the main fuel grades, Integr8 continues to establish itself in the alternative fuels space.

“We’re geared up to assist clients in the move to lower carbon options and are strengthening our network coverage of lower carbon fuels such as biofuels and LNG.” Lucas added.

Interested parties are invited to reach out to Lucas directly.

Contact Lucas Costa de Oliveira:

Email: lucas.c@integr8fuels.com

Mobile: +55 (21) 9 7183 1991

Address: Rio de Janeiro/RJ – Brasil, Rua Visconde de Inhaúma, 37 Sala 801 – Centro

Geopolitics have a huge bearing on our market, but something different is happening in HSFO bunker pricing.

October 26, 2023

It is often said that the more dramatic movements in oil prices are usually driven by world events, and that the bunker market is no different to any other part of the crude and products markets. Read More

We are in a global, geopolitical market

It is often said that the more dramatic movements in oil prices are usually driven by world events, and that the bunker market is no different to any other part of the crude and products markets.

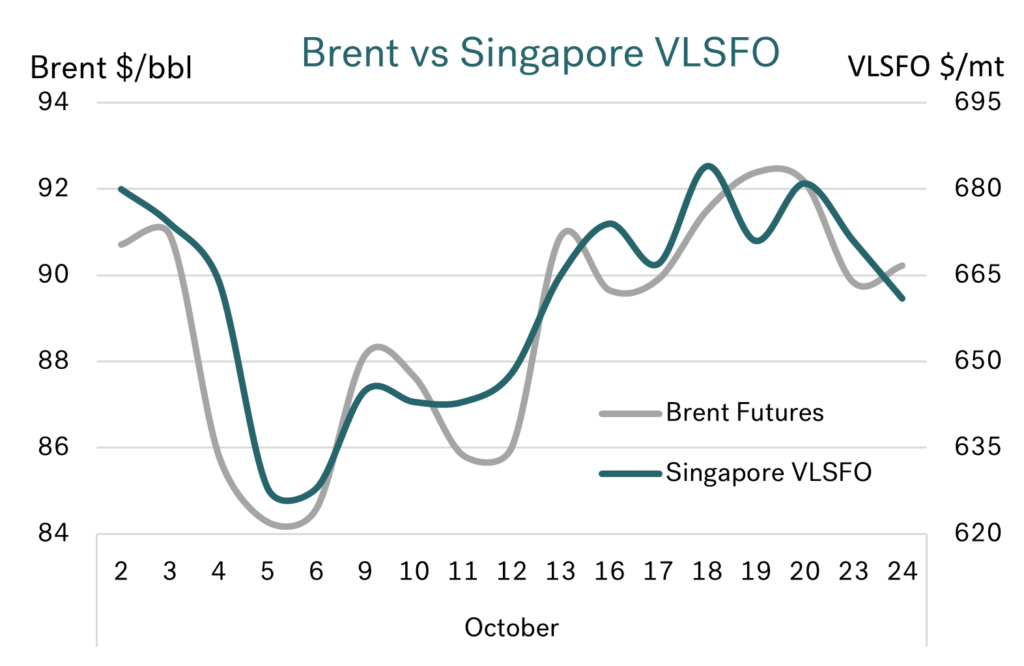

This is exactly what has happened in October. Crude prices were falling in the first week of the month on the back of weaker economic indications for China and Europe. Even though Saudi Arabia and Russia stated they would maintain their voluntary production cutbacks through to the end of the year, this had little impact on the market and oil prices continued their bearish slide.

Over this first week of October Brent futures were down $7/bbl, Singapore VLSFO down $50/mt and Rotterdam VLSFO down by almost $40/mt.

Shortly thereafter, the extreme events in the Middle East took hold. Oil prices rebounded with the news, wiping out the declines seen in the previous week; Brent futures moved back up to the low $90s, Singapore VLSFO returned to around $680/mt, and Rotterdam VLSFO hit $625/mt.

These “down and up” price developments and the close relationship between Brent crude and VLSFO are shown clearly in the chart below.

Source: Integr8 Fuels

Prices have eased at the time of writing, as people wait to see where the Middle East conflict goes and weaker economic indicators out of Europe come to the forefront.

Crude price direction is usually a very good guide for VLSFO

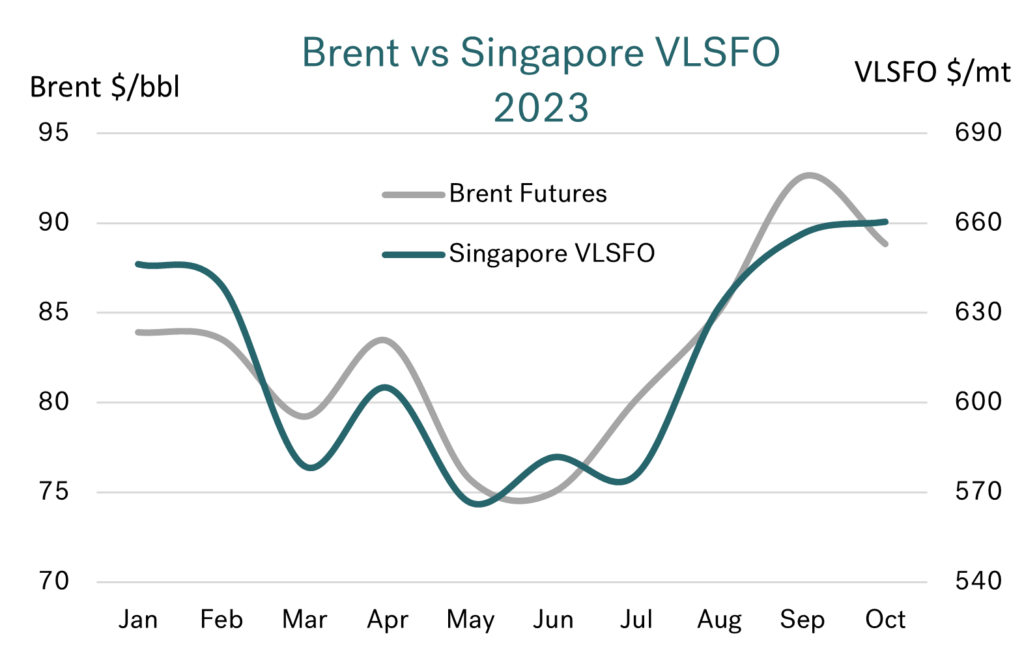

Putting some longer-term context into the Singapore VLSFO versus Brent relationship, the chart below illustrates monthly average price developments for these two commodities so far this year. It shows their very strong correlation and the range in pricing. When Brent crude was around $75/bbl, Singapore VLSFO was close to $575/mt. With recent crude prices rising to their highest levels so far this year and Brent in the low $90s, so monthly average Singapore VLSFO prices are at $660/mt and almost $100/mt above their mid-year lows.

Source: Integr8 Fuels

Source: Integr8 Fuels

In the near term, a lot of the movement in crude oil prices will be linked to what is happening in the Middle East, and so VLSFO price direction will be derived from these events. However, there are still nuances within the bunker market that we continue to monitor, not least the differences between VLSFO and HSFO.

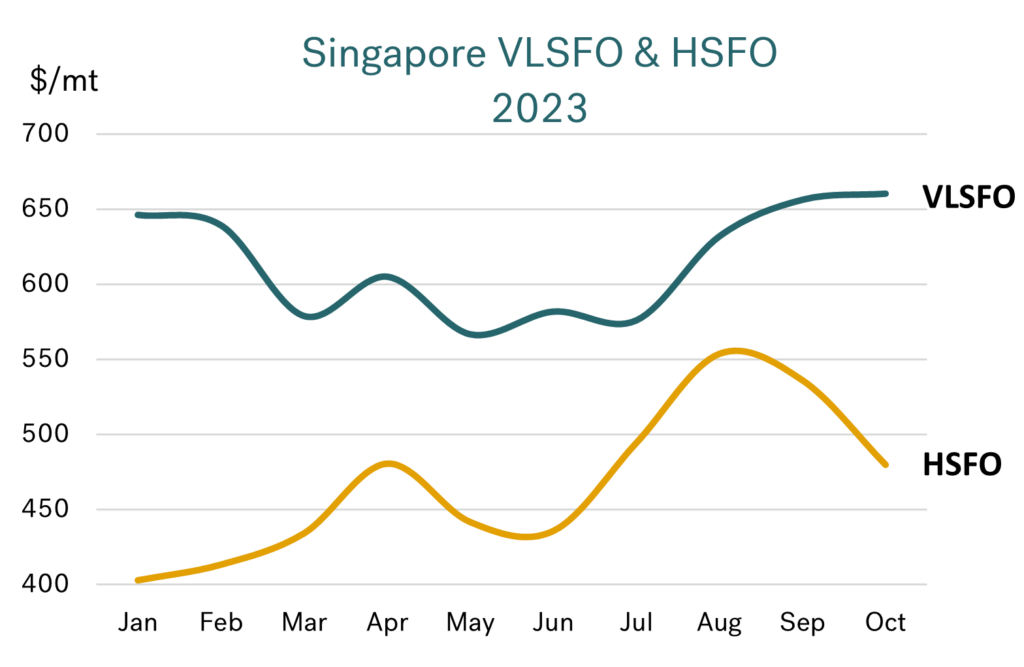

In complete contrast to VLSFO, average prices for HSFO have fallen!

Unlike VLSFO prices closely tracking crude and moving higher over recent months, there has been a turning point in the HSFO market and prices have actually fallen. Whereas monthly average Singapore VLSFO prices are now $30/mt higher than in August, Singapore HSFO prices are $70/mt lower!

