News April 22, 2026

From Surplus to Shortage: The New Oil Price Outlook

Market volatility is quieter, but not quiet enough.

Any hope that the Iran war and the hike in oil prices would be short-lived, with only a limited impact on bunker prices, can be forgotten.

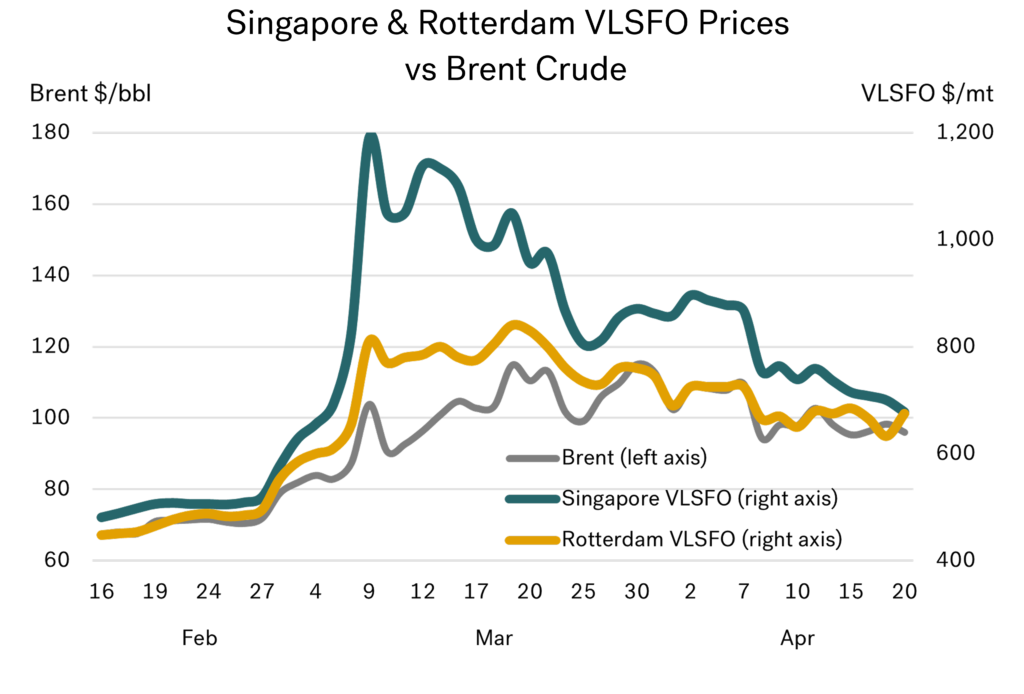

First, the good news: front-month Brent crude prices have come down from their peak of close to $120/bbl, and the massive premium paid for bunkers in Asia has disappeared. But the bad news is that we are still paying some $200/mt more for bunkers than two months ago —an increase of around 40%.

At the time of writing, front-month Brent crude is trading around the $95/bbl mark, and Singapore VLSFO prices have fallen from $1,200/mt in early March to below $700/mt. With Rotterdam prices dropping from $840/mt to $675/mt, the overall price structure looks a lot more balanced, but remains a quantum leap higher than before.

Source: Integr8 Fuels

Source: Integr8 Fuels

The huge Asian price premium was short-lived

In 2025, around 90% of crude and 75% of products passing through the Strait of Hormuz went to Asia. Therefore, it was not surprising that when the Strait closed, we saw a massive premium being paid for Asian bunkers. But, paraphrasing the oil economist Paul Frankel, the beauty and simplicity is that “oil is a liquid”, and so it can be easily moved around the world. Asian refiners have competed more aggressively for Atlantic Basin crude, taking more volumes from South America and the US. Although these crude grades are typically lighter than the ‘normal’ Middle East intake and could cause inefficiencies in the refining system, the net result is a re-balancing of crude supplies; Atlantic markets have tightened and Asian markets have eased.

This, plus a move to increase Chinese VLSFO output and some decline in product demand generally, has removed the massive Singapore VLSFO price premium seen in March.

