News Today, 13 hours ago

The Week in Alt Fuels: HVO for the quality-conscious

Denmark

Sweden

Amsterdam

Antwerp

Dunkirk

Genoa

Hamburg

Helsinki

Le Havre

Ravenna

Rotterdam

Singapore

Tallinn

Venice

HVO can cost shipowners hundreds of $/mt more than FAME while doing roughly the same job towards emission regulations. Why would anyone bunker it?

IMAGE: EcoCeres and Mitsui delivered 400 mt of HVO to a cruise ship in Singapore earlier this year. EcoCeres

IMAGE: EcoCeres and Mitsui delivered 400 mt of HVO to a cruise ship in Singapore earlier this year. EcoCeres

In recent months, we have seen hydrotreated vegetable oil (HVO) been launched by bunker suppliers and tested by shipowners in various ports.

Shipowners can be extremely price sensitive, often opting for the cheapest fuel as long as it meets quality specifications and regulations, and takes their ships from A to B.

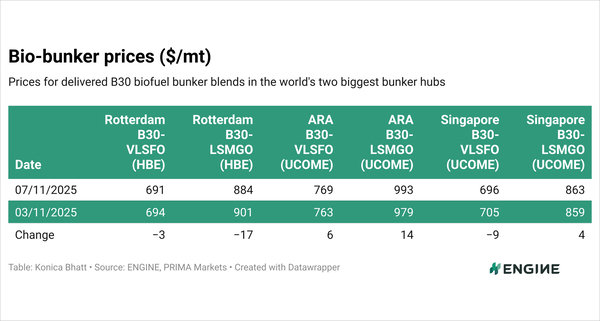

Burning a bit of biofuel can be the cheapest fuel alternative for ships trading in the EU for the first time this year. That’s fatty acid methyl ester (FAME) and not HVO, which we have seen priced 45-50% above FAME on an outright basis in ports like Rotterdam and Lisbon.

FAME and HVO are two categories of biofuels that are produced in different ways. FAME is produced through transesterification, a much cheaper production method than the hydrotreatment needed to produce HVO.

As FAME is considerably cheaper, HVO buyers will have to justify the extra costs by passing on these costs to cargo owners, passengers, governments, cities or port authorities – eventually consumer and citizens.

More bang for your buck?

HVO100 (100% HVO) has been priced about $560/mt higher than B100 (100% FAME) on an outright basis in Rotterdam.

HVO has a 19% greater default energy density than FAME in EU regulations, but that alone doesn’t justify its higher price for a bunker buyer. Adjusted for energy, Rotterdam’s HVO100 price premium over B100 narrows, but only to about $320/mt.

Both HVO and FAME count as zero-emission fuels in the EU Emissions Trading System (EU ETS), which means that you don’t pay to burn them.

In FuelEU Maritime, it’s the greenhouse gas (GHG) intensity that counts and you want it to be as low as possible to build valuable compliance surpluses. HVO can actually have a greater GHG intensity than FAME. If they are both produced from used cooking oil (UCO), HVO’s default GHG intensity in FuelEU Maritime is 5% higher than FAME’s.

With FuelEU and EU ETS emission costs and pooling values included, HVO100 is still a more expensive fuel than B100. Ships bunkering HVO100 in Rotterdam will pay about $210/mt more than they would have for B100 when the fuels are consumed between two EU ports this year, according to our calculations.

So HVO’s superior energy density goes some way to reduce its price premium over FAME for ships burning them in the EU, but it doesn’t close the gap.

When quality is king

For shipowners looking beyond outright price tags and EU emission costs, HVO can have a leg up in how it performs.

Unlike FAME, HVO is fully miscible with diesel and gasoil and can be used as a true drop-in fuel with fewer logistical and fuel quality concerns than FAME. It can be carried by normal bunker tankers up to 100%, whereas FAME has a 30% limit in most ports unless you carry it on an inland barge (ARA) or an IMO Type II chemical tanker (Singapore).

HVO has superior cold flow properties and a longer shelf-life than FAME, which can help justify it for ships in colder or more challenging conditions, like for Arctic voyages or navy vessels. It can also work as a low-emission pilot fuel for dual-fuel LNG, methanol and ammonia vessels.

Testing and supplying

Italian supplier Enilive just launched HVO bunker supply in the ports of Genoa and Ravenna, with Venice expected to follow suit by the end of the year. All three of these are cruise ports.

Last summer, Hamburg Port Authority’s fleet manager Flotte Hamburg said it would test HVO100 on three of its vessels before rolling it out across the Hamburg fleet. The HVO would be produced by Shell and delivered by German marine fuel supplier Friedrich G. Frommann. The port authority said the HVO meets the sustainability criteria in RED II – which cheaper FAME also does – and that it was looking for a low-emission biofuel option for vessels that can’t be electrified.

Finnish ferry operator Eckerö Line announced in April that it would buy HVO from Neste to make ferries running between Helsinki and Tallinn compliant with FuelEU Maritime’s 2% GHG reduction target – which FAME also does.

Also in April, EcoCeres and Mitsui announced they had delivered their first HVO stem in Singapore. A cruise ship bunkered 400 mt of HVO and they cited emission reductions as a reason for going for HVO.

The HVO bought in these three cases will no doubt have come with higher costs than FAME, despite both biofuel types doing the job towards emission reduction targets in the EU and elsewhere.

Dropping in and passing on costs

HVO’s flexibility in dropping smoothly into gasoil-powered ships is likely a factor for them. So is proximity to end consumers and citizens who might more willingly foot the extra fuel bill. Hamburg Port Authority is owned by the City of Hamburg, while Eckerö Line and cruise ships carry paying passengers.

An ARA bunker supplier says it is mainly cruise companies that opt for more expensive HVO over FAME. It’s “just the ones that want the best quality,” the supplier said. In one situation, a cruise company looking for biofuels had a very specific engine that could only take HVO because it was much smaller than a usual engine. That way the cruise ship could fit a couple of extra rooms for passengers.

But the supplier has generally seen very little HVO demand this year. It has just been one inland vessel, a couple of tankers and a few dredging vessels, in addition to the cruise ships.

A Scandinavian bunker supplier has not taken note of any specific vessel type taking HVO instead of FAME, but stresses that HVO’s drop-in flexibility can make it attractive. It can blend directly with gasoil onboard without any quality concerns.

In other news this week, CMA CGM ordered 10 LNG dual-fuel container ships that will mostly call at the two French Atlantic coast ports of Dunkirk and Le Havre. LNG continues to feature prominently in alternative fuel-capable vessel orders. 26 of 30 vessels added to the global orderbook were LNG dual-fuel in October, according to DNV data.

Maersk has taken delivery of the Brussels Mærsk, its 18th methanol-capable dual-fuel container vessel. Hercules Tanker Management launched the first in a series of three tankers capable of supplying methanol and B100 biofuel. The tanker Harriet will be time-chartered to bunker supplier Peninsula, which has the same management as Hercules.

By Erik Hoffmann

Please get in touch with comments or additional info to news@engine.online

Provided by

Latest articles from the region

Contact our Experts

With 50+ traders in 12 offices around the world, our team is available 24/7 to support you in your energy procurement needs.