Source: Integr8 Fuels

VLSFO and HSFO go in different directions

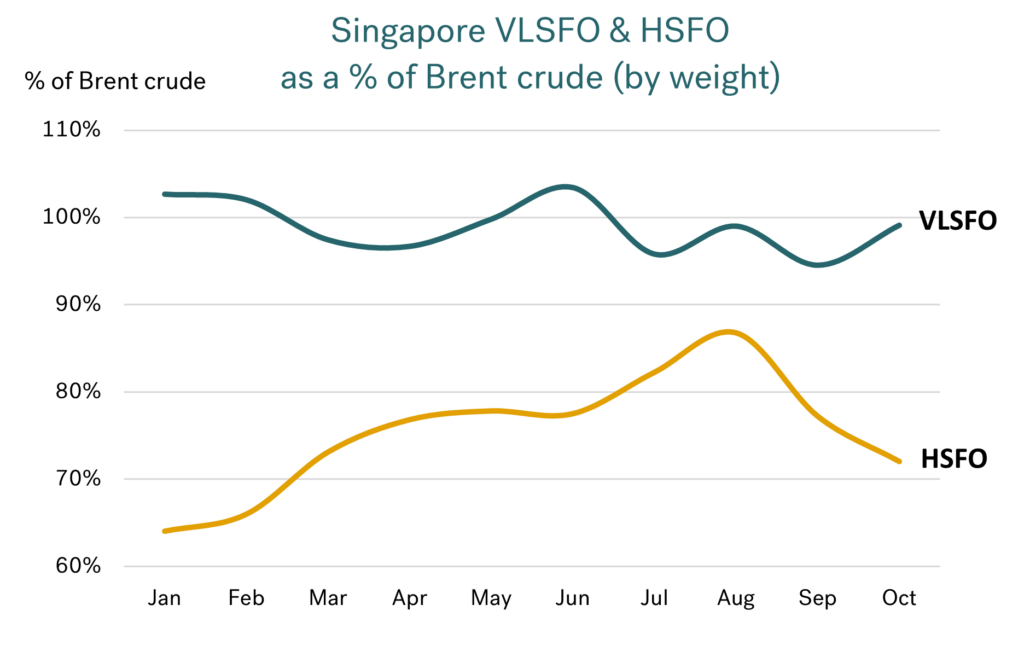

From the initial analysis, Singapore VLSFO closely tracks crude, so it is no surprise that the price relationship between these two are consistent. In fact, Singapore VLSFO is priced at close to 100% of Brent (on a weight basis) and this year has only varied within a very narrow range of 95-103%. If you go back three years, the relationship has been consistently tight and VLSFO has been within the 95-108% range of Brent in all but three months.

Source: Integr8 Fuels

This is in complete contrast to HSFO pricing versus crude. Taking Singapore HSFO as a benchmark, its percentage of Brent shifted from around 65% at the start of the year to close to 80% by mid-year. It is no surprise that the HSFO/Brent relationship strengthened even further in July and August to close to 90%, as Saudi Arabia and Russia made additional, voluntary cuts in crude production/exports totalling 1.5 million b/d (all of which are medium and heavy grades). Consequently, HSFO supply was always going to be squeezed and its relative price likely to rise.

With statements that the Saudi (and Russian) production cuts would run through to the end of this year, it might have been the case that HSFO prices would continue to be supported, at least going into the fourth quarter. This hasn’t happened, and HSFO prices have already fallen sharply despite the Saudi Arabia and Russia strategy and heightened geopolitical risks in the Middle East.

Why has HSFO fallen relative to Brent?

HSFO pricing was always expected to weaken versus Brent, not least in anticipation of the rise in Saudi and Russian crude exports from January. However, the shift has been ‘early’ and the key trigger for the turnaround has centred on the Middle East and a recent substantial increase in HSFO exports.

HSFO is used in a number of power-generating plants in the Middle East and demand is high in the region during the summer months to meet air conditioning demand. As temperatures eased in October, ‘local’ demand for HSFO fell back. Consequently, HSFO exports from the UAE moved from virtually nothing in September, to indications of around 3 million bbls going to Singapore in the middle two weeks of October. On this basis we could expect the seasonal pattern of continued HSFO exports from the UAE until power-generating demand increases again Q2 next year.

In addition to this seasonal shift, there has also been a structural change in HSFO exports from Kuwait. Like the UAE, Kuwait has been burning HSFO in its power generating sector, with supplies coming from their domestic refineries as well as imported volumes. However, with the phased introduction of the massive, 615,000 b/d Al Zour refinery from late last year, it was always planned that the country would switch to using lower sulphur fuel oil as part of its Environmental Fuel Project (EFP). This is now in place and the agreement is for Al Zour to supply up to 225,000 b/d of low-sulphur material to the Kuwait Ministry of Electricity as part of their cleaner energy program.

This has therefore ‘freed-up’ Kuwaiti HSFO for export and also removed them as a buyer of HSFO from the international market on a permanent basis. These ‘additional’ HSFO volumes are moving to Asia and are another contributing factor to a weakening HSFO price.

It all means a widening VLSFO – HSFO price differential

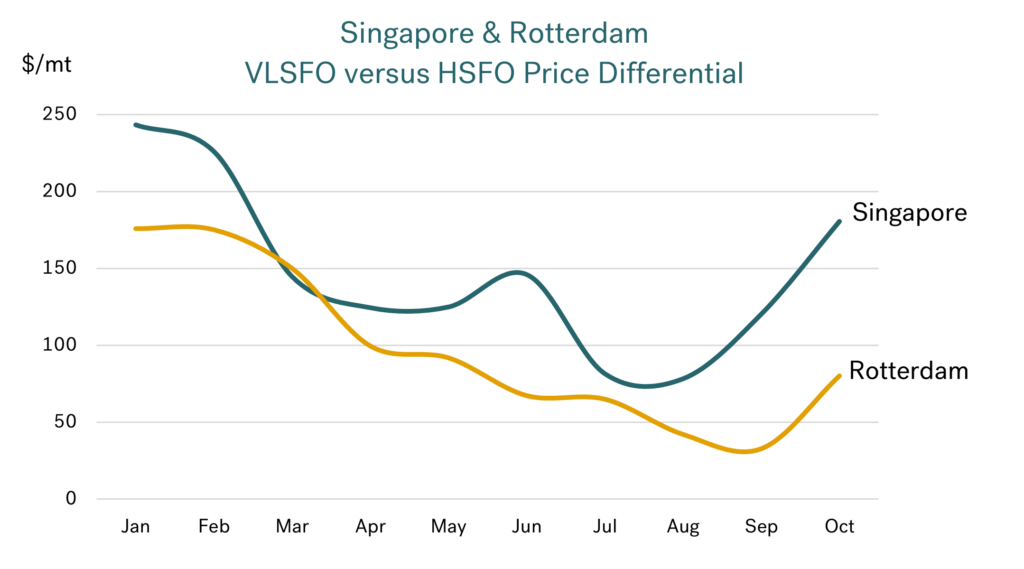

Looking at the VLSFO and HSFO markets, it is clear the price spread between the two products has widened. With ‘incremental’ HSFO volumes available in the Middle East and moving into Singapore, the widening has been greater in these two bunker regions.

This has meant the VLSFO – HSFO spread in Singapore has shifted from an extreme low of only $80/mt in July and August to an average of $180/mt in October. This is still not back to levels seen at the start of this year, but the advantages for scrubber-fitted ships are clearly far better than they have been since March.

Source: Integr8 Fuels

The price spread in Fujairah is very close to the Singapore differential, at around $175/mt in October. However, since the Russian invasion of Ukraine and the resulting ban on Russian products entering Europe (halting a substantial flow of HSFO), the VLSFO – HSFO price spread in Europe has typically been far smaller than in the Middle East and Asia. So, although the spread in Europe has widened, in Rotterdam it has only moved out to $80/mt in October, $100/mt less than in Singapore!

What next?

With the shifts in the HSFO pricing and additional heavier crudes expected to enter the market from the start of next year as Saudi Arabia and Russia remove their voluntary production cutbacks, we can expect ongoing relative downwards pressures on HSFO prices. In the near term, it remains to see what the geopolitical risk is on crude prices, which in turn will largely determine VLSFO pricing. Now the VLSFO – HSFO spread is far more attractive for owners of scrubber-fitted ships in the Middle East and Asia.

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com

Robust regulation and licensing key to ensuring ARA’s mass flow meter mandate is a success

October 24, 2023

On 19 October, the Port of Rotterdam and Antwerp-Bruges Port Authority officially confirmed that Mass Flow Metres (MFM) will become compulsory in Rotterdam, Antwerp and Brugge ports from January 2026. International bunker trading company Integr8 Fuels welcomed the announcement but emphasised that robust regulatory and enforcement protocols will prove critical in order to build confidence in the system. Read More

The initiative is a positive step towards much needed transparency, but scepticism remains without clarification of enforcement protocols.

On 19 October, the Port of Rotterdam and Antwerp-Bruges Port Authority officially confirmed that Mass Flow Metres (MFM) will become compulsory in Rotterdam, Antwerp and Brugge ports from January 2026. International bunker trading company Integr8 Fuels welcomed the announcement but emphasised that robust regulatory and enforcement protocols will prove critical in order to build confidence in the system.

A report from IBIA and BIMCO in May 22 showed that while strong support exists for licencing schemes, mass flow metering, and the transparency this brings between suppliers and receivers, only 80% of those surveyed trusted a correctly installed, certified, and used MFM.

Chris Turner, Bunker Quality & Claims Manager for Integr8 explained “The announcement is great news, but we must also commit to a transparent model strictly aligned to ISO 22192, with the ability to appropriately enforce and sanction. Without this, even with Mass Flow Meters being mandatory in these ports, endemic mistrust will remain, and the opaque nature of supply will persist in the eyes of many.”

Singapore – The Gold Standard

Singapore’s MFM roll-out could serve as a model for the ARA, Chris points out. The best practices achieved in Singapore was a result of an industry-wide initiative and has been underpinned by government support and regulatory enforcement.

Singapore’s approach has been to strive for best practice and deal with poor performance. Its MFM system reduces the chance of manipulation through the following measures:

• A robust Maritime and Port Authority of Singapore approval process

• Application of the SS 524:2021 quality management standard

• Sampling at the vessel manifold

• Traceable calibration

• Consistent documentation

Supported by robust enforcement, the model encourages dispute reporting and performance reviews, with demerit points and possible loss of licenses as penalties for non-compliance.

Licensing Benefits – Improved Compliance

Integr8 data shows that in the last 180 days there were significantly fewer quantity claims in Singapore than the global average (0.9% of Singapore volume vs 1.6% globally).

Chris continued: “Let’s not forget, many of the alternative fuels will be even more expensive, exacerbating potential hidden losses. With carbon taxes and emission trading schemes approaching, it’s even more important for fuel users to have reliable data and the use of MFMs contribute to that.”