Oil fundamentals have been turned on their head

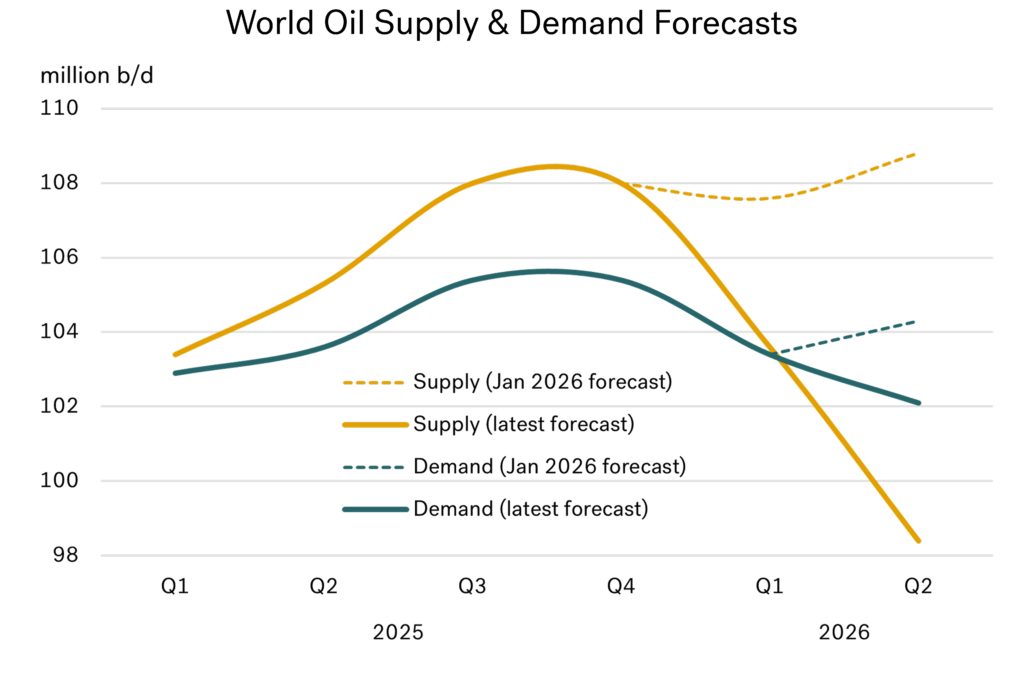

It currently looks like we have lost around 10 million b/d of oil supply due to the Hormuz closure. Although oil demand has fallen in response to higher prices and reduced availability, this only amounts to around 1.5 million b/d so far. The net result is that supply has fallen significantly below demand, and oil stocks are now declining rapidly.

On the demand side, the IEA has already revised down its oil demand forecast for this year, taking it from a modest increase of 0.7 million b/d to an actual decline of 0.1 million b/d versus 2025 levels. The longer the straits remain blocked, the greater the demand destruction will be. However, for now, the dominant story in the fundamentals is still the 10 million b/d loss in supply.

