News November 17, 2021

VLSFO: Back To Where We Started on ‘Day 1’ – What’s Next?

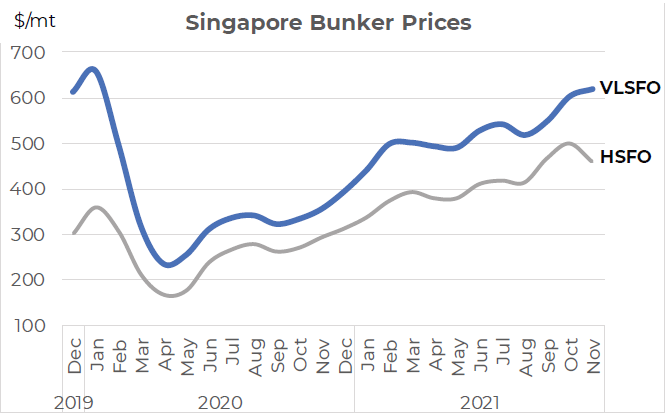

VLSFO prices back above $600

When VLSFO was fully introduced in December 2019/ January 2020, Singapore prices were in the range $615-660/mt; so far in November have averaged $620/mt – we are back to where it all started!

Source: Integr8 Fuels

Source: Integr8 Fuels

Events over the past 22 months are well documented and will be written about for many years to come. The oil industry will be a mere microcosm of all this, but when you are involved in the bunker market these oil industry details become significant. The collapse in oil demand at the start of the pandemic led VLSFO prices down to around $250/mt. The subsequent cutbacks in OPEC+ crude production, combined with the loss of US crude supplies and the eventual rebound in oil demand have all contributed to the rise in oil prices and the reason why VLSFO has moved back above $600/mt. The clear question is: Where do we go from here?

Analysts foresee prices falling from here

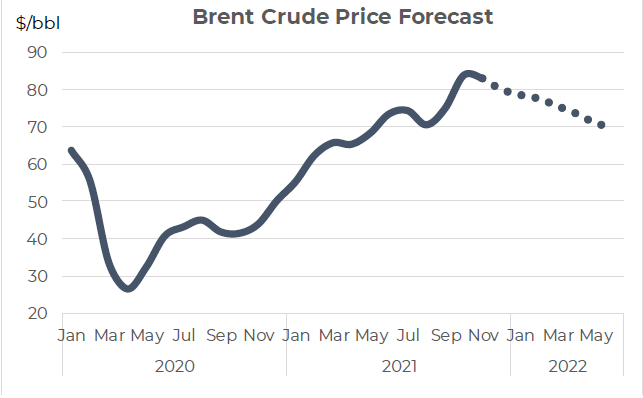

Some analysts are indicating that we are currently at a peak, and that prices will ease from here. Brent crude futures (front month) hit a high of above $86/bbl in late October and are currently trading around $82/bbl. The pointers now are towards $75/bbl in Q1 next year and $70/bbl by Q2. On this basis, it would imply Singapore VLSFO down from around $610/mt currently, to around $565/mt in Q1 and $530/mt by next June.

The fundamentals always ‘win out’

The recent price highs have come about as oil demand continues to

rebound and OPEC+ maintain their planned, and constrained increases

in production. Despite some pressure from the US on OPEC+ to go beyond this, there has been no shift in OPEC+ (nor Saudi) policy for countries with spare capacity to raise output in light of current prices.

This is despite some member countries producing below their allocated quotas because of previous low prices and a lack of spending in their upstream sectors. This rise in demand and constraints on supply has left oil stocks at low levels, and markets fundamentally tight. Also, although US crude production is rising in the wake of higher oil prices, the gains are considered relatively low, with a number of upstream companies ‘forced’ to reduce debts or pay shareholder dividends rather than go out on a massive expansion in drilling activity.

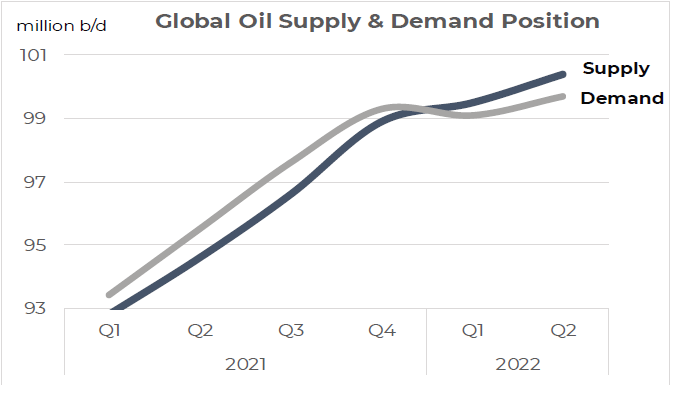

The overall result has been that oil demand has exceeded oil supply so far this year, and we have been in an extended period of stockdraws, leaving the market tight and Brent prices well in to the $80s.

The expectations now are that oil supply will continue to increase, even under the current OPEC+ strategy. On the demand side, total consumption is now back close to pre-pandemic levels and so future gains are seen as far more modest, stalling at just above 99 million b/d through to the middle of next year.