Not only do MFMs significantly reduce the likelihood of hidden loses, but the numbers continue to support licenced MFMs when it comes to VLSFO sulphur compliance. Data available to Integr8 shows that Singapore’s system appears to go a long way in lowering the chance of sulphur over 0.50% being reported (a x6 reduction compared to ARA), and allegations of sulphur breaching the carriage ban (also a x6 reduction compared to ARA).

All this suggests that if a commitment is taken to drive the quality systems to the right level, MFMs and licencing can have a significant benefit to disputes, hidden losses and quality issues, including critical MARPOL non-compliance.

“We have a super chance to make a lasting difference in the supply landscape, let’s seize it.” Chris concluded.

Contact Chris Turner:

Email: chris.t@integr8fuels.com

Dubai Tel: +971 4424 0700

Dubai Address: 2901 Silver Tower, Cluster I P.O. Box 214434, Jumeirah Lake Towers, Dubai

Integr8 sees spot LNG bunker demand pick up in evolving market

October 19, 2023

Integr8 Fuels’ LNG desk has recently traded several LNG stems as a volatile market encourages buyers to seek spot deals to manage their price risk. LNG bunkering is typically more complex than bunkering of conventional fuels. It requires a very good understanding of the operational, commercial and contractual aspects of LNG deliveries, and Integr8 has been helping several clients through the purchasing process. Read More

Integr8 Fuels’ LNG desk has recently traded several LNG stems as a volatile market encourages buyers to seek spot deals to manage their price risk.

LNG bunkering is typically more complex than bunkering of conventional fuels. It requires a very good understanding of the operational, commercial and contractual aspects of LNG deliveries, and Integr8 has been helping several clients through the purchasing process.

Volatility spurs spot trading

When strike action was announced by workers at two Chevron LNG plants in Australia, it sent shockwaves through the LNG market in September. While these plants primarily produce LNG for exports to Asian markets, the impact on prices was global and Europe’s benchmark TTF price surged on the news. The market feared global supply disruptions in an interconnected LNG supply chain. And this shows just how sensitive the global supply-demand balance has been to supply disruptions after Russia invaded Ukraine.

Volatile LNG prices are here to stay for the time being, but are expected to come down and stabilise at a lower level after 2025, argues Integr8 Fuels business manager Jonathan Gaylor. “We forget that before Russia’s war with Ukraine, LNG prices were competitive against conventional marine fuels and rather stable,” he says.

LNG was priced below €500/mt in Rotterdam’s bunker market until December 2021, when it had risen gradually for about a year. When Russia invaded Ukraine in late February, it started gathering pace and rose rapidly to new highs. A year later, the price had quintupled and peaked at over €2,500/mt. It had gone from a discount to VLSFO to a three-fold premium, and this discouraged owners of dual-fuel vessels from bunkering LNG. Their fuel flexibility came on display and the market saw widespread gas-to-oil switching.

Rotterdam’s LNG price has since come off sharply. It has dipped below LSMGO and traded at parity with VLSFO. Buyers have subsequently readjusted to take advantage of the renewed pricing opportunities, and oil-to-gas switching has become more prevalent again.

LNG and conventional low-sulphur marine fuels alternate between being at a discount to one another. This discourages terming up supply in contracts and has increasingly turned buyers towards the spot market to manage their price risks and costs on a more predictable near-term basis.

A highly volatile and competitive market presents new opportunities for traders to get involved, particularly as the global LNG-capable fleet is set to more than double from just over 400 vessels now to more than 800 by 2028, according to data from classification society DNV.

Container vessels used to make up the vast majority of vessels bunkering LNG. We have recently seen more dual-fuel tramp vessels bunkering. These typically require greater flexibility in timing and location, especially for tankers. Oil and chemical tankers now make up the biggest LNG-capable vessel type, with 116 vessels in operation and another 85 on order, according to DNV data.

Price references vary between suppliers and geographies. It is quite common to link LNG stem pricing to established wholesale oil and gas benchmarks like TTF, JKM, Henry Hub and Brent to cover some exposure to price swings.

There are longer-term Brent or fuel oil price linkage options for LNG, but they will typically come at a premium for buyers. By locking in the delta on a linked price of a certain percentage, LNG prices will have a partial ceiling based on conventional fuels and buyers can pay down the premiums they paid for investments in dual-fuel engines. The rate of payback on dual-fuel vessels is expected to pick up after 2026 as global LNG supply is set to be boosted by huge new volumes from Qatar and the US, according to multiple industry forecasts.

Challenges remain

LNG stems still require longer time to fix and deliver than conventional ones and this is also probably how things will play out in the foreseeable future. In many cases, compatibility studies between delivering and receiving vessels need to be performed to ensure safe and smooth deliveries.

Integr8 has the knowledge and network to identify competitive suppliers and advice buyers on how best to streamline the bunkering process. Having an overview of and ready access to supply intelligence can certainly help to make the bunker planning and delivery process more efficient for buyers.

Outlook

- Gas prices could easily rise on increased heating demand this winter, but will then likely come down again post winter. Especially if this winter proves that there is sufficient supply in Europe and industrial demand remains subdued.

- The global LNG-fuelled fleet is projected to grow faster than the LNG bunker fleet is expanding. This could lead to undersupply of bunker vessels in 2025-2026, when bunker demand is on track to rise above supply capacity and LNG prices become competitive. It could pose challenges to tramp trading vessels looking for timely LNG spot bunker deliveries.

- Looking further ahead, global gas supply is set to rise with production gains in Qatar and the US. Qatar is in the process of a major expansion of its North Field and two new LNG export terminals. A surge in exports is expected to boost US gas investments and production capacity to new highs over the next decade, with Europe as a key outlet.

Contact the Integr8 Fuels LNG bunker desk:

Email: LNG@integr8fuels.com

Tel: +44 20 7943 5408

Address: Zig Zag Building, 70 Victoria St, London SW1E 6SQ, UK

Bunker prices were high last month; they are even higher today. What is driving prices & how quickly can

they fall?

September 28, 2023

A month ago, we wrote about high bunker prices which were based on two key factors: Tightness in most product markets; And additional oil production cutbacks by Saudi Arabia. Now, bunker prices are even higher. Read More

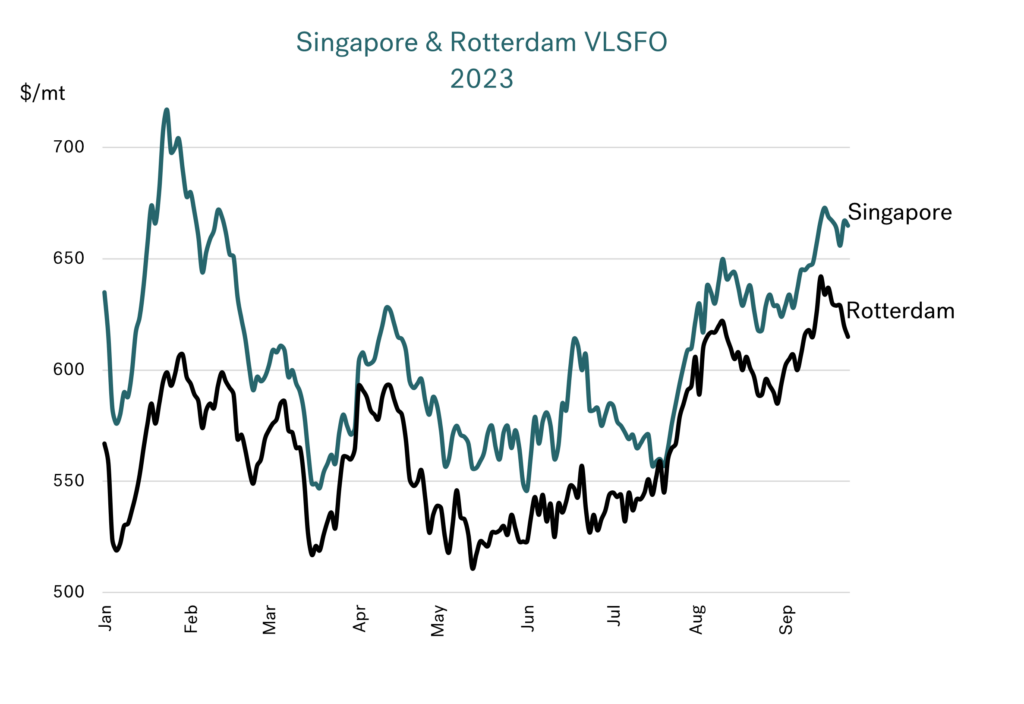

VLSFO prices have been on another rise

A month ago, we wrote about high bunker prices which were based on two key factors: Tightness in most product markets; And additional oil production cutbacks by Saudi Arabia. Now, bunker prices are even higher.

Brent has moved above $90/bbl, with Singapore VLSFO above $660/mt and close to peak levels seen at the start of this year. Rotterdam VLSFO has been trading at around $615-635/mt, its highest so far this year. More recently Rotterdam prices have eased slightly but they are still above this year’s previous peaks, and Singapore prices remain at high levels.

Source: Integr8 Fuels

Much tighter fundamentals are behind the price hike

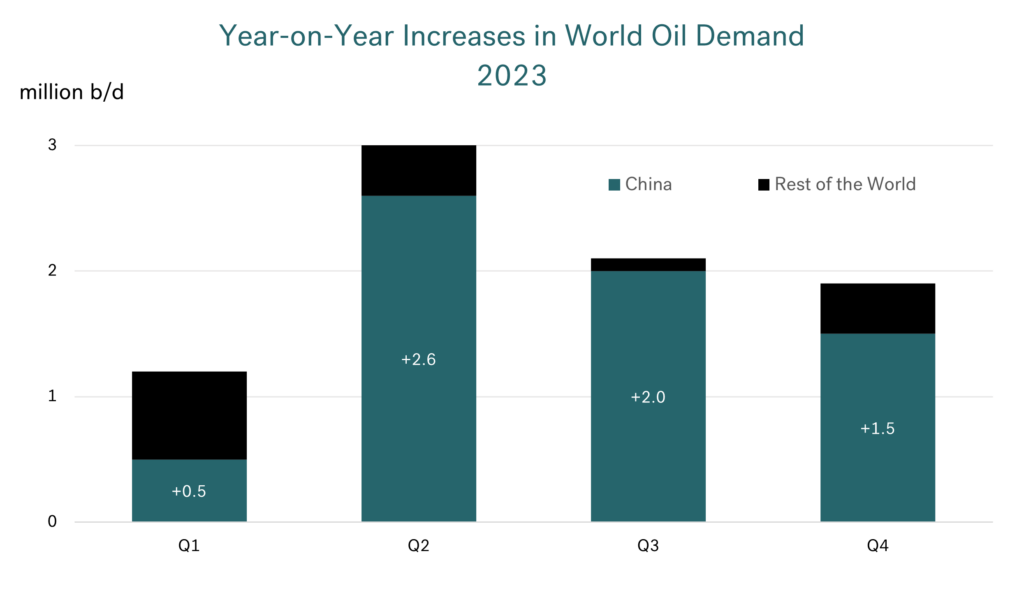

On a very short-term basis, the market can see dramatic price shifts, but it is normally the fundamentals that drive price direction over a period of weeks and months. We are now in a strong fundamental period, with year-on-year growth in global oil demand at 3 million b/d in Q2 this year and projected at 2 million b/d in Q3 and Q4. The key factor here is growth is almost entirely centred on China.

