News May 7, 2026

Familiar Patterns Emerging: How Market Volatility May Shape Bunker Quality

Tighter oil markets are starting to show in bunker fuel quality. Early sample data is moving, and published statistics are still catching up.

Marine fuel quality is often treated as a technical issue, but it is also a market signal. Bunker fuel sits at the end of a long and pressured chain: crude selection, refinery configuration, storage logistics, cutter stock economics, barge availability, and regulatory change. When that chain is disturbed, whether through planned regulation or sudden market disruption, the impact is not limited to price. It can also show up in the fuel itself: density, metals, ash, sediment, stability, sulphur margin, and unusual blend components.

I have written about this theme before. In my latest Bunker Quality Trends Report, I argued that quality data should not be viewed solely as a pass-or-fail exercise against specification. It can also provide insight into how the fuel pool is shifting. Upward trends in metals, pour point, ash, or density may not render a fuel unsuitable, but they can still point to changes in crude slate, refinery streams, or blending practice.

The warning signs that preceded previous bunker quality events are visible again. Not as a confirmed repeat of Houston in 2018 or Singapore in 2022, but as early movement in the data before the wider market has fully priced in the risk.

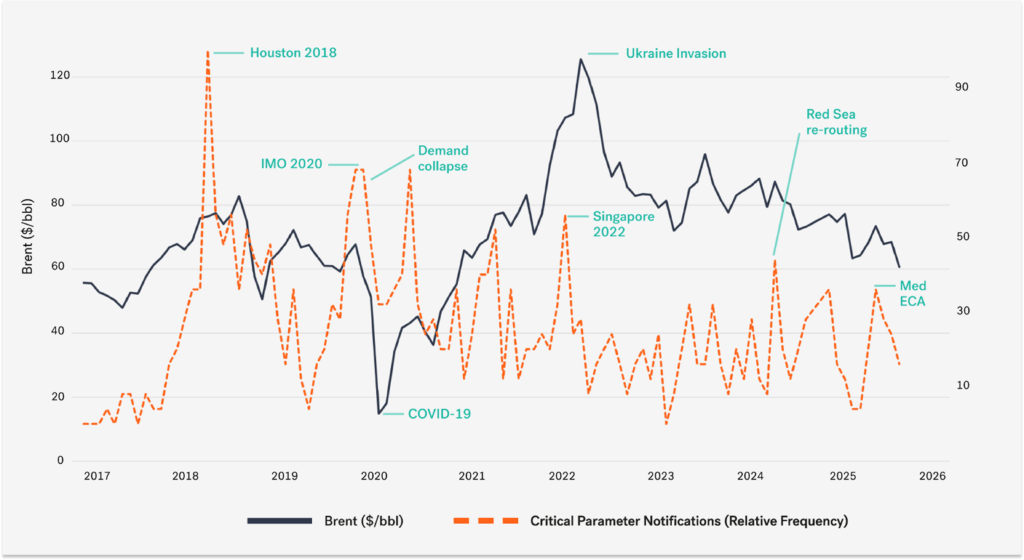

Figure 1: Historical timeline tracking Brent prices alongside critical parameter notifications, relative to frequency. (Integr8 Fuels)

The pattern started with what became known across the industry as the Houston problem in 2018. This served as a modern reminder that bunker quality risk can sit outside the normal specification tables. It was not an isolated supplier failure, but a wider blending pool issue that affected fuel moving through multiple suppliers across the region.

In a rising market, blenders appeared to have pushed the envelope. Cheaper and less familiar cutter stocks entered the pool, while very little GCMS testing was being carried out as part of routine quality control. Affected fuels were later associated with phenolic compounds and fatty acids, which in many cases correlated with elevated Total Acid Number. Vessels reported fuel pump, fuel system and engine-related problems.

The lesson was clear: routine ISO 8217 testing was essential, but it did not always tell the whole story.

