News 2 days ago

East of Suez Market Update 16 Jun 2025

Fujairah

Hualien

Kaohsiung

Keelung

Singapore

Taichung

Zhoushan

HSFO

LSMGO

VLSFO

Prices in East of Suez ports have moved down, and VLSFO and LSMGO availability has tightened in Zhoushan.

IMAGE: Night scene of Zhoushan, close to the dock on Putuo island. Getty Images

IMAGE: Night scene of Zhoushan, close to the dock on Putuo island. Getty Images

Changes on the day from Friday, to 17.00 SGT (09.00 GMT) today:

- VLSFO prices down in Fujairah ($19/mt), Zhoushan ($9/mt) and Singapore ($8/mt)

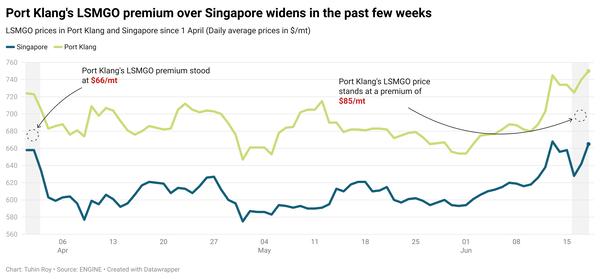

- LSMGO prices down in Singapore ($65/mt), Zhoushan ($49/mt) and Fujairah ($44/mt)

- HSFO prices down in Singapore ($24/mt), Zhoushan ($19/mt) and Fujairah ($9/mt)

- B24-VLSFO at a $177/mt premium over VLSFO in Singapore

- B24-VLSFO at a $212/mt premium over VLSFO in Fujairah

Fujairah’s VLSFO price has dropped by $19/mt over the weekend — the sharpest decline among the three major Asian bunker ports. A lower-priced 500–1,500 mt VLSFO stem recently fixed at the port has contributed to drag the benchmark down. As a result, Fujairah's VLSFO discounts to Zhoushan and Singapore have widened by $10/mt and $11/mt, reaching $27/mt and $21/mt, respectively.

Prompt bunker availability in Fujairah remains tight, with lead times for all fuel grades holding steady at 5–7 days.

In Zhoushan, VLSFO supply has tightened, as several suppliers are running low on stock and replenishment cargoes have been delayed, according to a source. Lead times for VLSFO have increased from 4–7 days last week to around ten days now. LSMGO lead times have also risen sharply, from 2–3 days to about ten days now. Conversely, HSFO lead times in Zhoushan have improved, decreasing from 4–7 days to 3–5 days.

In Taiwan, recommended lead times for both VLSFO and LSMGO are around three days in Taichung and Kaohsiung. Supplies remain stable in Hualien and Keelung, with lead times unchanged at approximately two days.

Brent

The front-month ICE Brent contract has declined by $0.61/bbl on the day from Friday, to trade at $73.63/bbl at 17.00 SGT (09.00 GMT).

Upward pressure:

Brent crude’s price has gained some upward momentum over the weekend as the simmering conflict between Israel and Iran quickly escalated, with the former targeting Tehran’s oil and gas facilities.

Over the weekend, Israel struck two key energy facilities near Tehran – Shahran fuel depot and the Shahr Rey oil refinery. The strikes have caused a series of explosions, according to media reports. Both the facilities were among the largest oil infrastructure sites in Iran.

“This marks a dramatic escalation in the conflict that has hung over the oil market since Hamas attacked Israel about 20 months ago,” ANZ Bank’s senior commodity strategist Daniel Hynes remarked.

Iran also retaliated with a barrage of drones and missiles towards multiple Israeli cities including the Haifa oil refinery in northern Israel. “The risk that this conflict will impact flows of crude oil rose significantly over the weekend,” Hynes added.

Downward pressure:

Additional supply from OPEC+ producers such as Saudi Arabia and the UAE could help cushion the market against short-term supply disruptions, according to market analysts.

“OPEC sits on 5m b/d [5 million b/d] of spare production capacity, and so any supply disruptions could prompt OPEC to bring this supply back onto the market quicker than expected,” two analysts from ING Bank noted.

Earlier in June, the oil producers’ alliance agreed to raise output by 411,000 b/d for July, maintaining the same monthly increase it has implemented consistently for the past three months.

Market watchers will closely review the upcoming OPEC oil market report, due later today, for fresh insights into the group’s supply and demand outlook.

By Tuhin Roy and Aparupa Mazumder

Please get in touch with comments or additional info to news@engine.online

Provided by

Latest articles from the region

Contact our Experts

With 50+ traders in 12 offices around the world, our team is available 24/7 to support you in your energy procurement needs.