At the same time there are huge constraints in oil supply, with the additional 1 million b/d voluntary cut made by Saudi Arabia, starting in July. In fact, part of the recent price hike is that Saudi Arabia has recently committed to extending these additional cuts through to the end of this year. Additionally, the September 21st announcement by Russia which banned all diesel and gasoline exports to support their own domestic market and, we can see clear reasons why oil prices have taken another leap higher over the past month.

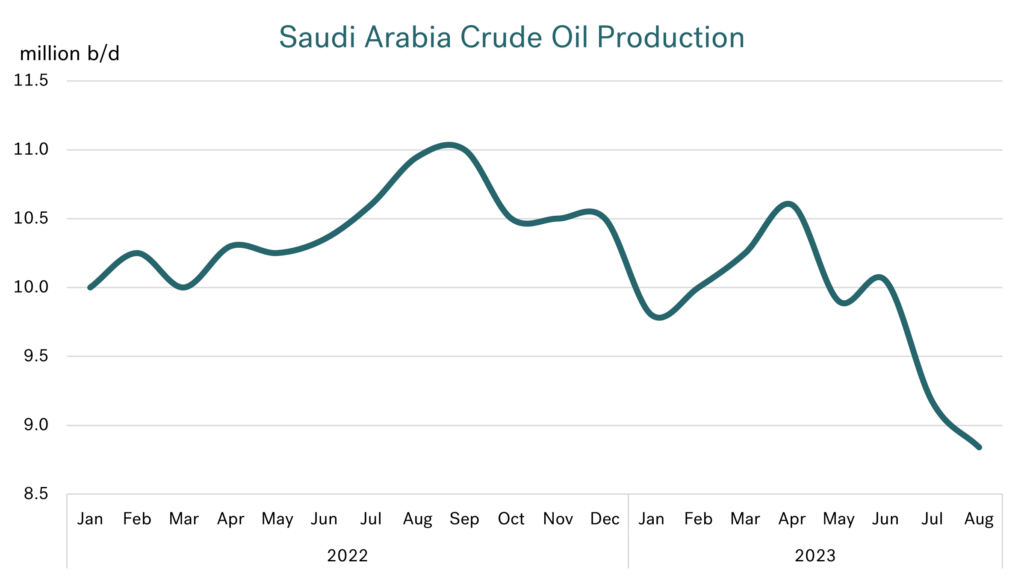

On the supply side, it is what’s happening to Saudi oil production

Saudi Arabia’s stated policy is aimed at supporting a market with less volatility, and more sustainable and predictable outcomes. As part of this strategy, the country had reduced crude output by 0.5 million b/d in line with the overall OPEC+ agreement, and then made a further 1 million b/d cut over the second half of this year. The net result is that Saudi crude production has fallen sharply over the past few months and is currently some 1.5 million b/d lower than average 2022 levels (8.9 million b/d in August vs an average of 10.4 million b/d last year). This lower level of output is expected to be maintained through to the end of the year.

Source: Integr8 Fuels

Source: Integr8 Fuels

Looking at alternative crude supplies, US production crude production is near record highs and higher oil prices has incentivised even greater investment in US shale oil. However, the problem here is Saudi cuts are instantaneous and any rise in US shale production from new investment takes months. Hence, current signals are for a potential tightness in supply over the rest of this year, before an expected 1 million b/d hike in January as Saudi crude output climbs back towards 10 million b/d.

On the demand side it is all about China, China, China

Fundamentals on the demand side also point to higher oil prices. As mentioned, increases in global oil demand are running at 2-3 million b/d (year-on-year), and these are big numbers. However, they are almost entirely based on what is happening in China; product demand developments elsewhere are minimal, and even falling in Europe and projected to start falling in the US next year

The reason for current very high year-on-year growth rates in China is that the country was still largely in lockdown through 2022, and the easing has only taken place this year. This is much later than almost all other countries worldwide, where the post-pandemic ‘boom’ took place in 2022, not 2023. Therefore, it is more-or-less China alone that is driving up oil demand this year.

Source: Integr8 Fuels

Clearly there is a risk of weaker demand than forecast in many countries but if we are looking for a big price impact from the demand side, then it is more likely to be stories about China that are going to drive prices up or down.

Market tightness in Q3 & Q4, but potentially changing going into 2024

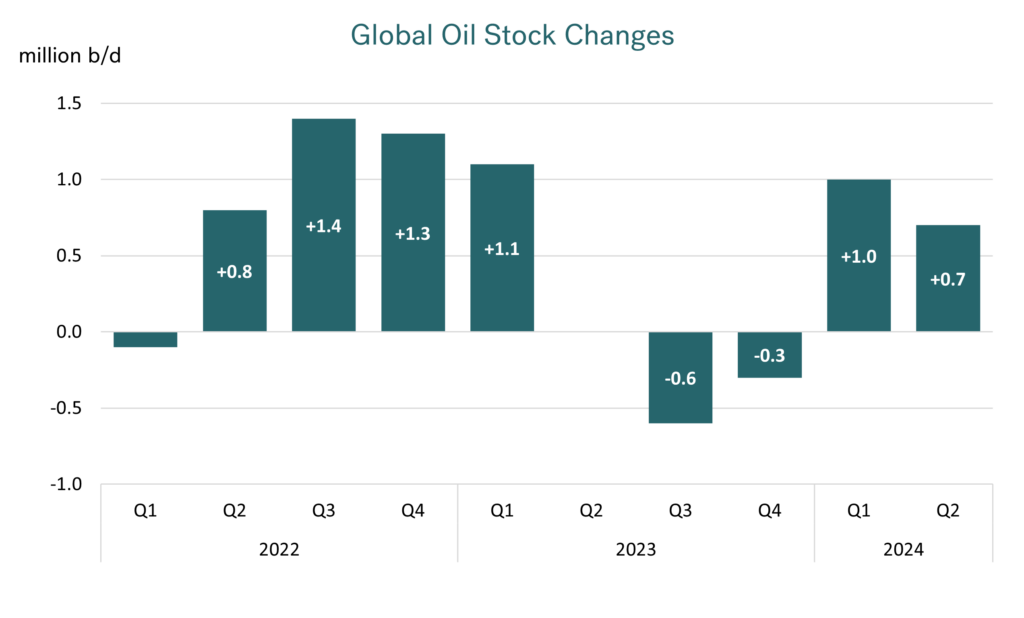

Bringing together these more extreme developments in supply and demand, the graph below illustrates global fundamentals on a quarterly basis. The key for us is that global oil supply exceeded demand through most of 2022 and in the first quarter of this year, resulting in an ongoing global stock build. However, we have just been through a turning point, where demand is exceeding supply in Q3 this year and this is expected to be repeated in Q4, leading to stock draws.

Source: Integr8 Fuels

It is not until the start of next year that we see a reversal and another turning point is envisaged. It is at this stage; Saudi Arabia says it will lift its voluntary 1 million b/d cutbacks. At the same time year-on-year growth in oil demand is expected to ease back to around 1 million b/d. So, at the start of next year oil supply is projected to exceed demand once again, reverting us back to a world of stock builds.

Summarising by looking at the global stock build/stock draw positions, we can see the exceptional times we are currently in; Having moved to a position of stock draws in Q3 and projected for Q4 this year. In addition, the tightness in global stocks lies with oil products, and not crude oil. This has been driven by high product demand and exacerbated by several unplanned refinery outages this year.

Source: Integr8 Fuels

Going into next year the position looks like reversing again, going back to a fundamental global stock build.

What’s next?

Given the fundamentals, these developments explain the wave of price rises we have seen in September.

Looking ahead over the rest of this year and into 2024, on the demand side China is the main story. Of course, Chinese demand could be higher than currently projected, in which case Brent crude could easily pass the $100/bbl ‘barrier’, along with Singapore VLSFO going above $700/mt. However, the chatter at the moment is about weakness in the Chinese economy. If this translates to lower oil demand, then it will be a sign ‘to sell’, and prices for us all would come down. This is clearly the story to watch on the demand side.

The supply side seems more predictable – When Saudi Arabia announces the additional cutbacks will be eased (or there are strong indications of this), then oil prices are likely to fall. A reversal of the Russian ban on diesel and gasoline exports could also have a bearish impact.

Timing is everything in all these developments, and the extent of any fall in prices may still be dependent on how tight oil product stocks are at the time and what stocks look like doing in the near term.

Being precise on price movements is difficult, but we know prices never wait for the fundamentals to be borne out; Markets react on news, changes, and psychology. If the fundamentals do play out as shown in this report, then prices are more likely to fall before the end of the year, in anticipation of weaker fundamentals going into 2024. Let’s see what happens….

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com

If refinery throughput is back up towards record highs, why are refinery margins and bunker prices so high?

