News February 19, 2026

OPEC: How Far Must Prices Fall to Force a Move?

We can learn a lot from looking at the past

History is something we can always learn from, and in the bunker market, it is worth looking back to see where prices have previously found a floor. It may not be a guarantee of what will happen, especially in extreme circumstances, though it does indicate where prices have hit a low and bounced back.

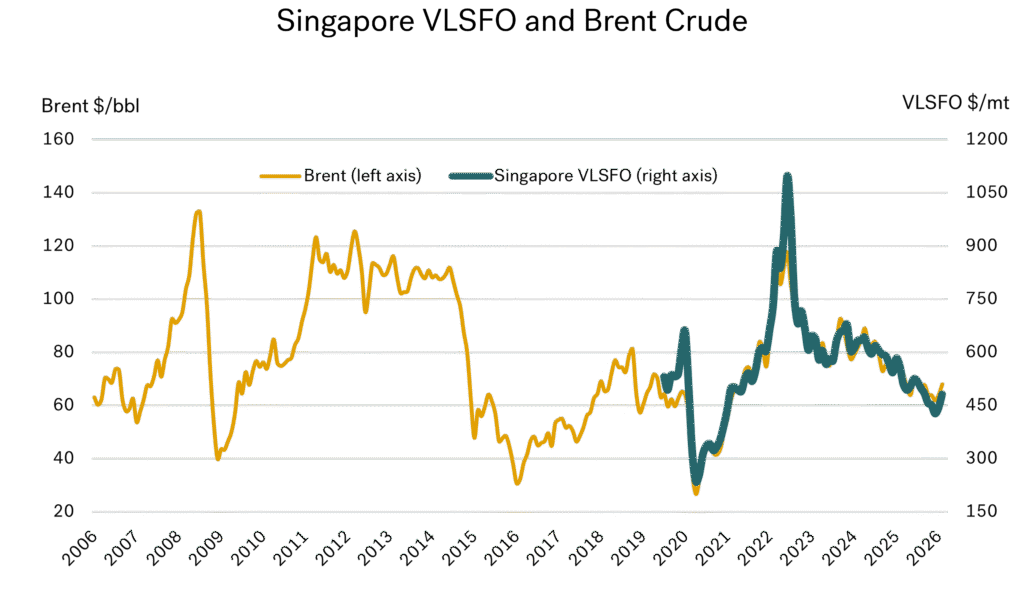

The graph below illustrates the long-run, 20-year history of average monthly Brent crude oil prices, along with prices for Singapore VLSFO as introduced in late 2019. As we have covered in many of our previous reports, VLSFO prices do ultimately track crude prices.

Source: Integr8 Fuels

Source: Integr8 Fuels

From the graph above, there have been three distinct periods over the past 20 years when we have seen ‘low’ oil prices, where Brent fell below $50/bbl. The first period was in 2008/09 with the global economic crisis; the second was in 2015/17 with an oil supply glut; and the third, most recent period, was in 2020 with the global COVID-19 pandemic.

The first and last of these periods were driven by extreme global events that affected all industries and markets, prompting major interventions from OPEC — unlike in 2015.