Source: Integr8 Fuels

Source: Integr8 Fuels

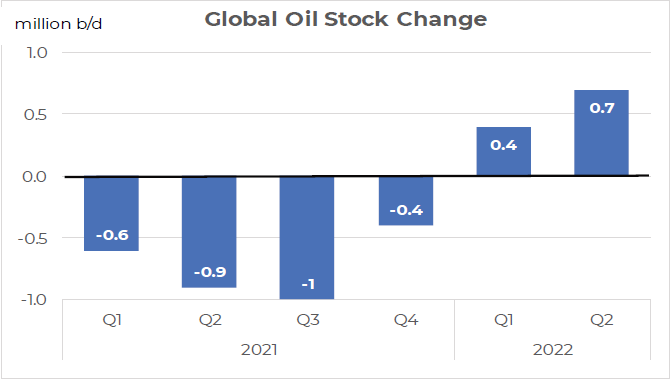

We are moving from a position of stockdraws to stockbuilds

This means we would shift from a global stockdraw averaging around 0.7 million b/d this year, to a stockbuild of 0.6 million b/d in the first half of next year. It is this anticipated shift in oil fundamentals that forms the backdrop to lower price forecasts through to the middle of next year.

Source: Integr8 Fuels

Source: Integr8 Fuels

Subject to change – Here are some of the known unknowns:

In addition to this ‘base’ position, there is also a possibility of developments and an agreement in the US-Iran nuclear talks, which resume at end November. The next 6 months may be too soon to see any material increase in oil supplies, but if sanctions on Iran are lifted, the expectations are that they could increase production and exports by 1.0- 1.5 million b/d. There are clearly a number of other variables that could affect this base case, not least with the pandemic (positive or negative), but also the extent of the northern hemisphere winter; any further demands on oil into power generation; what may happen to US production; and the OPEC+ strategy.

Finally, the economy, high prices and inflation can cause trigger responses, such as a reduction in oil demand and the release of strategic oil reserves (although the use of reserves usually has little long-term effect on oil prices). Any of these factors could lead to analysts changing their views.

Today’s mood is bearish on price

Working within the base case, analysts are indicating Brent prices falling back down to around $70/bbl by the middle of next year, as stocks build and tightness eases.

Source: Integr8 Fuels

Source: Integr8 Fuels

We have often outlined that the crude price largely sets the absolute

level of bunker prices, but with VLSFO and HSFO also having relative

strengthening or weaking positions against crude, driven by what is

happening in:

- The refining sector with margins and maintenance;

- Supply and demand developments for other oil products;

- At extremes, even what is happening to natural gas prices (as highlighted in one of our reports last month).

In the first instance here, we have taken a fixed relationship with crude prices, to at least show the extend of bunker price movements based on analysts’ current expectations for Brent. In subsequent reports we will

return to looking at the relative shifts in bunker prices versus crude oil and other product prices.

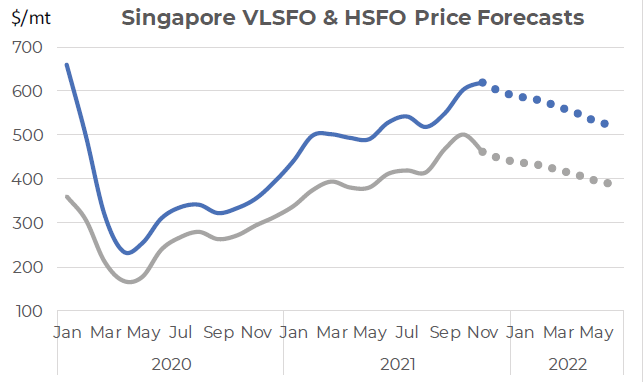

From this, current bunker prices are seen as towards their highs and that some downwards movement is expected. In this case it shows bunker prices will ease back towards levels seen at during the first half of this year, with Singapore VLSFO in the low $500s by the middle of next year. This is around $100/mt lower than today. On the same basis, Singapore HSFO would be around $380/mt by mid-2022.

Source: Integr8 Fuels

Source: Integr8 Fuels

The relative price of bunkers can easily shift, with any extreme cold weather ‘pulling’ more HSFO into power generation (such as in Pakistan, or in S. Kora/Japan) and giving relative strength to HSFO prices. Conversely, if global oil demand is stronger than forecast coming out of the northern hemisphere winter, we could expect higher refinery throughputs and more HSFO supplies, putting relative downwards pressure on HSFO prices. Typically, higher global oil demand would lead to a relative strengthening in VLSFO pricing (and vice versa). These are nuances around the underlying price of bunkers, but still important. By definition, things can change, but the sentiment today is one of weakening bunker prices in the near term.

Steve Christy, Research Contributor

E: steve.christy@integr8fuels.com

Posted by

Elaina Cameron

Contact our Experts

With 65+ traders in 13 offices around the world, our team is available 24/7 to support you in your energy procurement needs.