August 23, 2023

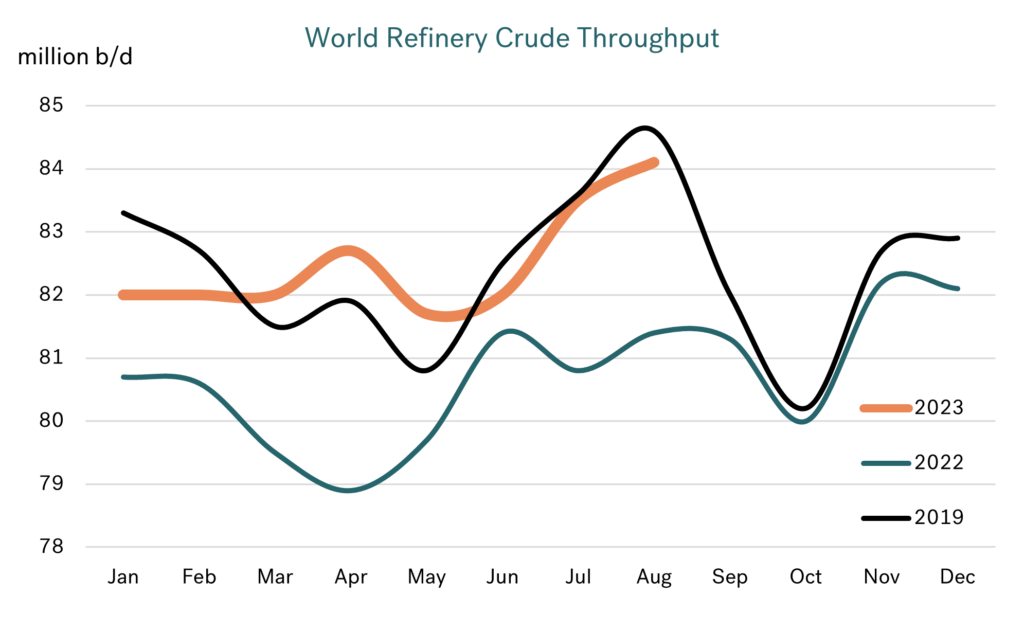

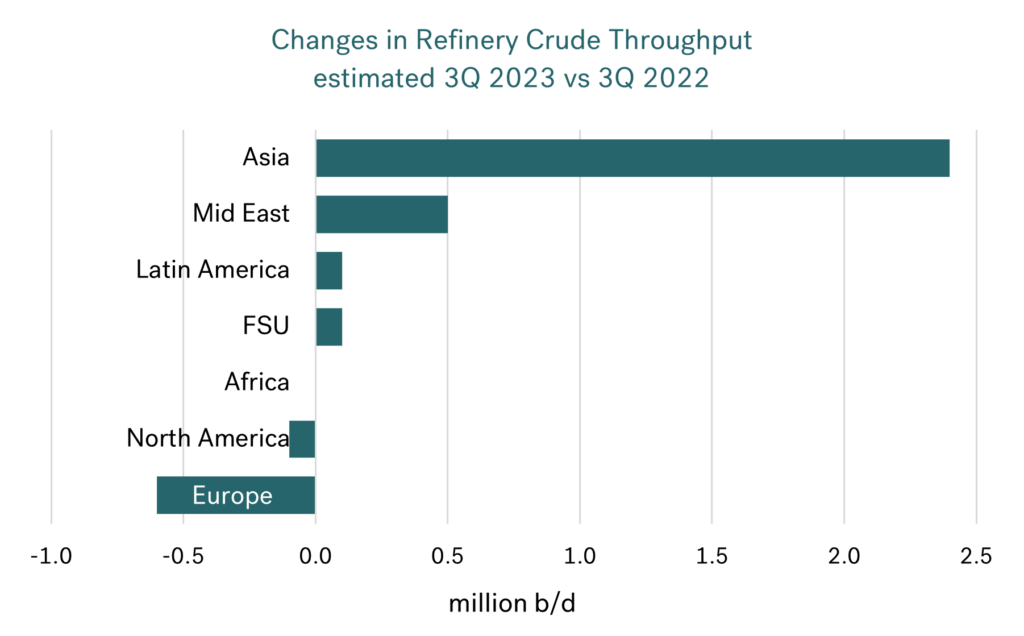

Over the past six months worldwide refinery crude throughputs have finally returned to their pre-pandemic, 2019 levels. The extent of this rise in clearly shown in the graph below, with estimated August crude throughputs at 84 million b/d and around 2.5 million b/d higher than 12 months ago. On the face of it this looks good for product availabilities. Read More

Refinery throughput is finally back to 2019 levels, however…

Over the past six months worldwide refinery crude throughputs have finally returned to their pre-pandemic, 2019 levels. The extent of this rise in clearly shown in the graph below, with estimated August crude throughputs at 84 million b/d and around 2.5 million b/d higher than 12 months ago. On the face of it this looks good for product availabilities.

Source: EIA

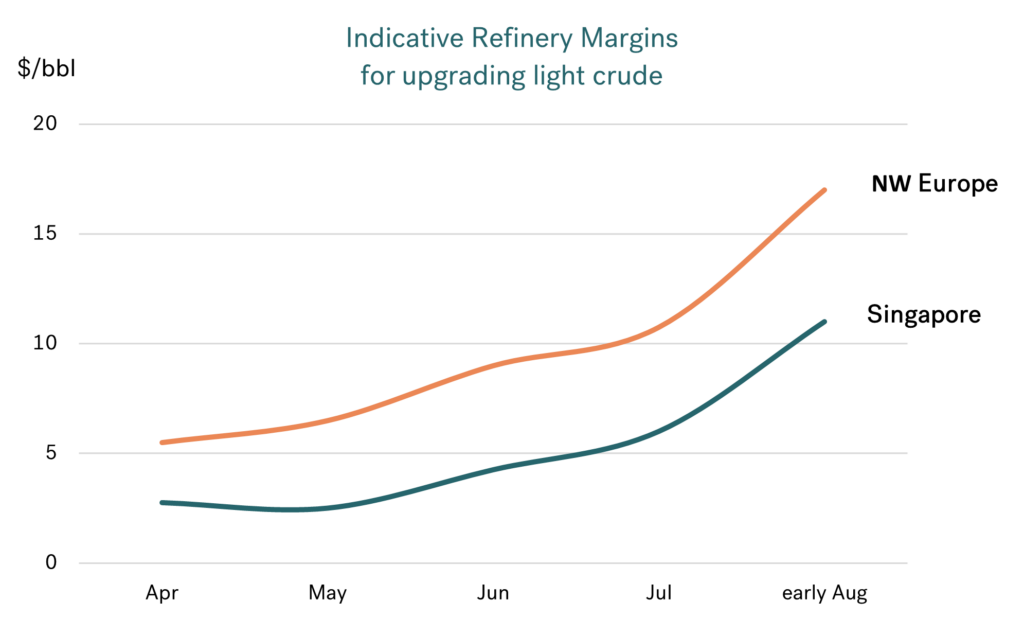

Contradictory position of high refinery runs and high refinery margins

Despite this surge in throughputs to near record highs, most product markets are extremely tight, including those covering the bunker market. The industry is being led by rising demand, with stock levels generally remaining at the low end of historic ranges. This means gasoline is strong, middle distillates are strong, and HSFO is extremely strong. The only product showing weakness is naphtha, which is at the very lighter end of the barrel and some of the reasons for this will become apparent in this report.

This tightness in most product markets is pushing refinery margins much higher and having the knock-on effect of higher bunker prices. The graph below illustrates recent indicative upgrading margins for lighter crude in two key bunkering centers.

Source: Eikon

Source: Eikon

Although not back to the extreme highs around the middle of last year, these margins are strong; up by around $10/bbl, and some 3-4 times greater than back in April. A reasonable conclusion may be that these much bigger margins would drive seasonal refinery crude throughputs considerably higher in both regions, however…

Where is the growth in world refining crude throughput?

As expected, the major gain in refinery throughput has been in Asia, and almost all of this has been in China. New capacity and stronger demand in China have led to an estimated 2 million b/d increase in throughput over the past 12 months.

Similarly, Middle East crude throughputs are also up, again with new capacity coming on stream in Kuwait and Saudi Arabia supporting the increase. Operations in Africa and North America look to be largely unchanged seasonally from last year, with the US EIA suggesting a slight reduction in US crude throughputs.

However, Europe is the outlier, where refinery operations here look to be much lower than 12 months ago, with a drop of more than 0.5 million b/d in crude throughput! This is despite strong refining margins and an apparent attraction to run more crude.

Source: EIA

Why is European refinery throughput down on last year?

The first thing to say is that there have been refinery capacity closures in Europe, but this does not fully explain the drop in throughputs at a time of high margins.

There is typically some operational flexibility in the refining system to shift the type of products supplied, but this is usually very limited. At the same time, most refineries are designed to process specific types of crude, and as a generalisation this tends to be more towards medium and heavier grades.

This is the case in Europe, where the infrastructure is generally designed for medium and heavier crude grades and yet the industry:

- Has ‘lost’ access to Russian (medium) crude because of the ban in place;

- Has seen a reduction in Middle East (heavy) crude imports with the cutbacks in production in that region, which have been even more severe with further cuts by Saudi Arabia in July.

These ‘losses’ have been filled by importing more US crude and running more North Sea grades. However, these ‘new’ crude are much lighter the Russian and Middle East grades they are replacing and as a result European refiners have hit limitations in processing crude.

Ordinarily in these circumstances European refiners may have bought in feedstocks to fill upgrading units, but this has been too challenging with the ban on the Russian feedstock trade to Europe. All-round, the European refining industry is being squeezed and the net result is that crude distillation runs have had to be cut. Therefore, there is an inability in Europe to supply the market with exactly what it needs, even though refining margins are strong!

What does this all mean for bunker prices?

