News Today, 23 hours ago

East of Suez Market Update 18 Apr 2025

Fujairah

Hong Kong

Hualien

Kaohsiung

Keelung

Singapore

Taichung

Zhoushan

HSFO

LSMGO

VLSFO

Prices in East of Suez ports have moved up, and availability of all grades is good in Zhoushan.

Changes on the day, to 17.00 SGT (09.00 GMT) today:

- VLSFO prices up in Zhoushan ($12/mt), Fujairah ($10/mt) and Singapore ($6/mt)

- LSMGO prices up in Fujairah, Zhoushan ($15/mt) and Singapore ($4/mt)

- HSFO prices up in Zhoushan ($10/mt), Singapore ($9/mt) and Fujairah ($6/mt)

- B24-VLSFO at a $252/mt premium over VLSFO in Singapore

- B24-VLSFO at a $245/mt premium over VLSFO in Fujairah

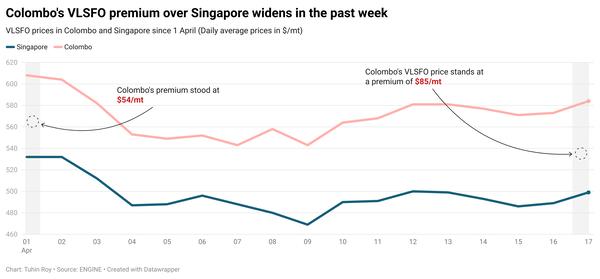

Zhoushan’s VLSFO price has increased by $12/mt over the past day, marking the sharpest rise among the three major Asian bunker ports. Zhoushan's VLSFO now stands at a premium of $28/mt over Fujairah and $17/mt over Singapore.

Availability has improved across all grades in Zhoushan, with most suppliers now recommending lead times of 4–6 days, reduced from the previous 5–7 days.

In Hong Kong, lead times for all fuel grades remain steady at around seven days, unchanged from recent weeks.

In Taiwan, VLSFO and LSMGO supplies remain stable in Hualien and Keelung, with lead times holding steady at around two days, the same as last week. In Kaohsiung and Taichung, deliveries of both grades require lead times of approximately three days.

Brent

The ICE Brent Futures market is closed for trading today on account of Good Friday holiday. Front-month ICE Brent closed at $67.96/bbl on Thursday, which was $1.56/bbl higher than the price at 17.00 SGT (09.00 GMT) on the day.

Upward pressure:

Brent futures traded firm this week, drawing some support from recent geopolitical events that have rattled global markets.

Last week, the Donald Trump-led US government implemented a temporary pause on country-specific tariffs for most trade partners for 90 days. This development eased some demand concerns, with global investors’ focus fixed on trade talks between Washington and its allies.

“Crude oil edged higher on the prospects of a de-escalation in the trade war,” ANZ Bank’s senior commodity strategist Daniel Hynes remarked.

On the supply side, Washington announced stricter sanctions on several companies and vessels responsible for facilitating Iranian oil shipments to China. Brent’s price moved higher following the announcement.

OPEC+ revealed revised compensation plans from seven members yesterday, aiming to make deeper production cuts in the coming months for previous overproduction.

The seven OPEC+ members will collectively cut production by a total of 4.6 million b/d through June 2026, the coalition said.

Downward pressure:

Brent crude felt some downward pressure from easing geopolitical tensions, following a high-level meeting between representatives from the US and Iran last week.

Both parties held "positive" and "constructive" talks in Oman, in an effort to address concerns over Tehran’s advancing nuclear programme, as President Trump warned earlier of a potential military action should negotiations fail to yield a deal, according to Reuters. Iran and the US are set to hold another round of talks in Rome this weekend.

Market analysts suggest that a favourable outcome could prompt Washington to ease its tough sanctions on Tehran’s oil exports, which in turn could put downward pressure on oil prices.

Earlier this week, OPEC released its monthly oil market report, which presented a subdued outlook for global oil demand.

Global oil consumption in 2025 is expected to average 105.05 million b/d, OPEC said. Previously, it expected consumption to average around 105.2 million b/d this year.

Commercial US crude oil inventories gained by 515,000 bbls to touch 443 million bbls for the week ending 11 April, according to data from the US Energy Information Administration (EIA).

A rise in inventories typically signals weaker oil demand, which can put downward pressure on Brent's price.

By Tuhin Roy and Aparupa Mazumder

Please get in touch with comments or additional info to news@engine.online

Provided by

Latest articles from the region

Contact our Experts

With 50+ traders in 12 offices around the world, our team is available 24/7 to support you in your energy procurement needs.