News 5 days ago

East of Suez Market Update 25 Jun 2025

Busan

Daesan

Fujairah

Onsan

Singapore

Ulsan

Yeosu

Zhoushan

HSFO

LSMGO

VLSFO

Prices in East of Suez ports have moved in mixed directions, and availability across all grades is good in several South Korean ports.

Changes on the day to 17.00 SGT (09.00 GMT) today:

- VLSFO prices up in Fujairah ($11/mt), Zhoushan ($9/mt) and Singapore ($2/mt)

- LSMGO prices up in Zhoushan ($16/mt), unchanged in Fujairah and down in Singapore ($6/mt)

- HSFO prices up in Singapore ($1/mt), and down in Fujairah ($8/mt) and Zhoushan ($5/mt)

- B24-VLSFO at a $159/mt premium over VLSFO in Singapore

- B24-VLSFO at a $145/mt premium over VLSFO in Fujairah

Fujairah’s VLSFO price has increased by $11/mt in the past day — the sharpest rise among the three major Asian bunker ports. This uptick was supported by a higher-priced 150–500 mt VLSFO stem recently fixed in the port. As a result, Fujairah’s VLSFO discount to Singapore has been erased, while its discount to Zhoushan has narrowed to just $6/mt.

VLSFO availability in Fujairah has tightened, with recommended lead times rising to about nine days, up from 5–7 days last week. Most suppliers are reluctant to commit to large volume stems due to ongoing market volatility driven by the Middle East conflict and cargo shortages. Premiums are being added for larger stems, according to a trader.

LSMGO and HSFO lead times remain around seven days, unchanged from the previous week. While some prompt deliveries are possible, they are typically offered at a premium.

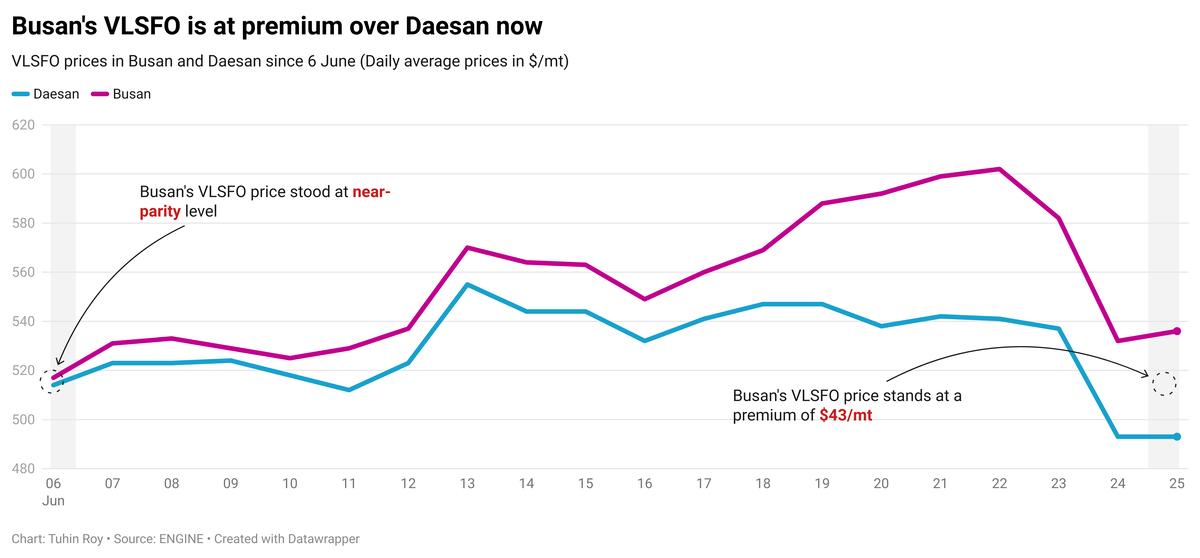

In South Korea, VLSFO is now being priced at a premium of $43/mt in southern ports like Busan compared to western ports such as Daesan — a steep rise from the $3/mt spread at the start of June. A source attributes this to supplier efforts to raise prices ahead of July, following weaker levels earlier in the month. However, the price surge has curbed demand, with many bunker buyers turning to nearby Chinese ports like Zhoushan.

Lead times across multiple South Korean ports have improved, now averaging 5–6 days, compared to the 5–10 days advised last week.

Weather-related disruptions are expected to impact bunker operations: Ulsan, Onsan, Busan, and Yeosu may face delays due to high waves from 29 June-1 July, while Daesan and Taean are likely to see interruptions from swells between 30 June-1 July.

Brent

The front-month ICE Brent contract has moved $1.16/bbl lower on the day, to trade at $68.02/bbl at 17.00 SGT (09.00 GMT).

Upward pressure:

Brent futures have gained some support following the American Petroleum Institute's (API) weekly oil inventory report.

US crude oil inventories declined by 4.28 million bbls in the week ending 20 June, according to API estimates.

The decline in crude stocks surprised market analysts, who expected a much smaller draw of 600,000 bbls. The numbers were “significantly above the anticipated decrease of around 0.6 million barrels,” two analysts from ING Bank noted.

A decrease in US crude stockpiles generally signals stronger demand and can provide some support to Brent's price.

Market participants now await the US Energy Information Administration’s (EIA) crude inventory report, scheduled for release later today.

Downward pressure:

Brent’s price has plunged as some geopolitical risk premiums have been priced out of the oil market, according to analysts.

US President Donald Trump said on Truth Social yesterday that China can continue purchasing oil from Iran, following the successful implementation of a ceasefire between Israel and Iran, according to a Reuters report. Meanwhile, the White House clarified that the statement did not indicate a relaxation of US sanctions against Iran.

“With the Israel-Iran ceasefire holding steady, oil’s risk bid collapsed,” SPI Asset Management managing partner Stephen Innes said.

Given that the tensions between Israel and Iran remain contained in the upcoming weeks, market attention is expected to shift back to the anticipated supply surplus later this year.

“The latest slump in prices brings the market back to where it was before Israel attacked Iran on 12 June,” ANZ Bank’s senior commodity strategist Daniel Hynes remarked.

“OPEC is scheduled to ramp up output in July faster than originally agreed,” he added. The group is due to meet on 6 July to discuss a further supply boost in August.

By Tuhin Roy and Aparupa Mazumder

Please get in touch with comments or additional info to news@engine.online

Provided by

Latest articles from the region

Contact our Experts

With 50+ traders in 12 offices around the world, our team is available 24/7 to support you in your energy procurement needs.