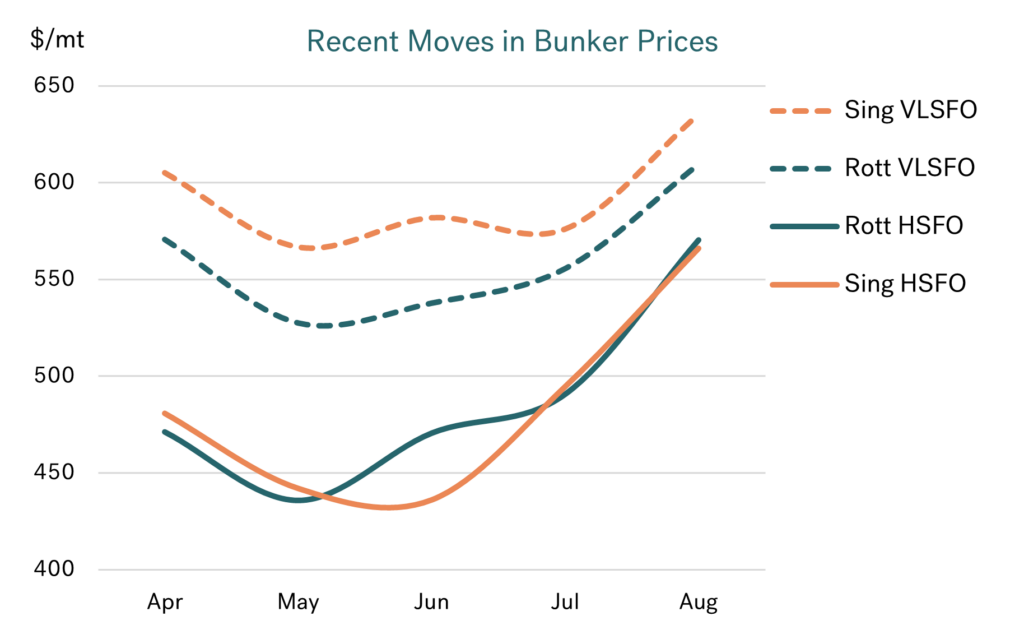

The importance of all of this to us in the bunker market is that pricing for low sulphur fuel oil and VLSFO blending components is relatively strong. However, the upwards pressures in HSFO markets, especially in Europe, are even greater. The enforced shift to a lighter crude slate in the European refining sector has pushed European HSFO margins to a 30 year high!

The graph below illustrates recent developments for VLSFO and HSFO prices in Singapore and Rotterdam, with all prices dipping between May/June but rising since then.

Source: Integr8 Fuels

So far in August, in both regions, average VLSFO prices are around $55/mt higher than in July. Also, whilst Singapore VLSFO prices remain above Rotterdam, this differential has narrowed to only $20-25/mt, showing bigger price increases in the European bunker market.

However, the biggest price increases from July to August have been for HSFO, which are up by $80/mt in Rotterdam and $72/mt in Singapore. Again, the pricing pressures have been greater in Europe, and with this Rotterdam HSFO prices are now at a slight premium to Singapore, which compares with an historic average discount of around $15/mt.

What are the signposts going forward?

Clearly movements in crude prices will have an ‘over-arching’ impact on product pricing across the barrel, and so for prices in our market.

But looking more specifically, the cutbacks in OPEC+ have centred on heavier supplies from the Middle East and so had a global impact on the HSFO market. This has been further exacerbated with Saudi Arabia implementing an additional cutback of close to 1 million b/d in July, and this has now been extended at least through to September. So there does not appear to be any near-term ‘relief’ to the tight global HSFO market conditions. At the same time, it is very difficult (if not impossible) to see the European ban on Russian crude, products and feedstocks being revoked anytime soon. This, along with the OPEC+ cuts, would indicate a continued greater tightness in the European HSFO market.

Let’s see where this takes us over the coming months.

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com

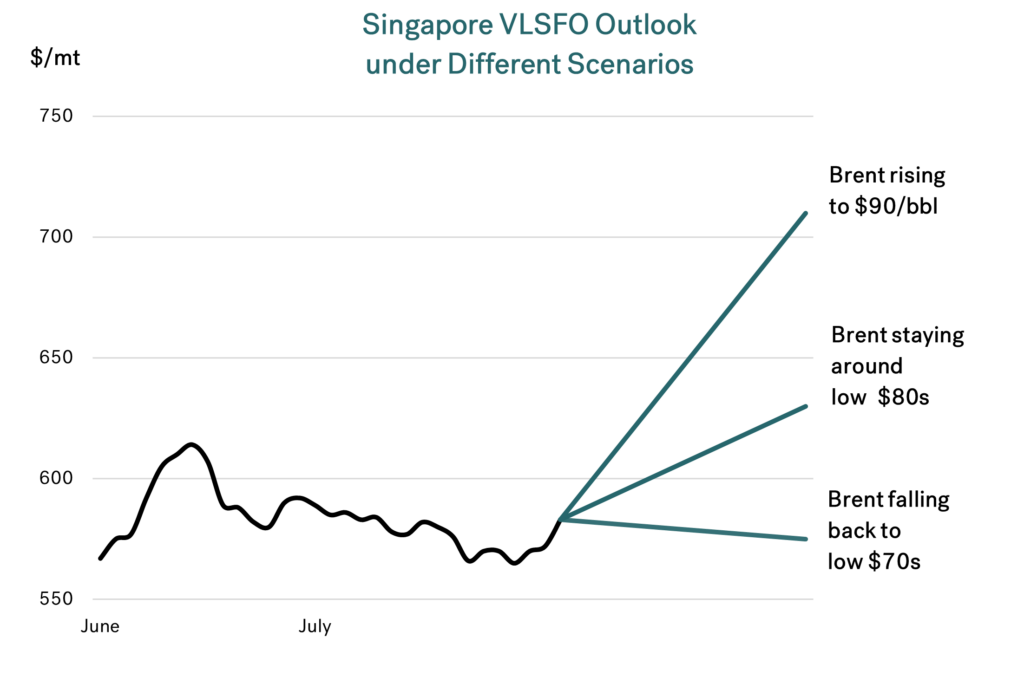

The price is right; but what is happening to VLSFO in Singapore?

July 26, 2023

A big push up on crude oil prices to 3-month highs - Oil prices have seen a strong hike over the past month, with Brent front month futures up by around $10/bbl, to $82/bbl. This is the highest price we have seen for 3 months and has revived the talk and forecasts of higher prices in the second half of this year. Read More

A big push up on crude oil prices to 3-month highs

Oil prices have seen a strong hike over the past month, with Brent front month futures up by around $10/bbl, to $82/bbl. This is the highest price we have seen for 3 months and has revived the talk and forecasts of higher prices in the second half of this year.

Source: Integr8 Fuels

At the same time, heavier, more sour crude grades have strengthened by even more. We are now at a point where Oman is priced at around $1.50/bbl above Brent, when over the first half of this year it averaged a more typical $1.50/bbl below Brent. All of these moves have a heavy influence on bunker prices.

Forecasters have been talking about a price rise for some time

Since the start of this year we have been writing about how forecasters saw a potential rise in oil prices in the second half of the year. These views have been based on combined expectations of strength in oil demand coming from China and constraints in oil supply with cutbacks from OPEC+ (principally Saudi Arabia). Chinese oil demand has risen sharply and is now well above pre-pandemic levels (although there are concerns about the extent of future growth). At the same time OPEC+ has cut production, and these two developments together have pushed crude prices higher.

Crude prices usually drive product prices (although the reverse can also be true) and price direction is typically reflected across the barrel. There are obviously nuances between products, with different drivers impacting different sectors. However, a strong upward price for crude is usually a strong upward price for products.

What about HSFO bunker prices?

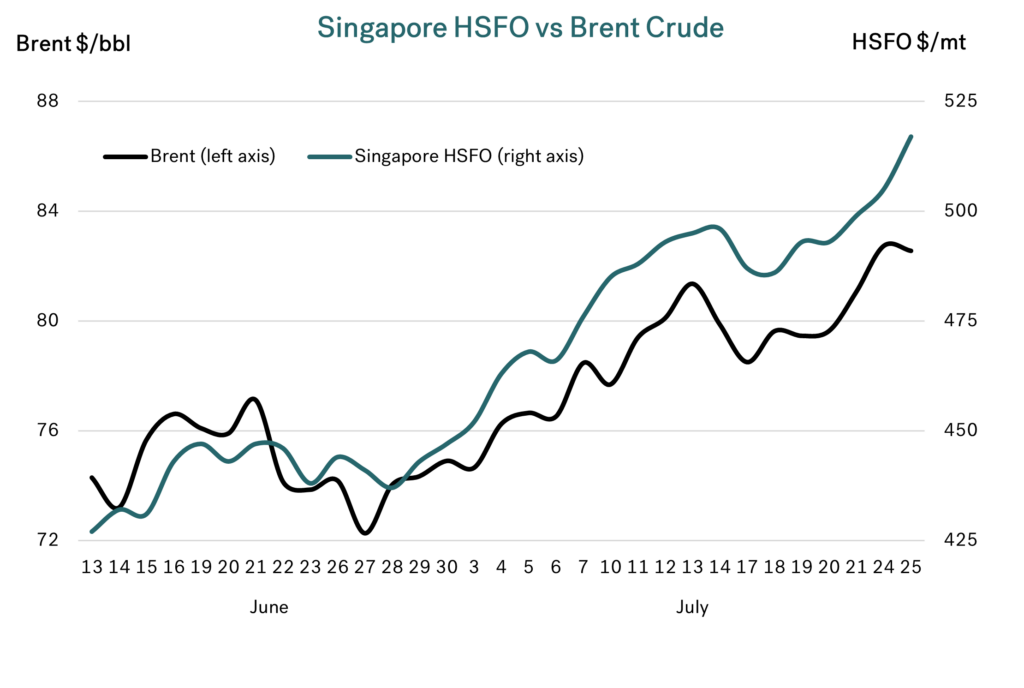

Looking first at Singapore HSFO prices, developments over the past month have been as expected given the rise in crude prices and the moves by OPEC+ (and Saudi Arabia in particular) to cut oil production. Singapore HSFO quotes moved higher as crude prices moved up. However, there has also been a further impact on this market, with fewer HSFO cargoes moving from the Middle East to Asia because of strong local demand for power generation in the Middle East.

In addition, there is the prospect of a fall in high sulphur supplies with further cutbacks in Middle East crude production, which are predominantly heavier and higher sulphur grades. The net result has been an even greater increase in Singapore HSFO prices than in the crude market, and this is clearly shown in the chart below, with the left and right axes scaled the same.

Source: Integr8 Fuels

The current HSFO bunker market in Rotterdam is also broadly in line with crude, although there has been a difference in the timing of price rises.