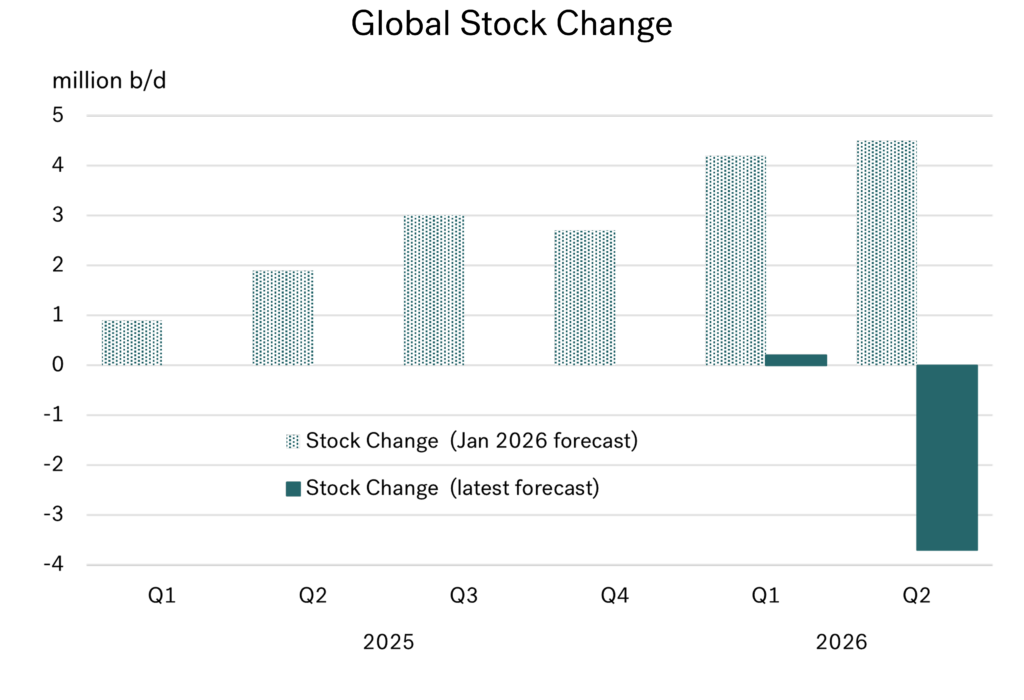

Back in January, expectations were that oil demand would be around 104 million b/d throughout this year, with supply at around 108 million b/d. The implication was a massive 4 million b/d stock build, and hence talk of much lower oil prices, even pushing VLSFO into the low $300s (see figure below).

Source: Integr8 Fuels

Source: Integr8 Fuels

The war has completely reversed these fundamentals. In the latest IEA forecasts, supply in Q2 has fallen to 98 million b/d, significantly below the revised 102 million b/d demand figure. Instead of a 4 million b/d stock build, we are now looking at a 4 million b/d stock draw. If we compare the current situation with expectations just a few months ago, it is clear why talk of Brent returning to $60/bbl and VLSFO dropping below $400/mt now looks unrealistic.

Oil stocks are now falling fast

Focusing on global stock changes, there was a build throughout the whole of 2025. The perception was that this build would grow even further in 2026, exceeding 4 million b/d in both the first and second quarters of this year. That outlook was brought to an abrupt end when the war led to the closure of the Strait of Hormuz soon after attacks began on February 28.

As a result, what was expected to be a continued build has shifted dramatically: global stocks are now estimated to show only a minimal increase in Q1, followed by a draw of around 4 million b/d in Q2 (see figure below).

Even if the war ends soon and the Strait of Hormuz reopens, the market will remain fundamentally tighter. With ongoing political and war-risk tensions, oil prices are likely to stay supported.

Source: Integr8 Fuels

Source: Integr8 Fuels

What is the latest outlook for crude prices?

The status of a ceasefire, the blockade of the Strait of Hormuz, negotiations in Pakistan, and numerous other war-related developments will have a major bearing on day-to-day price movements. In fact, it is highly likely that something significant will have changed between the writing and publication of this report.

However, one thing is clear: we are now in a very different world, with current supply shortages and heightened geopolitical and war-related risks.

