Bunker Quality Trends Report April 2026

April 6, 2026

Integr8 Fuels’ seventh edition of the bi-annual Bunker Quality Trends report reveals key trends relating to the quality and availability of both conventional and alternative marine fuels. Read More

Integr8 Fuels’ Bunker Quality Trends Report April 2026

Integr8 Fuels’ latest biannual Bunker Quality Trends Report explores how global availability, alternative fuels, and geopolitics are shaping an increasingly complex marine fuel market. The data assessment period for this report spans from July 2025 to January 2026.

Key findings include:

-

Global Availability: Stable at a macro level, but risk is increasingly localised. Availability is driven by supply chain complexity, port-specific variability, and operational factors rather than systemic quality decline.

-

Biofuels: Biofuel risk is operational rather than structural, with handling, compatibility, and feedstock variability now defining performance above specification limits.

-

Geopolitics & Regulations: The shift from price to value is accelerating, energy content and carbon exposure (EU ETS) are reshaping fuel economics, while regulatory and crude flow changes add new layers of complexity.

Trusted by thousands of operators, shipowners, bunker buyers and market analysts, this report is a go-to resource for mitigating risk and improving buying performance.

About the Author:

Chris Turner, Technical Manager

Chris joined Integr8 Fuels in 2017, spending several years in Singapore before relocating to Dubai. With over 35 years in oil and shipping, he has held roles in laboratory management, physical supply, broking, and trading. More recently, he has focused on technical supervision of exclusive buying and helped develop quality systems for biofuel purchasing, leading to Integr8’s ISCC certification.

An active IBIA Technical Working Group member, Chris is also a regular speaker and panellist at major bunkering conferences worldwide.

New partnership to boost bunker fuel services at NSW’s Port of Edrom

November 24, 2025

Integr8 Fuels signed a Memorandum of Understanding with Pentarch Offshore Solutions, formalised on 12 November, at the Port of Edrom, NSW, Australia Read More

Pictured: Chris Seidel (Integr8 Fuels) and William Kavanan (Pentarch Offshore Solutions)

Integr8 Fuels is pleased to announce the signing of a Memorandum of Understanding (MOU) with Pentarch Offshore Solutions, formalised during an event on 12 November, at the Port of Edrom, Eden, New South Wales (NSW), Australia.

The agreement marks a key step in enhancing bunker fuel provision and operational support for expanding offshore energy, maritime, and defence activities in the region. Representatives from the NSW Port Authority and Regional Development NSW were also present to witness the signing.

Meeting Growing Australian Maritime Refuelling Needs

Integr8 Fuels, alongside Pentarch Offshore Solutions and regional stakeholders, is contributing to the ongoing transformation of the Port of Edrom into a multi-functional marine and energy terminal.

The MOU builds on existing fuel supply commitments to a range of Australian and international marine contractors, including allied defence and naval refuelling operations.

Christopher Seidel, Integr8 Fuels’ Business Manager, said:

“This partnership strengthens Integr8 Fuels’ presence in the Australian market, demonstrating our commitment to supporting critical marine and offshore operations. We look forward to collaborating with Pentarch Offshore Solutions and contributing to the growth and capability of the Port of Edrom and the Far South Coast community of New South Wales.”

William Kanavan, Managing Director of Pentarch Offshore Solutions, commented:

“The signing of this MOU marks a significant milestone for Pentarch Offshore Solutions, firmly positioning our region on the global map as a growing hub for marine and offshore energy operations. Our developing partnership with a world-leading fuel provider like Integr8 Fuels demonstrates the scale of opportunity this regional port can deliver – for industry, and for Australia.”

___

Integr8 Sales Contact: Chris Seidel, chris.s@integr8fuels.com

Integr8 Media Contact: Angela Freeth, angela.f@integr8fuels.com

Bunker Quality Trends Report September 2025

September 10, 2025

Integr8 Fuels’ sixth edition of the bi-annual Bunker Quality Trends report reveals key trends relating to the quality and availability of both conventional and alternative marine fuels. Read More

Integr8 Fuels’ Bunker Quality Trends Report H1 2025

Integr8 Fuels’ latest biannual Bunker Quality Trends Report explores how sanctions, new regulations, and alternative fuels are reshaping marine fuel markets in 2025.