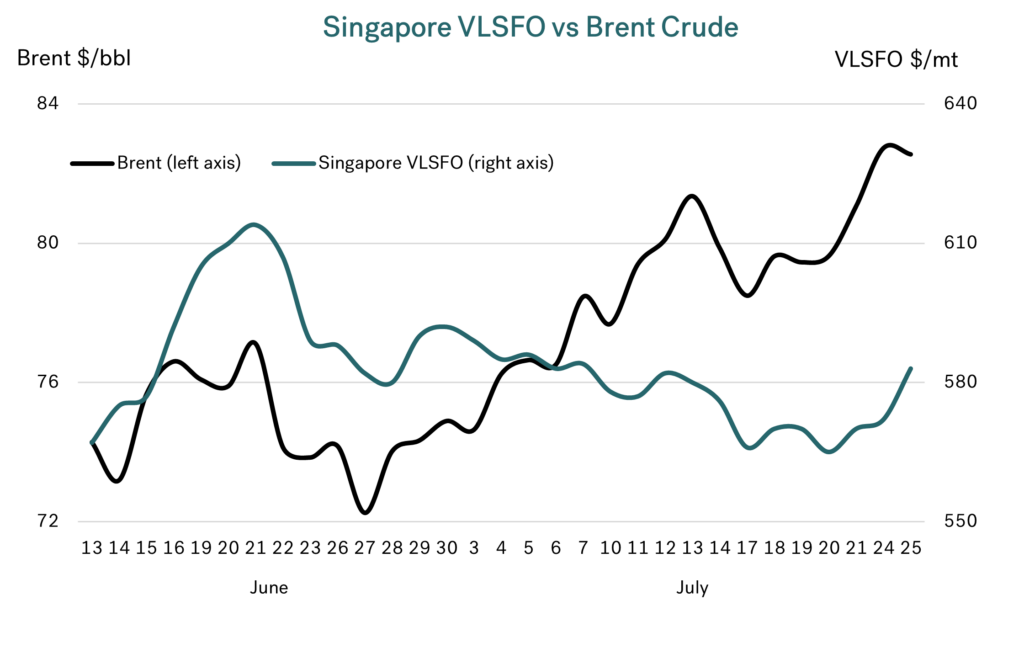

Has VLSFO in Singapore moved in the same way?

This is the focus of the report, and the simple answer is “NO”. In the second half of June, Singapore VLSFO prices rose and fell in line with Brent. However, since the start of July there has been a dramatic divergence in these prices. Singapore VLSFO has gone in the opposite direction to crude and HSFO and has actually fallen! This is contrary to usual expectations, but as the mantra says:

“The price is the price!”

The graph below shows these developments, again with the left and right axes scaled the same.

Source: Integr8 Fuels

The main reason for this Singapore VLSFO price ‘divergence’ is put down to an excess of low sulphur fuel oil in the region. This has come about with the West-East arb being open more recently and so several low sulphur fuel oil cargoes moving from NW Europe to Singapore. On top of this, there is an additional and ongoing low sulphur supply from Kuwait’s relatively new Al-Zour refinery.

This surge in low sulphur supply has been met with limited buying, and as a consequence sellers have been pricing very aggressively on the low side to try to clear this build-up of volumes. Hence, Singapore VLSFO prices have fallen, in sharp contrast to strong rises in crude and HSFO pricing.

What does this mean for Singapore VLSFO pricing in the near term?

These price ‘divergences’ happen, but they are generally temporary, and price relationships do move back towards ‘the norm’ over a period of time. The ‘rebalancing’ will take place with the West-East arb closing and so reducing incoming supplies to Singapore. At the same time, buying interest will pick up, especially if buyers perceive a tighter market and higher prices on the horizon.

This can all happen over a brief period (weeks not months), and there are a number of scenarios that can play out here, including:

1. Brent crude stabilising in the low $80s

In this case Singapore VLSFO prices are likely to catch up with the recent hike in crude prices, and we could see Singapore VLSFO rise by around $50/mt from recent levels, to somewhere around $630/mt.

2. Brent crude falling back to the low $70s

Timings may not be the same as movements in the Singapore VLSFO market, but the main point is we would not expect Singapore VLSFO prices to be significantly lower even if Brent crude does return to the low $70s.

3. Brent crude continuing to rise (to say around $90/bbl)

Here we would not only see Singapore VLSFO prices rise to reflect the recent rise in Brent to $80/bbl, but then see additional bunker price gains as crude takes another step up. Picking $90/bbl as an arbitrary crude number, this would imply Singapore VLSFO rising by more than $100/mt from current levels, to around $700/mt.

Source: Integr8 Fuels

In two of these three cases it suggests Singapore VLSFO prices will rise; it will take a reverse in Brent prices to the low $70s to hold Singapore VLSFO around $580/mt. For VLSFO prices to fall significantly below these levels is likely to need Brent crude to drop into the $60s, which is not what the current OPEC+ strategy is working towards.

As always, forecasting is never straight forward, but having a framework to hang things on and then looking for key indicators can give us a better steer as to where Singapore VLSFO is likely to go.

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com

The IEA has just published its 5-year outlook; What does it mean for the bunker market?

June 28, 2023

The IEA has just published its annual medium-term outlook for the oil industry. This looks five years ahead and covers the fundamental aspects of the industry, from demand and supply to refining and trade, plus a view on the outlook for Brent crude oil prices. Read More

Overview

The IEA has just published its annual medium-term outlook for the oil industry. This looks five years ahead and covers the fundamental aspects of the industry, from demand and supply to refining and trade, plus a view on the outlook for Brent crude oil prices.

In this report, we analyse the key features of the oil market (which will set the underlying price for oil) and specific issues for the bunker sector, including pricing pressures in our sector and the potential overall size of our market; will it continue to grow?

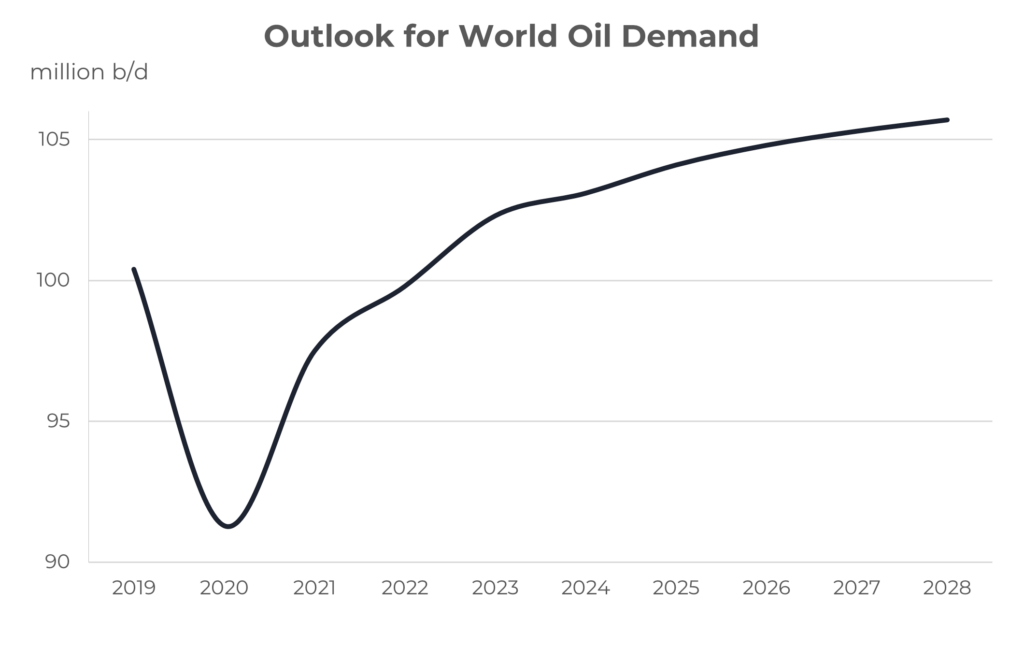

What are the prospects for oil demand in the next 5 years?

The first thing to say is that the IEA sees oil demand continuing to grow throughout the period, but the rate of growth is forecast to slow considerably.

Source: Integr8 Fuels

We are clearly still in the post-pandemic ‘return to normal’, but we are almost there; it is probably only international air travel from China that has to be ‘normalised’, and that will come soon. In this context, world oil demand is forecast to rise by 2.4 million b/d this year. Next year demand is forecast to rise by 0.8 million b/d, and is then projected to slow to only 0.4 million b/d growth by 2028. This slowdown in demand growth is principally down to energy transition to electric vehicles (EVs), with one in seven new car sales last year being EVs. This is only increasing and also being driven by China. However, greater efficiencies in the combustion engine are also a significant contributing factor.

Driving, air travel and shipping activity are all forecast to continue rising, but EVs and more efficient engines mean any increase in oil demand is much lower than otherwise expected. Efficiency is a key word across most sectors, with government backed strategies targeting net zero emissions by 2050. We are clearly involved ourselves through the IMO’s drive to reduce greenhouse gas emissions through the Energy Efficiency Design Index (EEDI) on new ships.

So, by 2028 there is still growth in oil demand, but only just and the writing is on the wall for peak oil demand to be reached sometime soon after this, and then go in to decline.

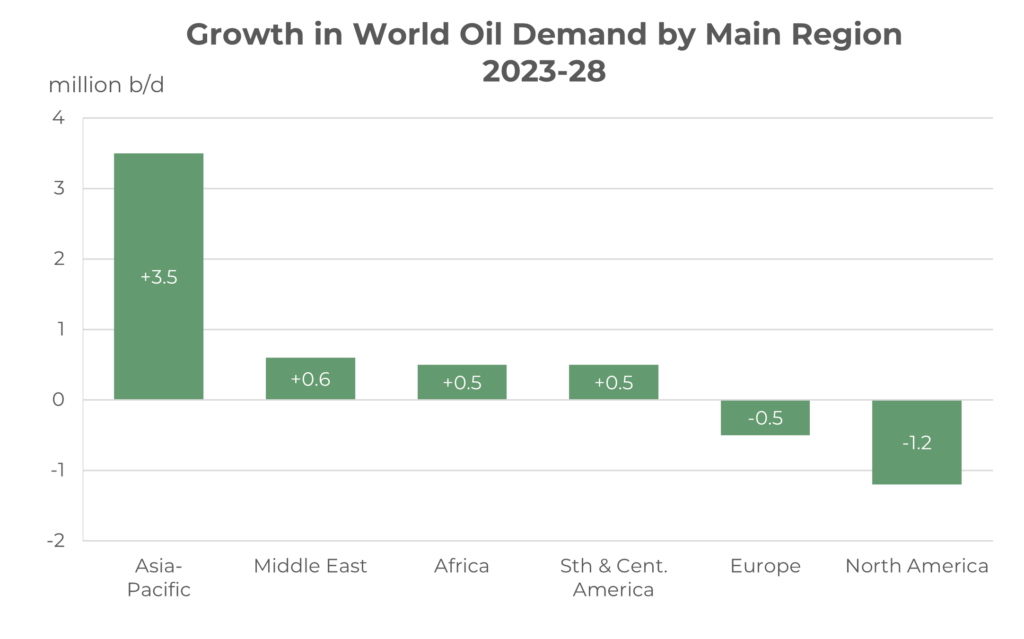

Asia is the focus for demand growth

Simply put, growth in oil demand over the next five years is centered on Asia. China alone accounts for 1.5 million b/d of the growth, followed by India, at 0.8 million b/d; each of these countries is greater than any other entire region.

