News May 20, 2026

Tighter Refining Conditions Are Supporting Higher Bunker Prices

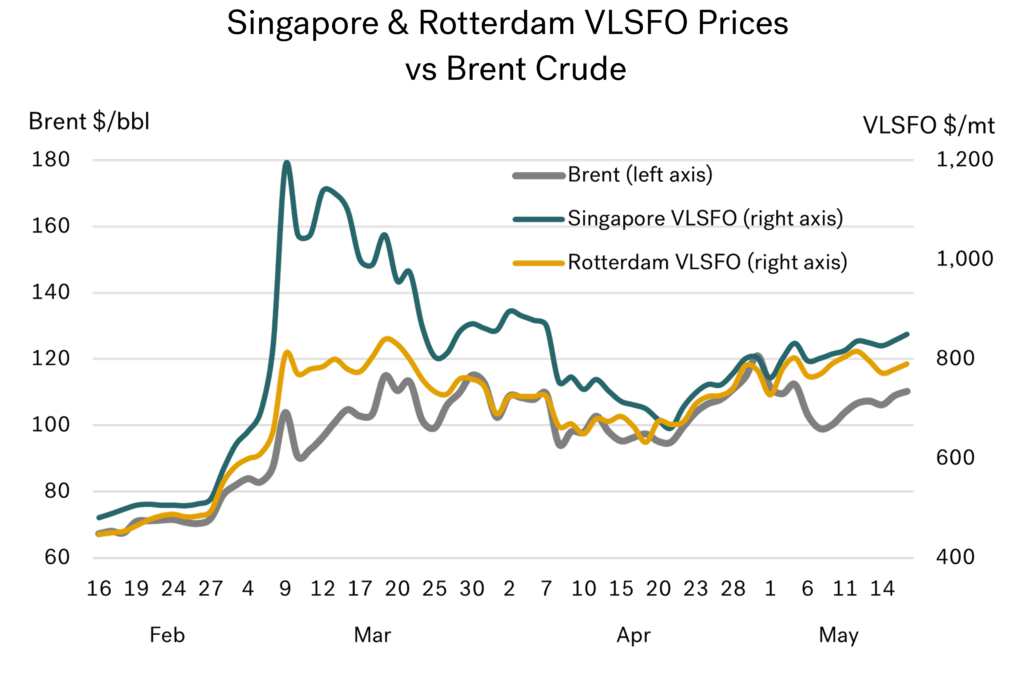

Prices are on the up (again)

We have already seen that it is almost impossible to predict how and when the Iran war will end, and when the Strait of Hormuz will reopen. In last month’s report, we looked at the potential for bunker prices to fall if the war were to end within two to three weeks, which seemed credible at the time, and a higher price trajectory towards $900/mt for Singapore VLSFO if the war continued for another one to two months. At present, we are clearly on the higher trajectory.

Prices continue to rise and fall with sentiment surrounding a possible end to the war, but over the past couple of weeks the overall direction has been upwards. At the same time, bunker prices have once again moved ahead of crude, and Singapore VLSFO also strengthened relative to Rotterdam.

Source: Integr8 Fuels

Source: Integr8 Fuels

Where to next?

It seems we are on a rolling cycle of commentary where analysts continue to assume the war will end within the next month. However, even if it does, refinery operations have already been severely reduced and stock levels materially depleted. There is no quick return to where we were; the market has fundamentally changed in the past 12 weeks.