Key findings include:

-

Sanctions: U.S. measures have reshaped global fuel flows, leading to quality issues in key hubs where Russian stock has been replaced by barrels from the Middle East.

-

Mediterranean ECA: The 0.1% sulphur cap has transformed the regional fuel mix, with VLSFO use halving and distillate demand surging. Early ULSFO quality issues are now easing.

-

Biofuels: While niche, biofuels are becoming cost-competitive under EU and ECA rules if savvy-buying strategies are followed. Risks include pour point challenges, but strategic buying can unlock regulatory and financial advantages.

Trusted by thousands of operators, owners, bunker buyers and market analysts, this report is a go-to resource for mitigating risk and improving buying performance.

A word from the author, Chris Turner, Bunker Quality & Claims Manager:

“Sanctions, new ECAs and alternative fuels are all reshaping the bunker landscape at the same time. Our latest whitepaper shows how these changes are not only affecting fuel availability and compliance but also creating new risks and opportunities in quality and cost. Shipowners need to stay on top of these shifts to avoid exposure and unlock the benefits where they exist.”

ADNOC L&S highlights Integr8 as key to its alternative bunker fuel strategy

June 9, 2025

ADNOC L&S stated that Integr8's global footprint, market expertise, and data-led trading capabilities position the company as a critical partner in delivering cleaner, more compliant marine fuels. Read More

DUBAI, 09 June 2025 – ADNOC Logistics & Services (ADNOC L&S), subsidiary of the Abu Dhabi National Oil Company, has named Integr8 as a central component of its strategy to scale up alternative bunker fuel supply, including biofuels and LNG.

In a recent interview with S&P Global Commodity Insights, ADNOC L&S CEO Abdulkareem Al Masabi, explained how Integr8’s global footprint, market expertise, and data-led trading capabilities position the company as a critical partner in delivering cleaner, more compliant marine fuels. The comments underscore Integr8’s strategic role in supporting ADNOC L&S’s ambitions to grow its influence in the evolving alternative fuels market.

“Integr8 will play an integral part going forward (when we) look at alternate fuels,” Al Masabi said. “Whether it be ammonia, biofuels and LNG… all of these things are actually in the game plan for Integr8 going forward.”

As demand for lower-emission fuels grows and compliance challenges increase, ADNOC L&S’s endorsement highlights the vital role of agile, globally connected traders like Integr8 in supporting the maritime energy transition.

Read the interview on the S&P Global website here.

Media Contact:

Angela Freeth, angela.f@integr8fuels.com

Integr8 announced as Emerald Sponsor and Cocktail Host at PULSES 25

May 19, 2025

Integr8 Fuels is proud to be an Emerald Sponsor of PULSES 25, the Global Pulse Confederation’s (GPC) flagship conference, taking place in Singapore from 20–22 May 2025. Read More

SINGAPORE, 19 May 2025 – Integr8 Fuels is proud to be an Emerald Sponsor of PULSES 25, the Global Pulse Confederation’s (GPC) flagship conference, taking place in Singapore from 20–22 May 2025.

As part of its sponsorship, Integr8 will host the closing cocktail reception on 22 May, bringing delegates together for a relaxed and sociable end to three days of discussion, insight and networking.

PULSES 25 brings together stakeholders from across the global pulse sector to explore critical issues including food security, sustainability, innovation, investment, and the digitalisation of trade. The event features keynote addresses from industry leaders and expert-led panel discussions, making it a key fixture in the GPC calendar for members looking to stay ahead in a rapidly evolving global market.

“Integr8 is proud to support an event that fosters international collaboration and dialogue on issues that impact the global food supply chain,” said a spokesperson at Integr8 Fuels. “We look forward to welcoming delegates at the closing cocktail reception in Singapore.”

