News 2 days ago

East of Suez Market Update 2 Jan 2025

Busan

Daesan

Fujairah

Incheon

Onsan

Singapore

Ulsan

Yeosu

Zhoushan

HSFO

LSMGO

VLSFO

Prices in East of Suez ports have been broadly stable, and bunker demand remains subdued in western South Korean ports such as Daesan.

Changes on the day, to 17.00 SGT (09.00 GMT) today:

- VLSFO prices up in Singapore, Fujairah and Zhoushan ($1/mt)

- LSMGO prices up in Singapore ($2/mt) and Zhoushan ($1/mt), and down in Fujairah ($1/mt)

- HSFO prices up in Zhoushan ($1/mt), and unchanged in Singapore and Fujairah

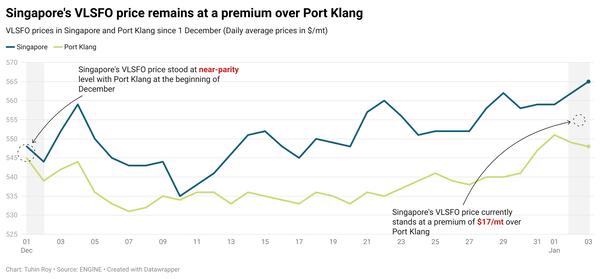

Bunker prices in East of Suez ports have remained largely steady over the past day. In Singapore, VLSFO is priced at a premium of $11/mt to Fujairah and at a discount of $15/mt to Zhoushan.

VLSFO availability in Singapore has improved, with lead times now reduced to 6-9 days from around 10 days last week. HSFO lead times remain unchanged at 10-13 days, while LSMGO lead times vary significantly between 4-14 days.

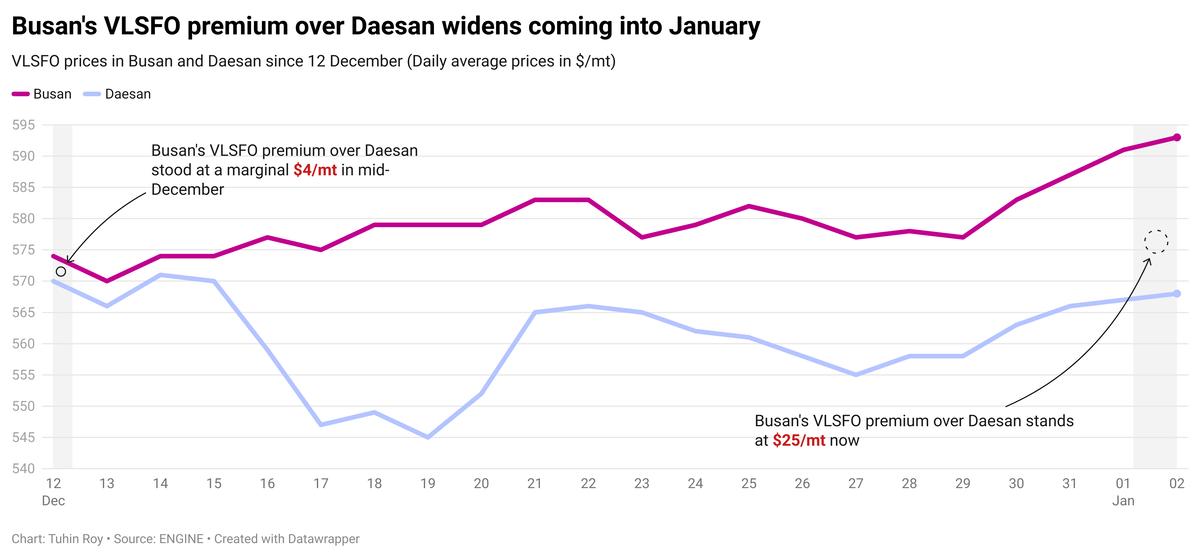

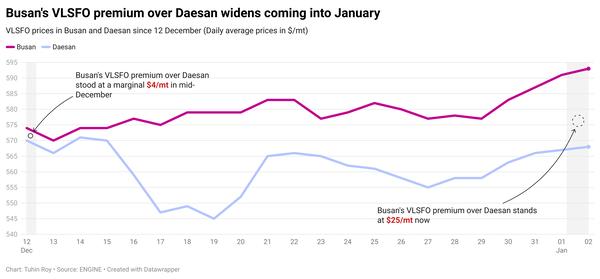

In South Korea, western ports such as Daesan are experiencing weaker demand, prompting suppliers there to offer a discount of around $25/mt on VLSFO compared to the grade's price in southern ports like Busan in order to attract buyers.

In southern South Korean ports, VLSFO and LSMGO lead times range between 4-12 days, remaining nearly unchanged from last week. In western ports, lead times have improved from 6-11 days last week to approximately seven days now. HSFO supply remains steady across South Korea, with most suppliers maintaining lead times of around 6-7 days across all ports.

However, bunker operations at Ulsan, Onsan, and Busan ports are likely to face intermittent disruptions due to potential bad weather from 6-8 January. Similarly, interruptions are expected at Daesan, Taean, and Yeosu ports on Friday and between 6-8 January.

Brent

The front-month ICE Brent contract has gained $0.32/bbl on the day from Tuesday, to trade at $74.92/bbl at 17.00 SGT (09.00 GMT).

Upward pressure:

Brent crude price has risen on the first trading day of 2025, supported by the gradual return of market participants after the Christmas holiday season.

According to SPI Asset Management's managing partner, Stephen Innes, the trajectory of oil prices in 2025 “hinges critically on OPEC+'s next moves."

The Saudi Arabia-led oil producers’ group has sought to prevent a surplus in 2025 by delaying the planned 2.2 million b/d production increases by three more months through March 2025.

Other global factors influencing Brent's price include geopolitical tensions in the Middle East, potential trade tariff hikes and stricter sanctions under Trump 2.0, Innes remarked.

“As we vault into the new year, the oil market is poised on the brink of significant upheaval,” he added.

Downward pressure:

Brent’s price felt some downward pressure as fresh economic data from China missed analysts’ expectations and renewed demand growth concerns in the world’s second-largest oil consumer.

China's manufacturing purchasing managers' index (PMI) came in at 50.1% in December, noting a small decline from 50.3% achieved in November, data from the National Bureau of Statistics (NBS) showed.

A decline in the PMI reading typically indicates a contraction in the manufacturing sector. This also raises concerns about demand growth, which negatively impacts the prices of commodities such as oil.

“China’s official data Tuesday showed December manufacturing Purchasing Managers’ Index at 50.1, missing analyst expectations and softer than November’s 50.3 reading,” VANDA Insights’ founder and analyst Vandana Hari said.

Oil market participants currently await tomorrow’s US December manufacturing data, which will be key for oil price movements, according to analysts.

By Tuhin Roy and Aparupa Mazumder

Please get in touch with comments or additional info to news@engine.online

Provided by

Contact our Experts

With 50+ traders in 12 offices around the world, our team is available 24/7 to support you in your energy procurement needs.