OPEC has the power to raise & cut production

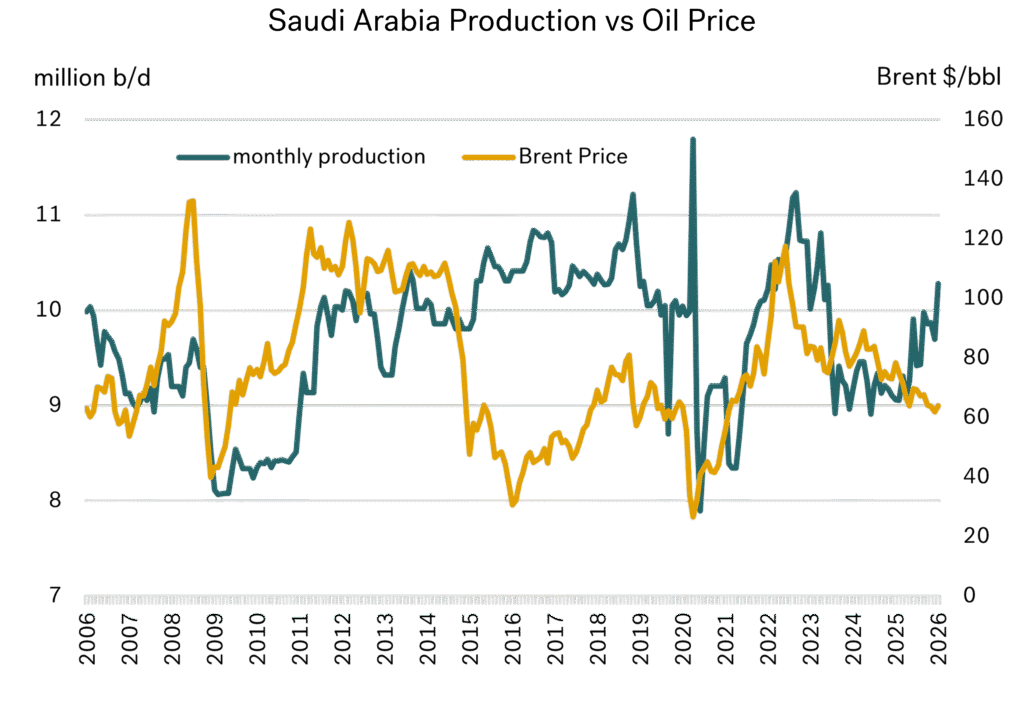

OPEC is the marginal supplier of oil in the industry and has shown a strong ability to respond and manage prices within a reasonable range. This means raising output if oil prices are going sky-high and damaging the global economy. It also means cutting production if prices are too low, which would then damage economies of the OPEC producers.

The core OPEC decision-making process has often been between the strong alliance of Saudi Arabia, UAE, and Kuwait. More recently, other producing countries have aligned themselves to OPEC, forming the OPEC+ group. For simplicity, this report focuses on Saudi Arabia’s response — as the most influential member of OPEC — rather than on the collective group.

In the 2008 global economic crisis and the 2020 global COVID-19 pandemic, OPEC clearly demonstrated their ability and willingness to manage oil prices. In 2008/09 when oil prices fell, Saudi Arabia cut production from 9.6 million b/d to 8.1 million b/d (a 15% fall) and as a result, oil prices rebounded from a $40/bbl low.

When crude prices hit $80/bbl Saudi Arabia (and OPEC) responded again, increasing production to 10 million b/d to prevent prices going sky-high. The same occurred in 2020 with the COVID-19 pandemic, prices collapsed and production was cut. As prices rebounded, the production taps were opened.

Source: Integr8 Fuels

Source: Integr8 Fuels

However, there was a noticeable difference in the 2015/17 oil supply glut. During this period, Saudi Arabia maintained production in the 10-11 million b/d range and prices only picked up gradually over the following two years to around $70/bbl, as oil demand increased and ate into the surplus.

The 2015/17 market is similar to the conditions we face today

The reason we have looked so carefully at 2015/17 is because it closely matches the situation we are in today, although this time around the potential supply-glut is led by low growth in world oil demand rather than a sharp increase in oil supply.

Current prices haven’t fallen to the $30-40/bbl lows of 2015/17, but they have been under downwards pressure and despite this, Saudi Arabia has raised production from 9.1 to 10 million b/d over recent months. This is obviously good news for bunker buyers, though not for oil exporters!

What will OPEC do?

There is a lot that goes on behind the scenes to decide whether OPEC cut or raise production. Saudi Arabia and others want to defend market share, so are unlikely just to keep cutting production, but they also need to protect revenue. So, what is a minimum level of production and a minimum level of revenue that Saudi Arabia is likely to work with.

As shown in the graph below, for almost all the past 20 years Saudi Arabia has produced between 9 and 10.5 million b/d. It is currently towards the high end of this range and so if pricing were to go ‘too low’, it is conceivable that Saudi Arabia could cut output by around 1 million b/d.