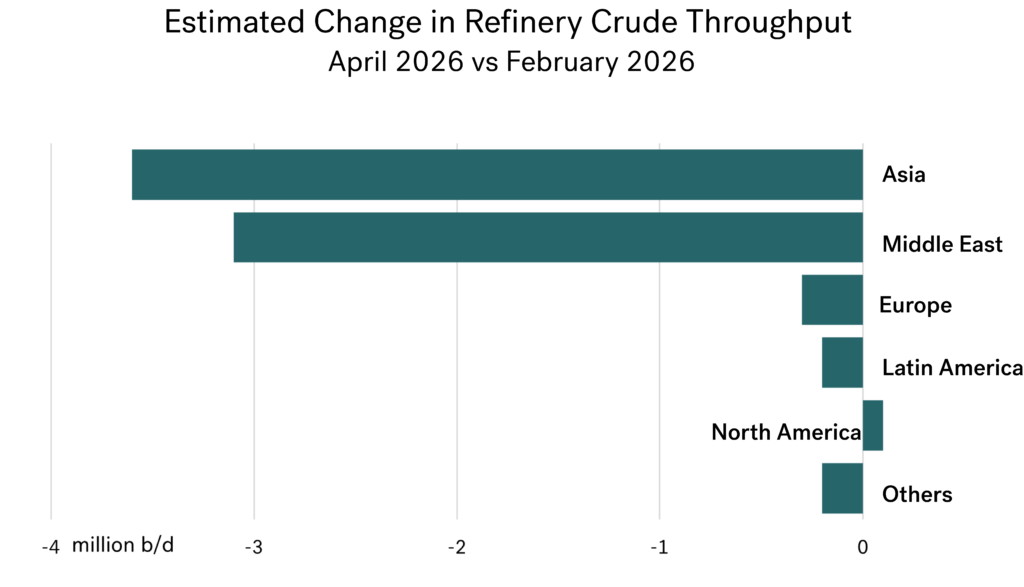

Refinery throughput is down and product markets are looking increasingly tight

The loss of Middle East crude production and refinery operations is at the centre of everything. Looking at the IEA’s view of the refinery sector, estimated global throughput for April is down by more than 7 million b/d since the start of the war. This is significantly greater than the estimated 3 million b/d drop in demand that has taken place this quarter.

The consequence is lower product stock levels and tighter product markets, creating uncertainty, higher prices, and higher refinery margins.

Current IEA forecasts for refinery throughput are also based on the Strait reopening sometime within the next month, with Middle East crude production and refinery operations moving much higher in Q3 and returning to pre-war levels in Q4. It is not an unreasonable premise, but it remains only

a premise.

Source: IEA

Source: IEA

The impact on refining is focused East of Suez

The more than 7 million b/d cutback in global refinery operations since February has been concentrated in the Middle East (down 3.1 million b/d) because of the inability to export products, and in Asia-Pacific (down 3.6 million b/d) because of the initial loss of crude imports from the Middle East into the region (see figure below).

Source: IEA

Source: IEA

Cutbacks in refinery operations elsewhere have been far more limited, with European runs down by only 0.3 million b/d, and Latin America down 0.2 million b/d. Runs in North America have increased slightly. The clear loss in access to “local” refinery supplies has therefore been in Asia-Pacific. However, regions do not rely solely on their own refinery operations; product imports and exports exist to balance deficits and surpluses across all international markets.

If one region suffers, every region suffers

Even through throughputs in the West have been largely unaffected, the competition for international products has intensified. As a prime example, Europe relies heavily on diesel, gasoil, and jet imports from the Middle East, but so does Asia-Pacific. This means both regions are now trying to “fill the gap”, but the situation in Asia is even more extreme because the region also has a massive shortfall in product supply from its own refineries.

This results in increased global competition for crude and products, lower oil stocks, a tightening market, higher prices, and stronger refining margins.