IMO 2020 & COVID-19

IMO 2020 then showed that quality pressure does not need to come from a surprise incident. It can also come from a planned transition. The move from High Sulphur Fuel Oil (HSFO) to Very Low Sulphur Fuel Oil (VLSFO) pushed the global bunker market through one of the largest blending shifts it had ever seen. Refiners, suppliers, terminals, barges and ship operators all had to adjust within a compressed timeframe.

New VLSFO blends entered the market at scale, with different aromatic and paraffinic balances, as well as distinct stability behaviour and handling characteristics. Cross-contamination, compatibility concerns, purifier loading, and sediment control all became live operational issues.

This was not simply a failure of planning. It was the natural stress created when the entire fuel pool changes direction at speed.

COVID-19 brought a very different type of shock. The collapse in transport demand changed refinery economics almost overnight. Gasoline demand weakened during what would normally have been the driving season, aviation demand collapsed, and refiners were left with intermediate streams, including Vacuum Gas Oil (VGO), that no longer had their usual economic outlets.

With fewer routes into conventional transport fuel demand, some of this material found its way into the bunker blending pool. The quality signal was not a single global contamination event. It was more subtle, with increased attention on paraffinic content, cold flow behaviour, stability, and the use of components that may not have been as prominent under normal demand conditions.

Again, the fuel reflected the market around it.

2022 Singapore HSFO Contamination

The Singapore HSFO contamination case in 2022 reinforced the same lesson. The fuel affected was not a straightforward specification failure. It contained high levels of chlorinated organic compounds, including 1,2 dichloroethane and tetrachloroethylene, and was later traced by the Maritime and Port Authority of Singapore to fuel loaded at Khor Fakkan, before being shipped for further blending and delivered into Singapore. Around 200 ships received this fuel, and roughly 80 of those 200 ships reported fuel pump and engine-related issues.

This occurred during a period of extreme market volatility following the invasion of Ukraine, when crude flows, product flows, and blending economics were under pressure.

The point was not that the war directly caused the contamination. Rather, stressed markets created conditions in which unusual intermediate streams could enter the bunker pool, often outside the reach of routine specification testing.

Disruption in the Red Sea & Bab el Mandab

The Red Sea and Bab el Mandab disruption brought a different type of pressure. This was not primarily a contamination story; it was a logistics story. The Houthi threat forced diversions around the Cape of Good Hope, increasing voyage distances, vessel speeds, bunker consumption, and pressure on strategic refuelling hubs. As noted previously in 2025, this pressure affected quality, particularly where tighter barge utilisation was a factor. This resulted in faster grade switching and reduced segregation margins, increasing the risk of cross-contamination, including VLSFO sulphur exceedances in certain locations.

The January 2025 sanctions added another layer of pressure by changing which barrels could move, where they could move, and who could handle them. Russian fuel oil, VGO, and related blend components had been part of the global balancing system. As these flows became harder for mainstream buyers, traders, insurers, and shipowners to access, the market had to replace them quickly.

In the early phase, this meant greater reliance on alternative residual streams, including heavier, metal-rich Middle East fuel oil barrels. This changed the fingerprint of the blend pool, particularly in terms of metals, ash, density, and stability characteristics.

As discussed in the latest edition of our Bunker Quality Trends Report the quality impact was not a single headline contamination case, but a broader drift in the residual fuel pool as replacement barrels worked their way into key bunker hubs.

The current market is now showing a similar set of pressures.

Integr8 Fuels’ expert contributor, Steve Christy’s recent article framed the oil market as moving from surplus to shortage. That is also the right starting point for the quality discussion. The Strait of Hormuz shock has not only lifted prices; it has changed the shape of the market. A previously comfortable balance has tightened, with supply risk, stock draws, and war premium now sitting at the centre of the outlook. Bunker prices moved first. Fuel quality may be next.

The first reaction was price. Asian bunkers carried a heavy premium when the Strait of Hormuz risk escalated, before that premium started to unwind as crude and product flows adjusted.

The more important point for quality is what happens beneath the surface. Asian refiners competed more aggressively for Atlantic Basin crude, including South American and U.S. barrels. Atlantic markets tightened, Asian markets eased, and the refining system began to rebalance around a

new constraint.