PULSES 25 is open exclusively to members of the Global Pulse Confederation. Membership provides access to the event and a range of benefits throughout the year.

For more information about the event and how to attend, visit https://pulses25.globalpulses.com.

Media Contact:

Angela Freeth, angela.f@integr8fuels.com

Integr8 Report Highlights VLSFO Quality Challenges, Biofuel Compliance Strategies, and Future Bunkering Trends

January 14, 2025

Integr8 renews ISCC EU certification to trade sustainable biofuels and help shipowners prove regulatory compliance. Read More

London, United Kingdom – 14 January 2025: Integr8 Fuels has published its latest Bunker Quality Trends report, offering unparalleled insights into the evolving landscape of marine fuels. Drawing on comprehensive data from over 130 million metric tons (MT) of deliveries, the report provides an in-depth analysis of critical quality issues, regulatory implications, and market trends. This edition of the report highlights five key developments:

- Why Changes in VLSFO Blends Could Trigger a Wave of Problem Fuels (Pg 10)

- The Smart Way to Meet Biofuel Targets: Plan Biofuel Bunkering on a Fleet or Pool Level (Pg 23)

- Barge Bottlenecks: The Sulphur Compliance Challenge in Southern Europe (Pg 12)

- Rising Automotive Fuel Blends Are Driving Flash Point Risks in the Med (Pg 19)

- Biofuels and LNG: Key Players in the Future of Fuel Compliance (Pgs 21-26)

Why Changes in VLSFO Blends Could Trigger a Wave of Problem Fuels

The introduction of the ISO 8217:2024 specification has brought renewed focus on viscosity limits, with a significant proportion of VLSFOs currently failing to meet the updated standards. Data from the report shows that over 45% of global VLSFO supply would not meet the RM380 2024 specification without adjustments to blend recipes. These changes could lead to a spike in problematic fuels, as was observed during the IMO 2020 transition, potentially affecting fuel stability and other critical parameters. Regions like Singapore and Houston are flagged as hotspots for adjustments, with over two-thirds of VLSFO in Singapore requiring reformulation. Buyers are urged to adapt charterparty wording to ensure suppliers comply with the latest standards to reduce the risk of critical handling issues.

The Smart Way to Meet Compliance Targets: Plan Biofuel Bunkering on a Fleet or Pool Level

When it comes to compliance with environmental regulations, FuelEU Maritime doesn’t specify a fixed biofuel percentage. The focus is on reducing the greenhouse gas (GHG) intensity across a vessel’s voyages over the course of a calendar year. The target is a 2% reduction in GHG intensity between two EU ports, which translates to around 3% biofuel blended with VLSFO or HSFO, or 2% biofuel with MGO. However, it’s more efficient to take larger biofuel quantities on select vessels and transfer compliance surpluses across your fleet or between ships in multiple fleets, which is also known as pooling. The most common biofuel grades stocked by suppliers are B24 and B30 blends, and pure B100. Their availability varies by port and region. Shipowners are advised to carefully manage their biofuel strategies and check the GHG intensity figures in Proof of Sustainability documents provided by suppliers.

Barge Bottlenecks: The Sulphur Compliance Challenge in Southern Europe

Sulphur compliance for VLSFO remains a pressing concern, with 2.4% of supplies exceeding the 95% confidence limits for ISO 8217 Table 2 parameters in the past six months. Geographical variances are significant, with higher non-compliance risks reported in bunker hubs such as Rotterdam and Balboa compared to Singapore. Infrastructure constraints, including the practice of switching between HSFO and VLSFO on the same barges, are identified as contributing factors. The report underscores the importance of data-driven procurement and robust supplier practices to mitigate these risks.

Rising Automotive Fuel Blends Are Driving Flash Point Risks in the Med

The integration of automotive diesel into bunkering pools has led to heightened risks of flash point non-compliance, particularly in the Mediterranean. Automotive fuels often have a minimum flash point of 55°C, below the 60°C threshold mandated for marine fuels under SOLAS regulations. The report identifies specific ports where these risks are most prevalent and calls for enhanced due diligence when purchasing in regions reliant on automotive diesel imports. Ensuring DMA specifications are met is critical to avoiding costly compliance breaches.