Source: Integr8 Fuels

It is shifts in the advanced economies of the US and Europe where demand for oil is falling.

Will oil supply be able to match oil demand?

The IEA does include a detailed analysis of future oil supply, with the bottom line that there is enough new oil to meet the expected gains in demand. The key players in additional oil production are the US, Brazil and Guyana in the non-OPEC+ countries, and Saudi Arabia, UAE and Iraq in the OPEC+ countries.

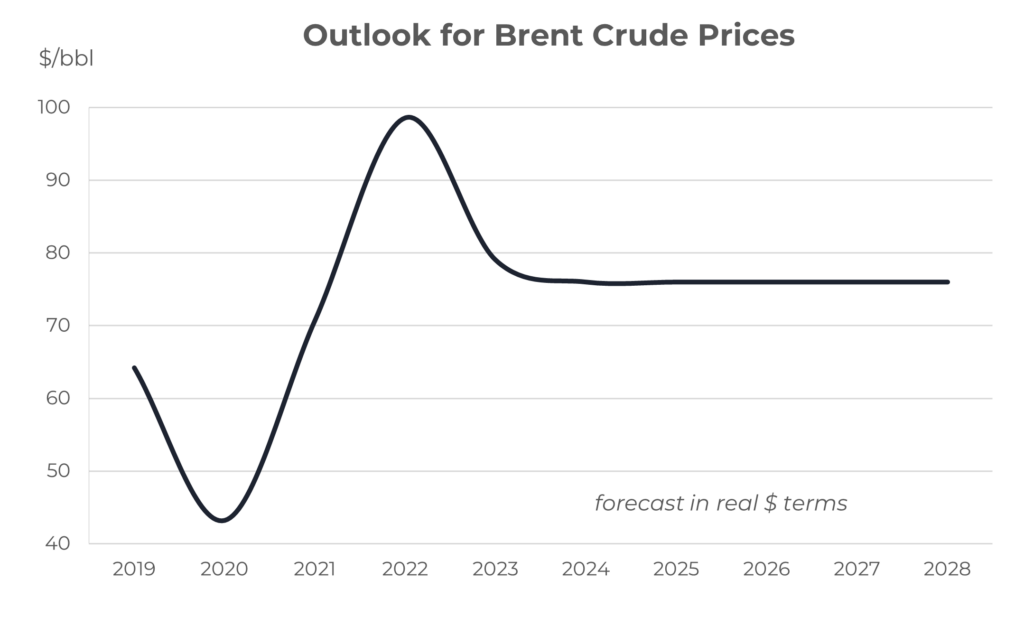

As a base forecast, the IEA envisages spare oil production capacity at close to 4 million b/d throughout the period. This implies no major price hikes in their 5-year outlook, and an underlying Brent price around $76/bbl (in real $ terms) and close to current levels.

Source: Integr8 Fuels

A straight-line forecast may be concerning, but their starting point is that there will be adequate supplies to meet demand. However, there are always major caveats, with the economy a huge variable, OPEC+ strategy a key player and political events potentially damning everything; but you have to start somewhere, and these ‘events’ are largely unforecastable.

What are the products in demand?

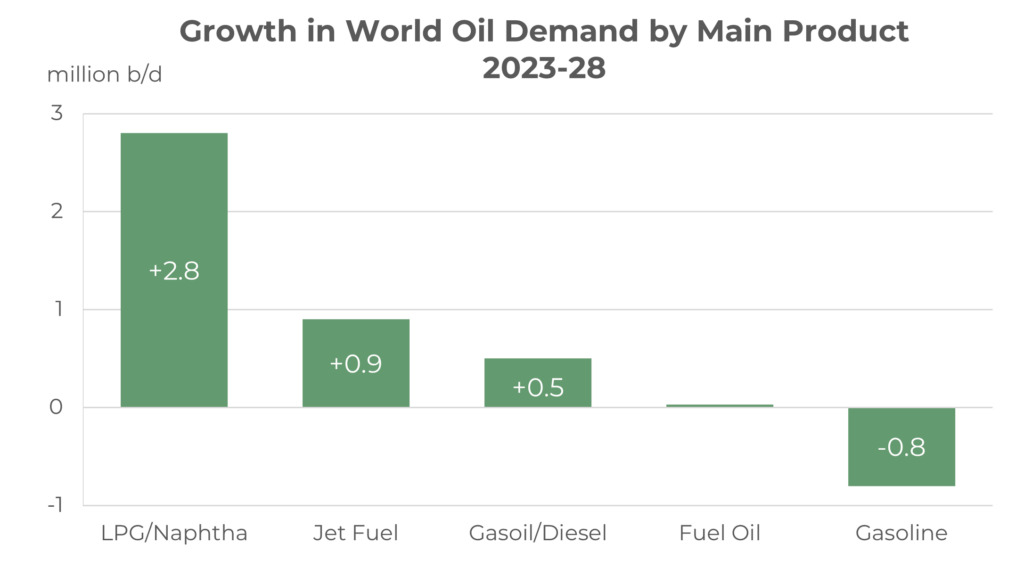

There is always a lot going on in the oil sector, but the backdrop to the IEA’s 5-year forecast is strong growth in demand for petrochemicals (LPG and naphtha) and jet fuel, but declines in the demand for gasoline from now on and declining demand for road transport in general towards the end of the period. Interestingly, the IEA sees demand for bunkers continuing to rise (see below). The magnitude of these changes is clearly seen in the graph below.

Source: Integr8 Fuels

The growth in jet fuel demand (and the smaller gains in gasoil) are crucial features for us in bunkers, as these will have a direct impact on refining balances, leading to pressures on VLSFO supply and pricing.

The nuance for us may not be the absolute price of crude but potential constraints in the refining industry leading to a squeeze on middle distillate supplies and prices. This would push the relative price of VLSFO higher versus crude.

What about the size of the bunker market?

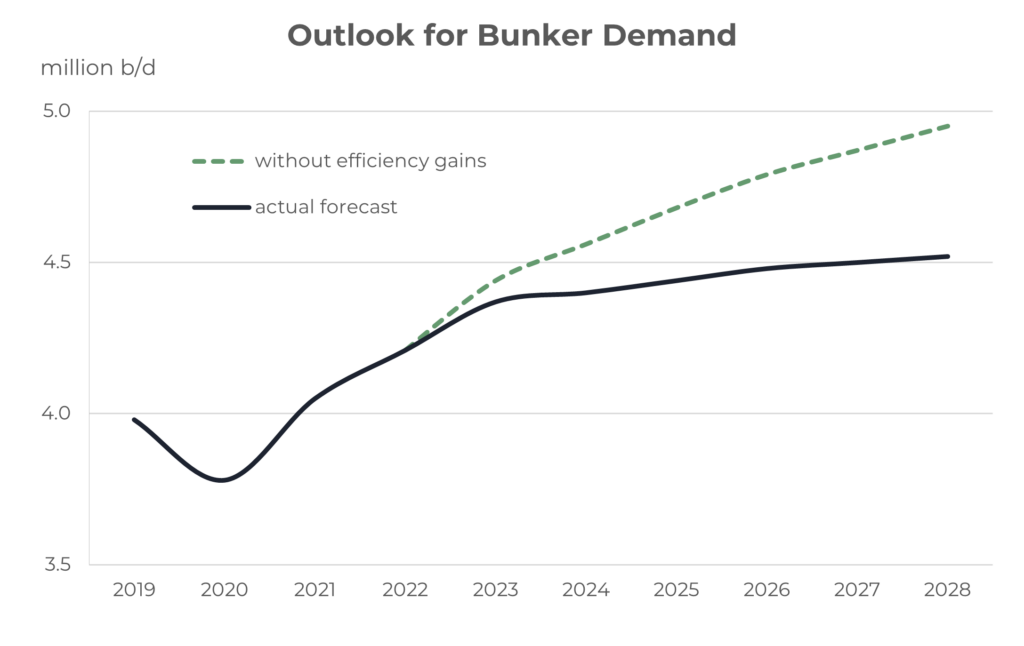

The IEA forecast seaborn trade to increase by 2-3% p.a. over the next 5 years. Ordinarily this would give a strong push on the overall size of our market, up from around 4.4 million b/d this year to around 4.9 million b/d by 2028.

However, like everywhere else, we know there is a huge drive towards greater efficiencies in our industry as part of the commitment towards ‘net zero’. With phases 1 and 2 of the EEDI kicking in during 2015 and 2020, and phase 3 starting in 2025, the shipping fleet is increasingly more efficient. The net result is bunker demand is forecast to rise not by 0.5 million b/d, but by around 0.1 million b/d by 2028. Nonetheless, the size of our market is likely to be relatively stable over the next 5 years (unlike the gasoline market and road diesel markets, which are in decline).

Source: Integr8 Fuels

Source: Integr8 Fuels

What is the outcome for us?

So, for us in the bunker market looking at it day-to-day, or week to week, it is positive, and we may actually see a very slight increase in the amount of activity taking place over the next 5 years. For those planners in our business, we are potentially looking at a ‘decent’ market size in the next 5 years.

Beyond 5 years it is more difficult, with the fleet becoming more efficient over time and talk of alternative fuels. Add to this the likelihood of more environmental legislation and the potential for new technologies (as we have seen in the car sector), and the longer-term bunker market is certainly an interesting one. Based on the latest IEA report, the bunker market looks pretty robust in terms of volumes and, at least as a base case, we are looking at annual average Singapore VLSFO prices at around $600-650/mt over the next 5 years. As always, let’s see what happens!

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com