That is the type of movement that can alter the residual fuel pool before anything formally falls outside specification.

Drawing on Integr8’s sample base of around 130 million tonnes of quality data per annum, the early signals are already visible.

Considering residual fuels at a high level, the main bunker hubs moved from a 1.8% specification exceedance rate in January and February 2026 to 2.6% in March and April to date. That represents a roughly 44% relative increase, with HSFO showing the stronger signal.

Singapore HSFO is one of the clearer examples. The headline specification exceedance rate was stable at 0.9% in Q4 2025 and again in January and February 2026, before rising to 2.7% in March and April to date. This does not confirm a major quality event, but it does indicate a clear change in both the rate and the composition of quality pressure.

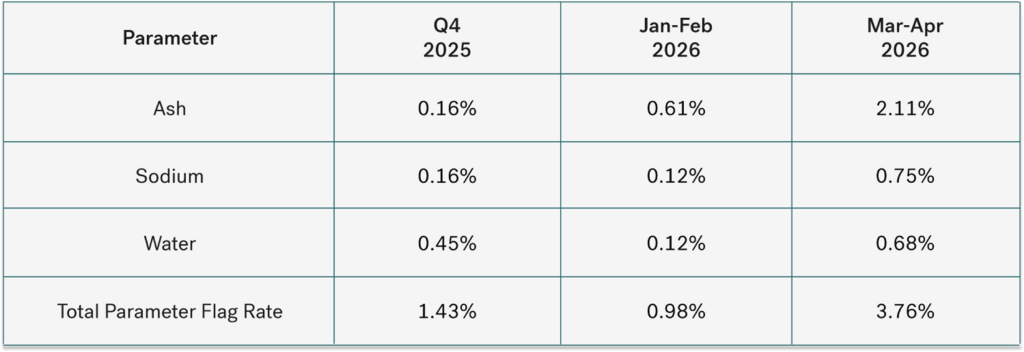

Figure 2: Data shown as individual parameter flags versus samples tested. One sample may carry more than one flag. (Integr8 Fuels)

The parameter split is where the story becomes more useful. Ash remained the main continuous signal, rising from 0.16% in Q4 2025 to 0.61% in January and February, then to 2.11% in March and April to date. Sodium also became more visible, moving from 0.12% to 0.75% between Jan-Feb and Mar-Apr 2026. Water requires careful interpretation because it was already present in Q4, eased in January and February, and then returned more strongly in March and April. This makes it a renewed signal rather than a new one.

Water matters because it is both an operational issue and a commercial one. It adds no energy, but unless it is identified and accounted for, it is still paid for as part of the delivered tonne. It also increases the amount of non-combustible material that must be settled, drained, purified, and ultimately, disposed of. When flat prices are high, this is not a minor quality inconvenience; it is direct value leakage.

The wider pattern is also consistent with tighter blend economics and reduced blend giveaway. When cutter stocks become more expensive relative to base residual material, there is increased pressure to minimise its use, hence lowering the cost of the barrel. Fuels may remain compliant, but they can sit closer to commercial or specification limits. This does not prove a quality event, but it does show how quality data can capture commercial pressure before the market gives it a name.

Away from routine table testing, the Singapore market has also seen a series of quality alerts between March and May 2026. Early reports identified elevated alkylresorcinols and phenolic compounds in VLSFO samples, with some vessels reporting sludge formation, fuel pump wear, and piston ring damage. Attention then shifted towards VLSFO stems containing compounds associated with Estonian shale oil-derived streams. Subsequent market reporting in May suggested the continued presence of these components in additional Singapore fuel samples, with indications that some blends may contain materially higher concentrations than previously observed.

At the time of reporting, operational issues had not been confirmed across all affected stems, although caution has continued to be advised. While no confirmed correlation has yet been established between these fuels and reported operational issues, including sludging and one alleged case of fuel pump damage, the most recent alert does suggest the continued presence of this stream within the market. These findings do not, in themselves, confirm a wider market quality event. However, they do reinforce the broader point that unusual blend components are appearing in the marine fuel pool during a period of shifting supply flows and tighter blend economics.