Biofuels and LNG: Key Players in the Future of Fuel Compliance

The report highlights the growing role of biofuels and LNG as transitional solutions for meeting stringent emissions regulations, such as FuelEU Maritime and the upcoming Mediterranean Emission Control Area (Med ECA). While LNG remains a reliable option due to its consistent quality and negligible SOx emissions, biofuels are gaining momentum as suppliers expand blending capabilities globally. The report cautions buyers about potential operational risks, such as biofuel-related cold flow challenges in colder climates and the limited availability of LNG bunker vessels. The introduction of the Med ECA from 1 May 2025 will likely boost LNG bunker demand in the region, however, the delivery of LNG bunker vessels is failing to keep up with growing demand, tightening the LNG supply chain.

The full report is available to download for free from the Integr8 website: https://integr8fuels.com/fuel-quality-trends-q1-2025/

Press Contact: Angela Freeth

Email: marketing@integr8fuels.com

To see how we can assist you with your fuel procurement requirements, visit our Contact Us page.

Bunker Quality Trends Report Jan 2025

January 14, 2025

Integr8 Fuels’ fifth edition of the bi-annual report analyses data from 130 million metric tons of supply, to reveal key trends relating to fuel quality and availability. Read More

This January 2025 edition of Integr8’s Bunker Quality Trends report is an essential resource for shipowners, charterers, and operators seeking to make informed decisions in an increasingly complex regulatory and market environment.

Leveraging data from over 130 million metric tons (MT) of global bunker fuel deliveries, the report highlights the most critical issues and actionable insights for the industry, including:

Strategic Buying

- Why Changes in VLSFO Blends Could Trigger a Wave of Problem Fuels

- Barge Bottlenecks: The Sulphur Compliance Challenge in Southern Europe

- Rising Automotive Fuel Blends Are Driving Flash Point Risks in the Med

- Smarter Procurement: Strategies to Tackle Fuel Quality and Availability Challenges

Practical Compliance

- Biofuel Compliance: How Much Ship Operators Need and the Smartest Way to Buy

- Navigating ISO 8217:2024 and Med ECA Rules: Adapting to a New Era

- Biofuels and LNG: Key Players in the Future of Fuel Compliance

Published January 2025

Integr8 Fuels renews ISCC EU certification for sustainable biofuel trading

December 31, 2024

Integr8 renews ISCC EU certification to trade sustainable biofuels and help shipowners prove regulatory compliance. Read More

Dubai, UAE – 31 December 2024 – Integr8 Fuels is pleased to announce the renewal of its International Sustainability and Carbon Certification (ISCC) certificate for the trading of sustainable biofuels. This renewal underscores Integr8’s ongoing commitment to providing shipowners with biofuels that are produced from legitimate feedstocks and via processes that meet stringent environmental regulations.

The ISCC EU certification is a globally recognised standard for sustainable production, sourcing, and trading of bio-based feedstocks and biofuels. With this renewed certification, Integr8 continues to offer Proof of Sustainability (PoS) for various liquid and gaseous biofuels, including fatty acid methyl ester (FAME), hydrotreated vegetable oil (HVO), and liquefied biomethane (LBM).

A PoS follows a fuel batch throughout its whole supply chain with greenhouse gas estimates. This documentation enables shipowners to demonstrate compliance with environmental regulations such as the EU Emissions Trading System and FuelEU Maritime, which require verifiable use of sustainable low-carbon fuels.

Chris Turner, Integr8’s Bunker Quality and Claims Manager, emphasised the importance of this certification:

“Renewing our ISCC EU certification reflects our dedication to supporting the maritime industry’s transition to more sustainable energy solutions. It ensures that our clients can continue to rely on us for compliant and ethically sourced biofuels.”

Integr8 Fuels remains committed to facilitating the shipping industry’s efforts to reduce greenhouse gas emissions by providing certified sustainable biofuels and comprehensive support to navigate evolving environmental regulations.