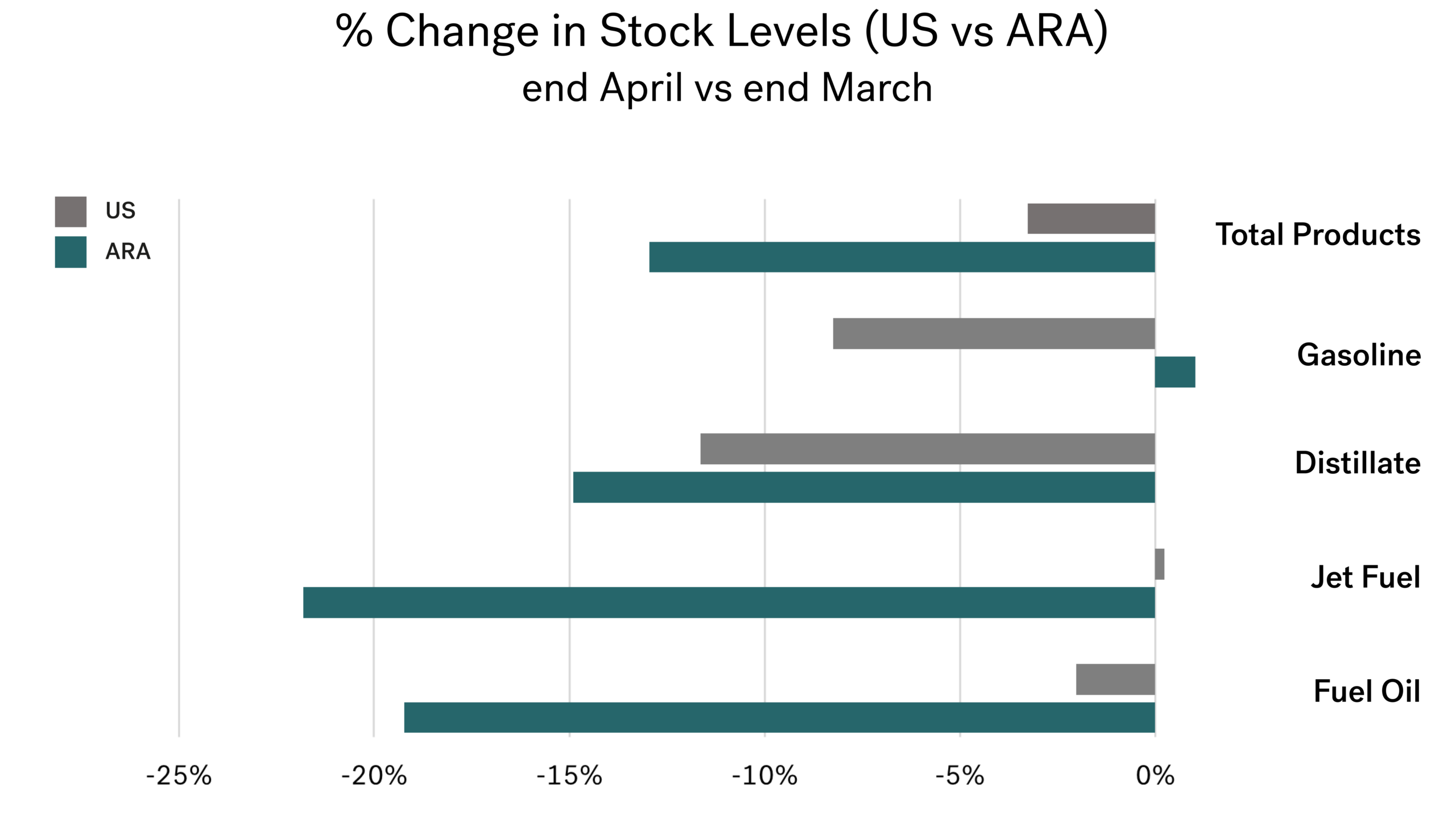

Early indications of what is happening to product stocks

These market squeezes can be observed through stock levels but reported stock data usually lags by at least 2-3 months, meaning we are still in a “waiting game” for full confirmation.

The fundamentals indicate a global stock draw of around 4 million b/d, while available data from the US and independent storage in Amsterdam, Rotterdam, and Antwerp (ARA) help to illustrate the position, including where and which products are the most under pressure.

Overall product stocks in ARA fell by 13% in April and are now at their lowest levels in more than 10 years. The situation in the US is very different, with product stocks down only 3% and still higher than 12 months ago. North-West Europe appears to be a significantly tighter market than the US.

Source: Integr8 Fuels

Source: Integr8 Fuels

However, we need to dig down to individual products. Here, gasoline stocks in the US have fallen, but the country remains a net importer of this product. Conversely, ARA gasoline stocks have increased slightly, with the region remaining a net exporter.

