News March 19, 2026

Have bunker prices outpaced the rest of the oil market?

Last month we wrote about a floor to bunker prices: what next?

Last month’s report on a floor to oil and bunker prices seemed an appropriate topic at the time, and the conclusion was Brent in the $40s and VLSFO in the $300s. Four weeks later, it looks like the report is already redundant and can be shelved for the foreseeable future.

Events and ‘Trump-led’ politics have caused chaos. From a commercial perspective, the closure of the Strait of Hormuz means oil is at the forefront of developments across global markets, and we are in the thick of it.

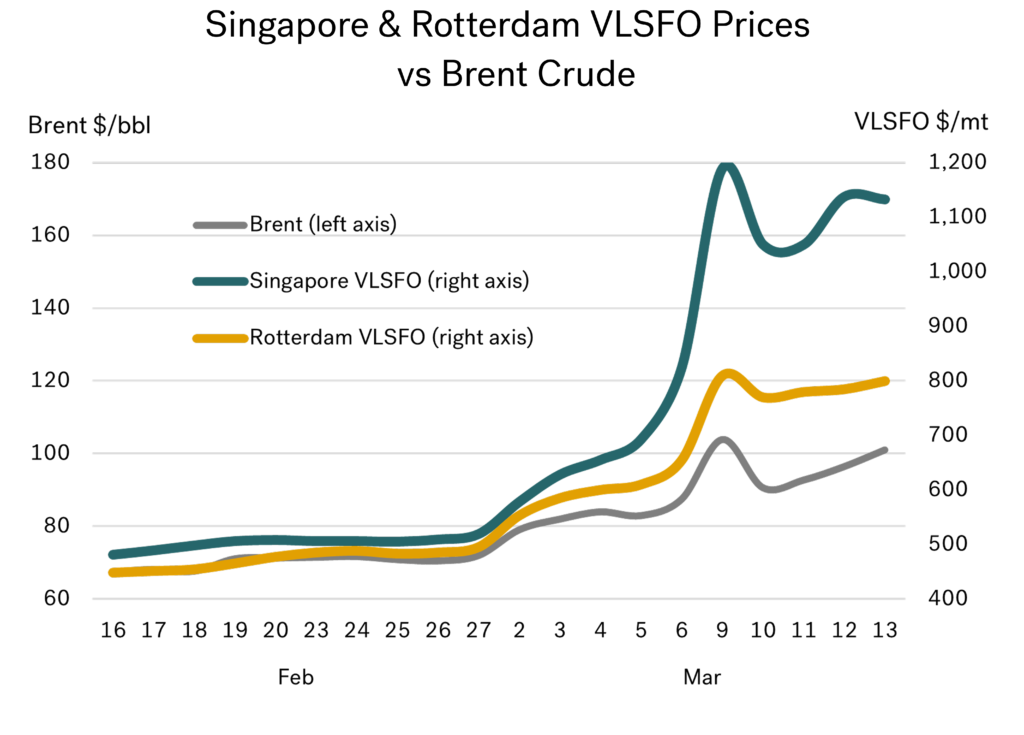

VLSFO up by more than crude, especially in Singapore

When it comes to headlines on oil pricing in the global media, it usually starts with crude, and then possibly gasoline. But behind the headlines, there is a lot more going on. The graph below (with left and right axes scaled the same) just about summarises everything for us in bunkers.

Headline Brent prices are just above $100/bbl, up by around $30/bbl (plus 45%) since the week before the war (although there was an intra-day high of $116/bbl on 9 March). However, bunker prices are up by significantly more than crude, with Rotterdam VLSFO prices up $340/mt and Singapore prices up a massive $635/mt, more than double their pre-war levels.

Source: Integr8 Fuels

Source: Integr8 Fuels

The outcome is clear, VLSFO prices have risen much higher than benchmark crude and the leap in Singapore VLSFO prices has been a lot more extreme than in Northwest Europe.