Press Contact: Angela Freeth

Email: marketing@integr8fuels.com

To see how we can assist you with your fuel procurement requirements, visit our Contact Us page.

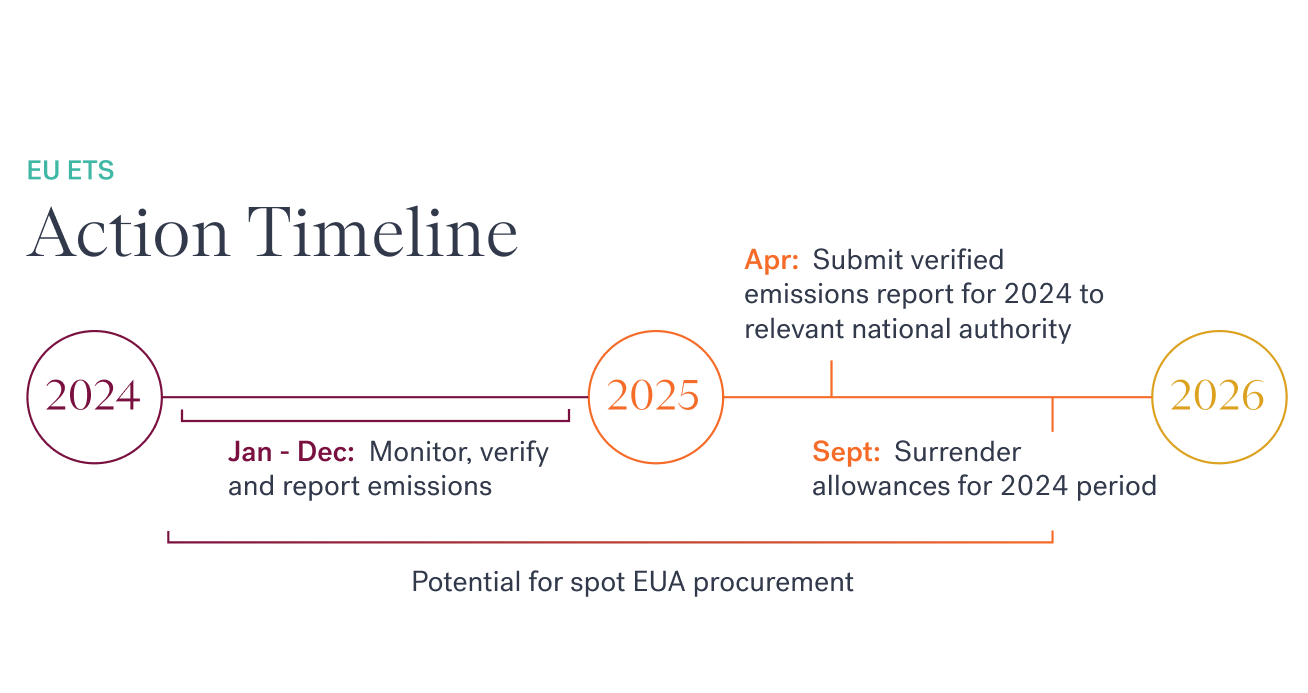

Utilising the physical spot EUA market for 2025 EU ETS compliance

December 12, 2024

How strategic buying can help shipping companies avoid a compliance headache. Read More

Marketing Communication

How strategic buying can help shipping companies avoid a compliance headache.

In less than a year, shipping companies will need to surrender enough European Union Allowances (EUAs) to cover their emissions for the 2024 reporting period.

With this date fast approaching, waiting until the September 2025 deadline to purchase EUAs could be costly. Many forward-thinking shipowners have been choosing a proactive approach by buying allowances immediately post-voyage in 2024 and will continue to do so in early 2025.

Why Adopt a Buy-As-You-Go Strategy for EUAs?

A buy-as-you-go approach to purchasing EUAs offers businesses a practical and efficient way to manage their carbon compliance obligations. This strategy is particularly beneficial for organisations looking to balance cost, stability, and regulatory compliance in a dynamic market environment.