At the same time, the story is not only about shortages. Some flows are opening up. Venezuelan heavy sour crude has been moving back into the U.S. Gulf Coast refining system in greater volumes, and U.S. Gulf refiners are structurally well placed to process it. Reported Venezuelan crude imports into the U.S. Gulf increased into early 2026, with Valero reportedly targeting up to 6.5 million

barrels for March and Chevron expected to lift Venezuelan exports to the U.S. materially over the same period.

That matters for bunker quality because Venezuelan crude is not a neutral barrel. It is typically heavy and sour, and many grades carry higher asphaltene and metals content than lighter sweet alternatives. In refining, those heavier, more metal-rich components tend to concentrate into the residual fraction which is where the marine fuel pool is most exposed.

The point is not that Venezuelan crude automatically creates a quality problem; it may instead support availability and improve U.S. Gulf refinery economics. However, it can also change the residual fingerprint through density, ash, vanadium, and stability behaviour.

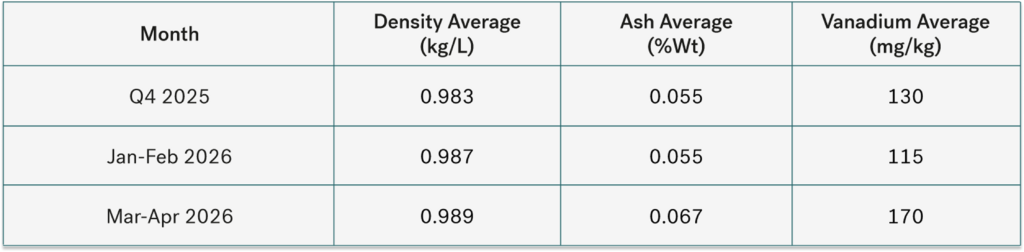

Figure 3: Data reflective of density, ash, and vanadium averages taken from fuel samples between Q4 2025 and Q1 2026. (Integr8 Fuels)

That is why the Greater Houston signal is worth watching. The formal exceedance rate does not yet indicate a major local quality event, but the fingerprint has shifted. Higher density, rising ash, and a stronger metals signal are consistent with a heavier residual pool.

This does not prove causation and should not be framed as a simple “Venezuelan crude equals quality issues” argument. The more defensible interpretation is that the crude slate and residual balancing system are changing, and the quality data is beginning to reflect that shift.

Conclusion

The conclusion is not that the market is heading for another incident like Houston in 2018 or Singapore in 2022. That would be too simplistic, and the data does not yet support it. The more important conclusion is that the conditions which allow quality risk to build are clearly present again. Bunker prices are rising, crude and product flows are shifting, blend economics are tighter, logistics are under pressure, and unusual components are already appearing in alerts outside the normal specification table. This combination is one that warrants attention.

The early data does not show a global contamination event, though it does show movement. Residual fuel exceedance rates at the main hubs have increased. HSFO is carrying the stronger signal. Singapore HSFO has shown a clear step up in ash, sodium, and water flags, and Greater Houston HSFO is developing a heavier residual fingerprint through density, ash, and vanadium. None of these realities point to a single cause. What they do point to is a bunker pool that is changing.

Quality is not only a question of whether fuel passes or fails ISO 8217. It is a question of usable energy, operational reliability, treatment burden, compatibility risk, and value loss that does not appear on the bunker invoice. Water, metals, ash, and stability behaviour all affect what the buyer receives. A clean certificate of quality does not resolve the commercial question.

The practical message is direct. This is the point in the cycle where buyers, suppliers, and operators should tighten surveillance before the claims arrive. The market may not be repeating what took place in Houston or Singapore, but the warning signs are familiar. The fuel quality data is already signalling that the pool is under stress.

Chris Turner

Technical Manager

E: chris.t@integr8fuels.com

Posted by

Chris Turner

Latest articles

Contact our Experts

With 65+ traders in 13 offices around the world, our team is available 24/7 to support you in your energy procurement needs.