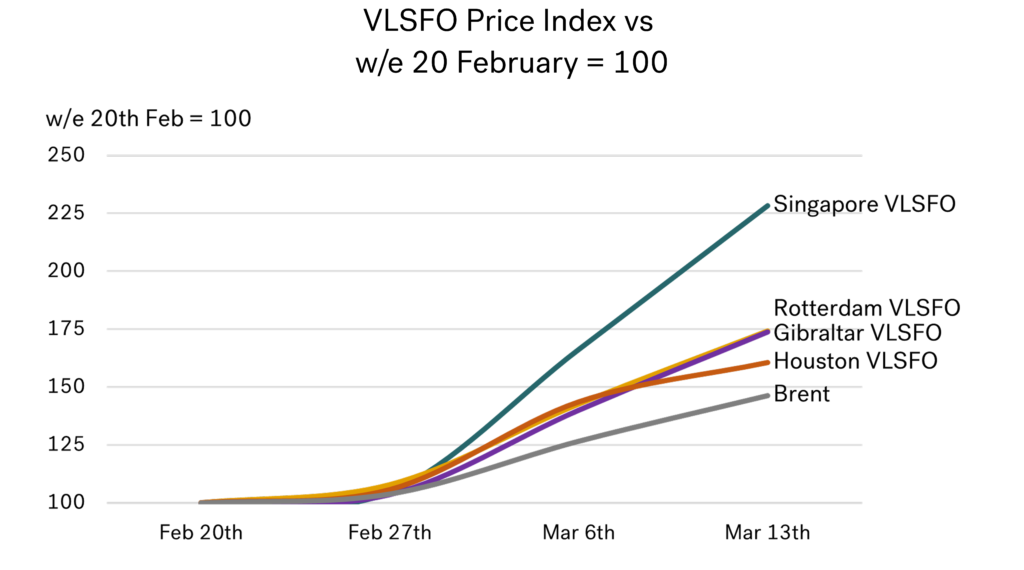

What has happened to VLSFO prices around the world?

The graph below looks at key regional VLSFO prices, indexed against their weekly average for 16–20 February (i.e. before any significant expectations of the start of US/Israeli attacks on Iran on 28 February). We have deliberately left the Middle East out of this analysis.

Source: Integr8 Fuels

Source: Integr8 Fuels

This shows that the main regional VLSFO price rises have been greater than for Brent crude, but the increase in US Gulf prices was less than in Europe, which in turn was significantly less than in Asia.

Looking more closely at what has happened to VLSFO prices around the world, there is a clear case that pricing pressures become more intensive as you move from west to east.

It’s the same for HSFO: price hikes bigger than crude, with Singapore at an extreme

The trend is the same for HSFO. All price increases are greater than for crude, and the increases get bigger as you move from the US Gulf to Europe and then on to Asia. In the US Gulf, again, HSFO prices are ‘only’ 65% higher than pre-war levels (plus $250/mt), whereas European markets are some 85% higher (plus $350/mt) and Singapore 100% higher than in mid-February (plus $425/mt).

Source: Integr8 Fuels

Source: Integr8 Fuels

The brief explanation is straightforward, as the majority of Middle East crude and product exports go east, and so a closure of the Strait affects Asian markets more than others. However, there are always knock-on effects that exacerbate the situation. In this case, an obvious tightening in Asian markets has meant China and India have responded by shutting down their product export markets in defence of their own domestic requirements.

This has therefore tightened Asian markets even further and created greater uncertainty about availabilities and pricing in the near term. If that is not enough, the squeeze on European markets and extremely high freight costs have meant the ‘normal’ product flows from Europe to Asia have also come to a halt.

It does not look easy for anyone buying bunkers right now, but if you must rank them, Asian pricing is suffering more.

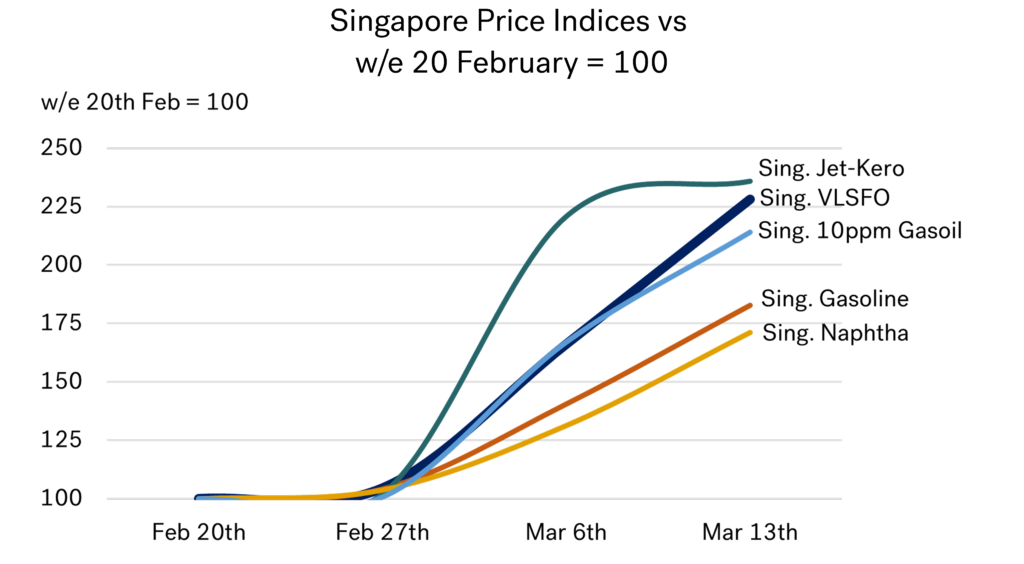

How does VLSFO compare with other products in Singapore?