One of the main advantages of this approach is improved budget management. Rather than waiting until deadlines to make potentially large payments, businesses can spread the cost of EUAs over time, by factoring in the cost of EUAs into freight prices on an ongoing basis and purchasing EUAs accordingly. This allows for greater financial flexibility and helps avoid the strain of lump-sum purchases at the last minute.

Additionally, a buy-as-you-go strategy can help mitigate the effects of price volatility in the EUA market. By purchasing allowances incrementally, companies can reduce their exposure to sudden price fluctuations, creating a more stable and predictable financial framework.

Finally, this approach ensures businesses stay ahead in meeting compliance requirements. Regularly purchasing allowances helps to avoid the risk of falling short, ensuring companies can meet their obligations and steer clear of fines or sanctions.

By adopting a buy-as-you-go strategy, businesses can take a proactive, balanced approach to managing their carbon responsibilities while maintaining financial control and operational peace of mind.

Simplifying EUA Procurement

Navigating the complexities of EUA procurement and compliance obligations can be challenging, which is why Integr8 offers a specialised team to support shipowners with the task. By leveraging the expertise of seasoned traders, Integr8’s Carbon Desk provides a flexible service tailored to meet the needs of businesses of all sizes.

One of the key advantages of the service is its accessibility (subject to confirmations of eligibility on a case-by-case basis). There are no minimum purchase requirements, meaning traders can start with as few as one EUA. This flexibility allows businesses to engage with the market on their own terms, whether they are looking to make small-scale purchases or explore larger opportunities over time.

Integr8 also eliminates upfront costs by forgoing commitment fees, making it easy for eligible companies to begin trading without financial barriers. The onboarding process is simple and efficient, with a straightforward KYC (Know Your Customer) process that ensures quick setup and minimal disruption.

All transactions are conducted in USD, helping to reduce foreign exchange risks and provide greater financial clarity. This approach is particularly beneficial for eligible businesses seeking to minimise complexities when managing their carbon compliance obligations.

By providing a seamless and accessible platform, Integr8’s Carbon Desk allows eligible businesses to streamline their EUA procurement and focus on achieving their environmental and compliance goals with confidence.

To request a free 30-minute consultation or to receive a brochure, email carbon@integr8fuels.com or contact your trading representative.

Media Contact:

Angela Freeth, angela.f@integr8fuels.com

Integr8 Fuels announces sponsorship of IBIA Annual Convention 2024

October 29, 2024

This flagship event, hosted by the International Bunker Industry Association (IBIA), will gather industry leaders from across the maritime and bunker sectors to address the evolving challenges and opportunities within the fuel supply chain. Read More

Athens, Greece – 29 October 2024 – Integr8 Fuels, a leading provider of marine fuel procurement and carbon trading services, is proud to announce its role as bronze sponsor of the IBIA Annual Convention 2024, taking place in Athens from 6-7 November. This flagship event, hosted by the International Bunker Industry Association (IBIA), will gather industry leaders from across the maritime and bunker sectors to address the evolving challenges and opportunities within the fuel supply chain.

Integr8 Fuels delivers a comprehensive range of services for shipowners and operators worldwide, offering data-driven insights and robust fuel management solutions. The company’s expertise in fuel procurement and risk management has made it a trusted partner for global fleets looking to optimise fuel strategies and navigate market volatility.

“We are excited to sponsor the IBIA Annual Convention 2024,” said an Integr8 Fuels spokesperson. “As the industry continues to focus on sustainability and operational efficiency, this event provides a vital forum for collaboration and exchange. We look forward to connecting with our industry peers to explore innovative ways to address these pressing challenges.”

Throughout the event, representatives from the Integr8 Fuels Athens office will be available to discuss the company’s latest offerings and insights into the trends shaping the future of marine fuel.

To arrange a meeting with an Integr8 Fuels representative at the convention, please email athens@integr8fuels.com.

For more information about the event, visit https://www.ibiaconvention.com/.

Media Contact:

Angela Freeth, angela.f@integr8fuels.com