Distillate stocks are down sharply in North-West Europe, as the region is heavily dependent on imports. Distillate stocks in the US are also down, but this is not a demand issue; rather, it reflects higher US exports, which have reached the second-highest monthly total in 10 years, with much of this material flowing to meet European and Asian deficits. Both distillate markets are tight, but for different reasons.

The tightness in key products will have a direct bearing on VLSFO and HSFO bunker prices in these regions and further afield; we cannot separate bunker markets from wider barrel dynamics or regional product balances.

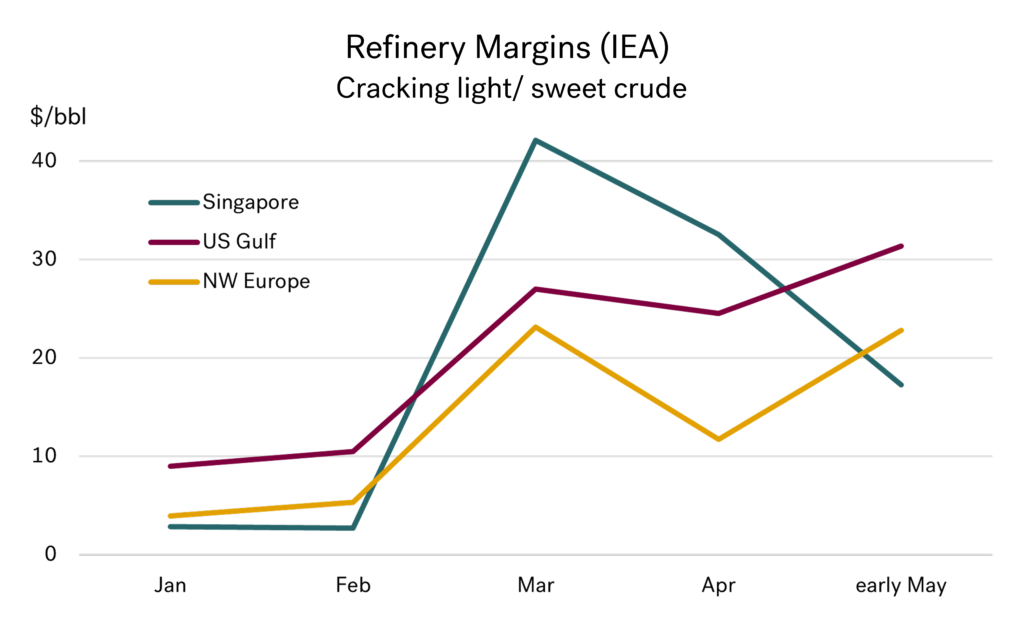

Refinery margins are an up-to-date measure of how tight markets are

Although it is still too early for more extensive oil stocks data, the implications are already clear. Product balances are tightening, and refinery margins are much higher than pre-war levels.

The initial post-war response saw Singapore refinery margins surge, reflected in exceptionally high Singapore VLSFO prices in March. Since then, we have seen a pull on crude and products from West to East. With this, there has been some rebalancing across regions, with Singapore margins easing and Atlantic margins strengthening. Currently, Singapore and European margins have converged to more similar levels, but all remain at much higher levels than in February.

These shifts in refinery margins have also been reflected in bunker price movements, with Singapore and Rotterdam VLSFO prices more closely aligned than in March and early April, although Singapore VLSFO is once again, showing signs of strengthening.

Source: IEA

Source: IEA

Conclusions

Given the market conditions and refinery margins, it is likely that upcoming seasonal refinery maintenance programmes will be limited. We are also likely to see further ebbs and flows in crude and product trade patterns, along with more releases from strategic stocks, but none of these are likely to be sufficient to fully offset current market tightness.

As for the end of the war, we appear to be in a rolling narrative where it is consistently described as being around four weeks away. If there is no near-term resolution, a potential backstop could be the run-up to the US midterm elections in November. There are no guarantees, but if that becomes the key marker, then we are talking about months rather than weeks.

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com

Posted by

Research Team

Contact our Experts

With 65+ traders in 13 offices around the world, our team is available 24/7 to support you in your energy procurement needs.