There is no doubt that the jet fuel market has come under huge pressure. Significant jet export volumes come out of the Middle East, and the ability to ramp up production elsewhere in the world is severely limited. Jet is almost entirely a straight-run product out of the refinery, and the vast majority of the world’s spare capacity is located in the Middle East.

Hence, when the war started, there was a near-instantaneous spike in jet prices, with Singapore jet-kero quotes more than doubling in the first week of the war. However, in the second week, prices then more or less stabilised. It was in the second week that we in bunkers began to feel the same extreme pricing pressures, and this is when our market ‘ran away’.

So now, the Singapore VLSFO market is in the same bracket as the Singapore jet market (and the 10ppm gasoil market), where prices have more than doubled in just two weeks. It’s difficult to say that Singapore gasoline and naphtha markets have fared better, with price rises of around 75% in two weeks, but it’s all relative!

Source: Integr8 Fuels

Source: Integr8 Fuels

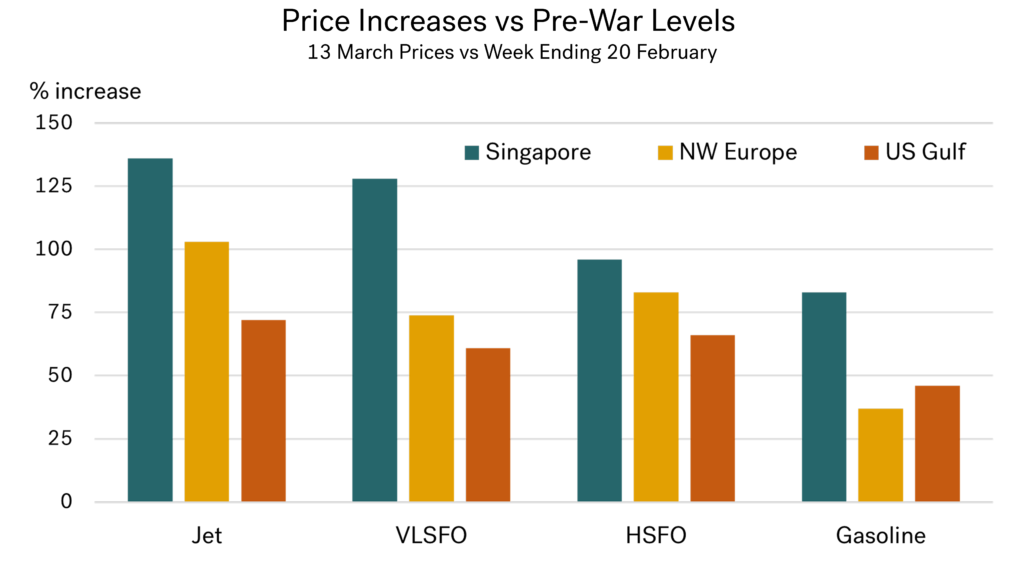

How have bunker markets fared in other international markets?

If we compare percentage price increases for bunkers against jet and gasoline over the first two weeks of the war, then the graph below illustrates that the biggest gains across these products have been in Asia, followed typically by Europe, and finally the US. It also shows that bunker price increases have been close to what is happening in the jet market, and higher than gasoline in

each of the main markets; we in bunkers have seen some of the biggest percentage price hikes in each region.

Source: Integr8 Fuels

Source: Integr8 Fuels

What is being done to ease prices?

There have been attempts to ease market pressures. The IEA has announced its biggest ever release of strategic stocks, at 400 million barrels. However, this can only help to a limited extent over a brief period. Also, a greater proportion of the release is in the West, whereas the greatest need is in the East. This raises further questions, such as whether there is a willingness, or even the ability, to trade these stocks to other countries and regions.

There are also talks to establish an international naval presence to protect shipping going through the Strait of Hormuz, although at the time of writing nothing had been finalised. There are further questions here about the willingness, the rates, and the insurance cover of merchant ships transiting the area.

Ultimately, it is only the resumption of Middle East oil production and refining operations, and the safe reopening of the Strait of Hormuz, that will bring prices down to more settled levels.

Let’s hope this report becomes redundant as quickly as the last one!

The time between writing, publishing, and reading this report can be an age in these chaotic times. Let’s hope this month’s report becomes redundant just as quickly as last month’s report looking at a floor to VLSFO prices in the $300s!

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com

Posted by

Research Team

Contact our Experts

With 65+ traders in 13 offices around the world, our team is available 24/7 to support you in your energy procurement needs.