Source: Integr8 Fuels

Source: Integr8 Fuels

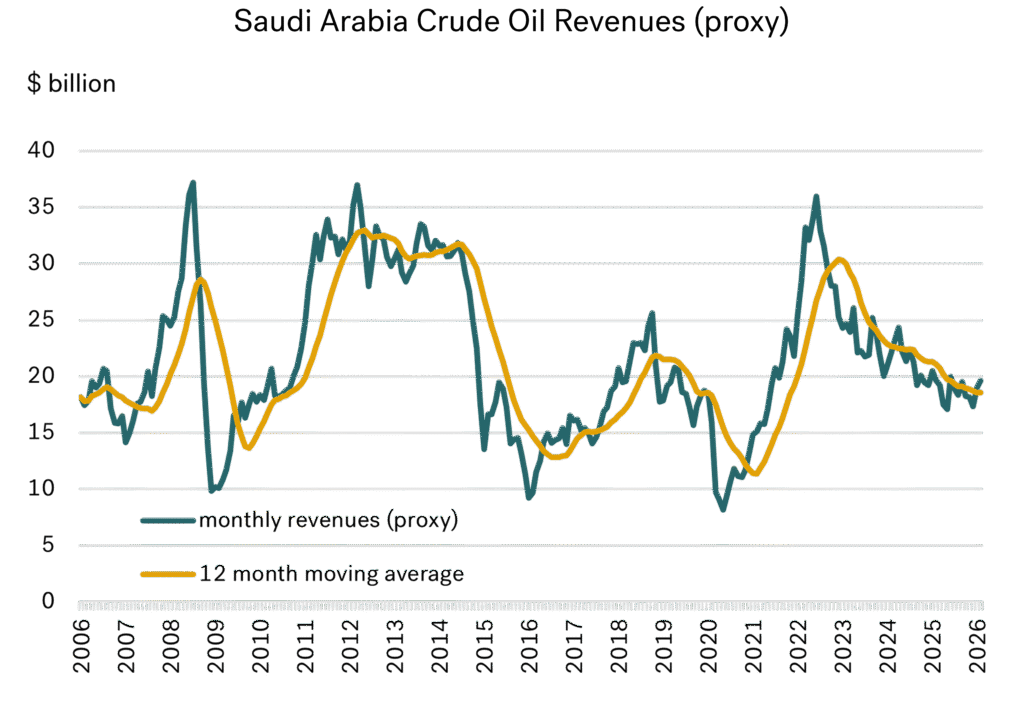

The following chart is a proxy to Saudi crude revenues, based on monthly production and an adjustment to monthly Brent prices (no adjustment for inflation is made). On this basis, it appears that $15 billion per month is the low end of the range. Over the past three years, revenues have fallen from a high of $30 billion per month however, they are still around $20 billion currently.

Source: Integr8 Fuels

Source: Integr8 Fuels

Given this, there is currently no pressing need for Saudi Arabia, or the rest of OPEC to push for production cuts and higher prices.

At what level could Saudi Arabia respond?

If Saudi Arabia continues to produce at around 10 million b/d and Brent prices are in the $60s or higher, then market share and revenues are unlikely to be an issue. If Saudi Arabia continues to produce at 10 million b/d and Brent prices fall to the mid $50s (as some analysts have forecast), estimated revenues would be at around $17 billion per month. This estimate sits towards the low end of the historic range, but may still be considered acceptable. It is only when Brent prices dip into the $40s that the revenue calculation is tested at the extreme lows of less than $15 billion per month. At this point, a change in strategy and production cuts could come about.

Based on this analysis, OPEC production at current levels and Brent prices in the $60s is unlikely to illicit an OPEC response to cut production and push prices higher. Even prices in the mid to high $50s could give OPEC an acceptable market share and an acceptable level of revenue. It is only when Brent prices fall to the low $50s that OPEC revenues would be squeezed. At prices in the $40s, revenues fall to historic lows (even before inflation is considered) and could trigger an OPEC response.

How low can bunker prices go before OPEC intervene

For those of us in bunkering, this could mean no OPEC response if Singapore VLSFO reaches $400/mt. If it reaches $350-375/mt on a sustained basis, then we should be wary of an OPEC response to cut production and raise oil prices. To summarise, at $300/mt prices we should expect OPEC to cut production and raise prices—until then, let’s monitor analyst theories and enjoy the current relatively low bunker prices.

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com

Posted by

Research Team

Latest articles

Contact our Experts

With 65+ traders in 13 offices around the world, our team is available 24/7 to support you in your energy procurement needs.