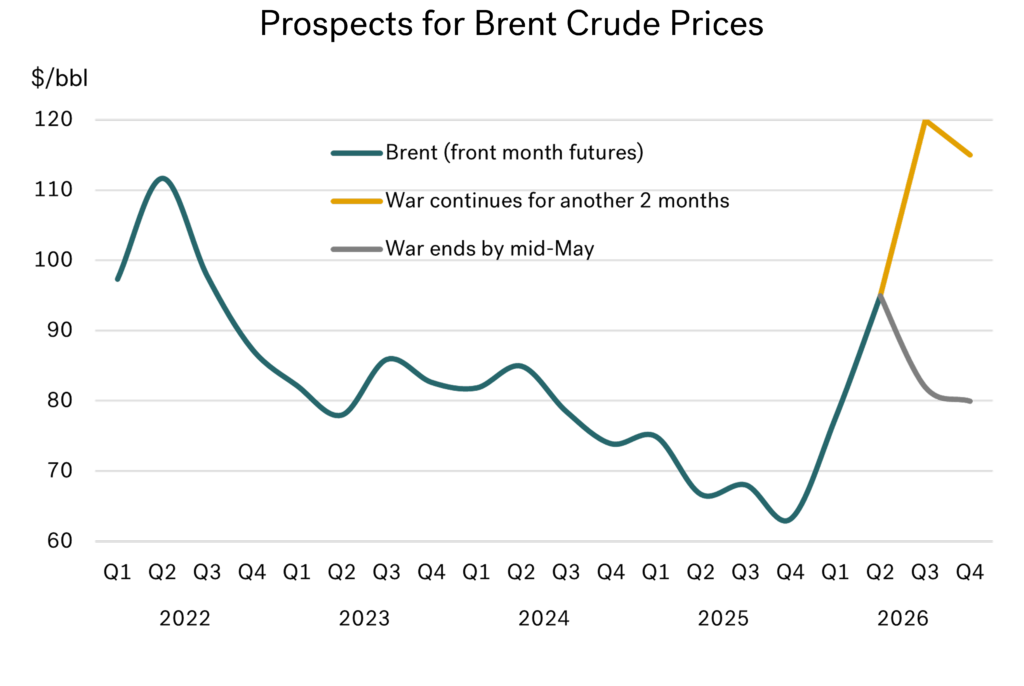

Goldman Sachs has its baseline average Brent forecast at $83/bbl for this year, and $80/bbl for the fourth quarter, assuming oil flows return to near-normal by mid-May. This compares with industry-wide forecasts of $52–60/bbl for 2026 made last October.

Goldman has also introduced an alternative scenario in its latest outlook, with Brent at $115–120/bbl in the second half of this year if there is an even later reopening of the Strait and a sustained 2 million b/d loss in oil supplies. Other analysts have suggested Brent prices could reach as high as $150/bbl if the blockade continues.

Source: Integr8 Fuels

Source: Integr8 Fuels

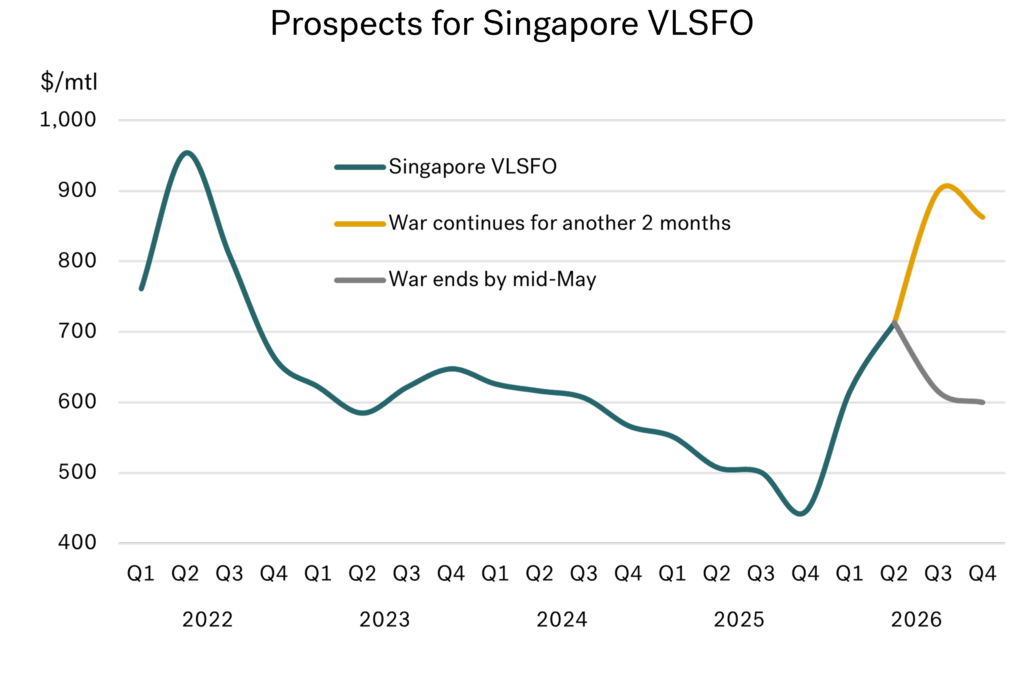

Where will bunker prices be for the rest of this year?

Superimposing the Goldman Sachs crude price forecasts onto the outlook for Singapore VLSFO indicates prices easing further from current level, down to around $600/mt in the fourth quarter in their base case (i.e. an end to the war and closure within the next 3 weeks). However, any further extension in the war and closure of the strait beyond this could push Singapore VLSFO prices closer to $900/mt in the second half of the year.

Source: Integr8 Fuels

Source: Integr8 Fuels

The bottom line

The nature of events so far means almost anything is possible. It does feel as though we may be entering a phase where the war could end soon, but even if that proves to be the case, prices are likely to remain significantly higher than previously anticipated.

The most pragmatic approach, therefore, is to watch, wait, and plan as best we can, given the uncertainty ahead.

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com

Posted by

Research Team

Latest articles

Contact our Experts

With 65+ traders in 13 offices around the world, our team is available 24/7 to support you in your energy procurement needs.