News 31st May, 2023

Europe & Africa Market Update

Amsterdam

Antwerp

Durban

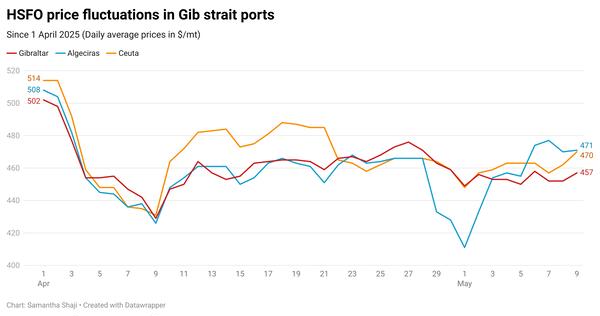

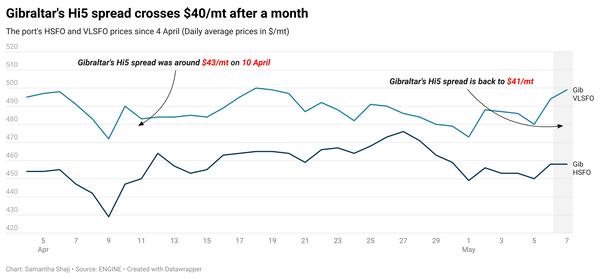

Gibraltar

Rotterdam

HSFO

LSMGO

VLSFO

Regional bunker prices have tracked declining Brent values, and prompt VLSFO supply is tight in the ARA hub amid loading delays.

PHOTO: The Europoort area in the Port of Rotterdam. Getty Images

PHOTO: The Europoort area in the Port of Rotterdam. Getty Images

Changes on the day to 09.00 GMT today:

- VLSFO prices down in Rotterdam ($19/mt), Durban ($8/mt) and Gibraltar ($8/mt)

- LSMGO prices down in Durban ($16/mt), Rotterdam ($15/mt) and Gibraltar ($13/mt)

- HSFO prices down in Gibraltar ($22/mt) and Rotterdam ($8/mt)

Prompt VLSFO supply is said to be tight in the ARA bunkering hub, a source says. Lead times of at least five days are generally recommended to ensure full coverage from suppliers. The source adds that product loading delays at terminals could have contributed to VLSFO tightness in the region. Bunker barges are taking more time than usual to load products.

The downward trend in LSMGO prices in European and African ports have largely mirrored front-month ICE Low Sulphur Gasoil Futures contract, which has dropped by nearly $18/mt in the past day.

LSMGO supply is relatively better in Antwerp and Rotterdam, however, securing prompt deliveries can be difficult in Amsterdam, sources say.

Amsterdam’s LSMGO price has come down by $39/mt in the past day amid downward pressure from a lower-priced 500-1,500 mt stem. A significant drop in the port’s benchmark has contributed to erase its price premium over ICE Low Sulphur Gasoil Futures from yesterday’s $20/mt to near parity levels now.

ICE Low Sulphur Gasoil Futures generally trade at a premium over LSMGO. Its premium over Rotterdam’s LSMGO currently stands at $20/mt.

Congestion has been reduced in Gibraltar, where seven vessels are waiting to bunker today, down from yesterday’s 11 vessels, port agent MH Bland says.

Brent

The front-month ICE Brent contract has dipped further by $2.64/bbl on the day, to $72.95/bbl at 09.00 GMT.

Upward pressure:

Oil markets continue to react to mixed signals from producing nations on another round of output cuts from OPEC+, ahead of the group’s meeting on 4 June.

However, the Russian Deputy Prime Minister has played down the possibility of another production cut.

“It seems Novak’s words have carried more weight in the markets as traders determined that no alignment of thought will mean no deal. That may prove a little naive given the sway that Saudi Arabia holds,” OANDA’s market analyst Craig Erlam said.

On the other hand, the US oil and gas rig count has gone down by 44 this month, the biggest drop since 2020, after energy firms in the US cut rigs for a fourth consecutive week, according to Baker Hughes report.

“The falling rig count in the US suggests that US oil production may have already peaked,” said Phil Flynn, senior account executive of The Price Futures Group.

Downward pressure:

The world’s largest oil importer, China has released a weaker-than-expected economic data, provoking oil markets to worry about a lag in demand recovery.

China’s official manufacturing purchasing managers’ index (PMI) dropped to 48.8 this month, down from 49.2 in April. A reading below 50 indicates contraction.

"The current pessimism surrounding China's commodity (oil) demand stands in contrast to the optimism at the beginning of this year," said Vivek Dhar, director of commodities research at the Commonwealth Bank of Australia.

Additionally, concerns about a second COVID wave in China and a potential increase in interest rate by the US Federal Reserve continue to weigh on Brent futures.

By Nithin Chandran and Aparupa Mazumder

Please get in touch with comments or additional info to news@engine.online

Provided by

Latest articles from the region

Contact our Experts

With 50+ traders in 12 offices around the world, our team is available 24/7 to support you in your energy procurement needs.