News September 28, 2023

Bunker prices were high last month; they are even higher today. What is driving prices & how quickly can

they fall?

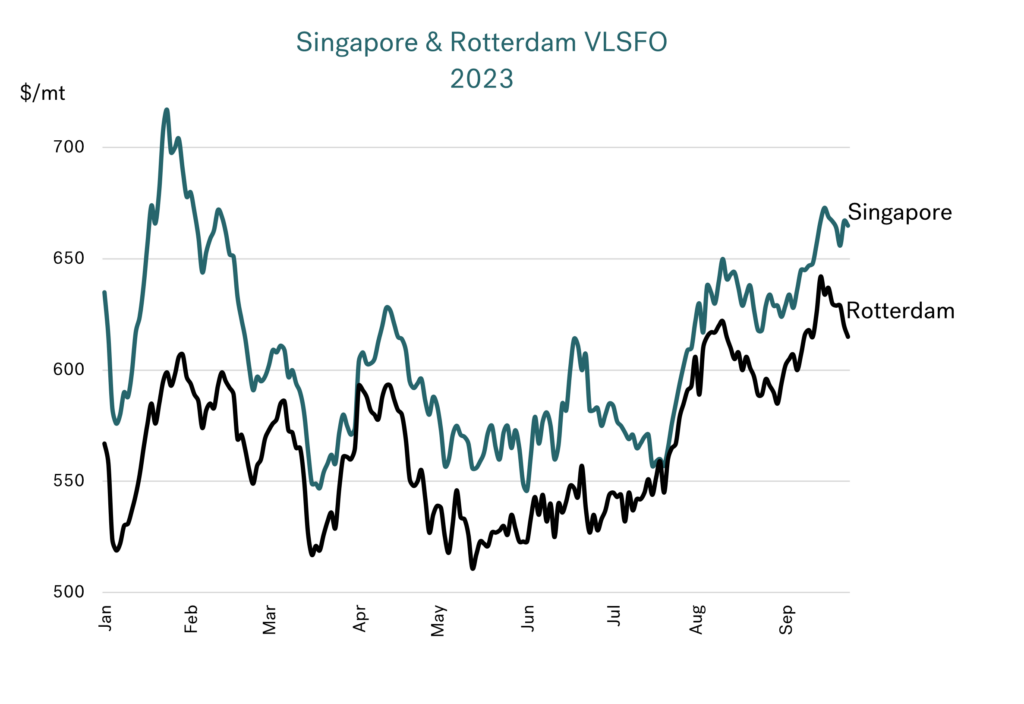

VLSFO prices have been on another rise

A month ago, we wrote about high bunker prices which were based on two key factors: Tightness in most product markets; And additional oil production cutbacks by Saudi Arabia. Now, bunker prices are even higher.

Brent has moved above $90/bbl, with Singapore VLSFO above $660/mt and close to peak levels seen at the start of this year. Rotterdam VLSFO has been trading at around $615-635/mt, its highest so far this year. More recently Rotterdam prices have eased slightly but they are still above this year’s previous peaks, and Singapore prices remain at high levels.

Source: Integr8 Fuels

Much tighter fundamentals are behind the price hike

On a very short-term basis, the market can see dramatic price shifts, but it is normally the fundamentals that drive price direction over a period of weeks and months. We are now in a strong fundamental period, with year-on-year growth in global oil demand at 3 million b/d in Q2 this year and projected at 2 million b/d in Q3 and Q4. The key factor here is growth is almost entirely centred on China.

At the same time there are huge constraints in oil supply, with the additional 1 million b/d voluntary cut made by Saudi Arabia, starting in July. In fact, part of the recent price hike is that Saudi Arabia has recently committed to extending these additional cuts through to the end of this year. Additionally, the September 21st announcement by Russia which banned all diesel and gasoline exports to support their own domestic market and, we can see clear reasons why oil prices have taken another leap higher over the past month.

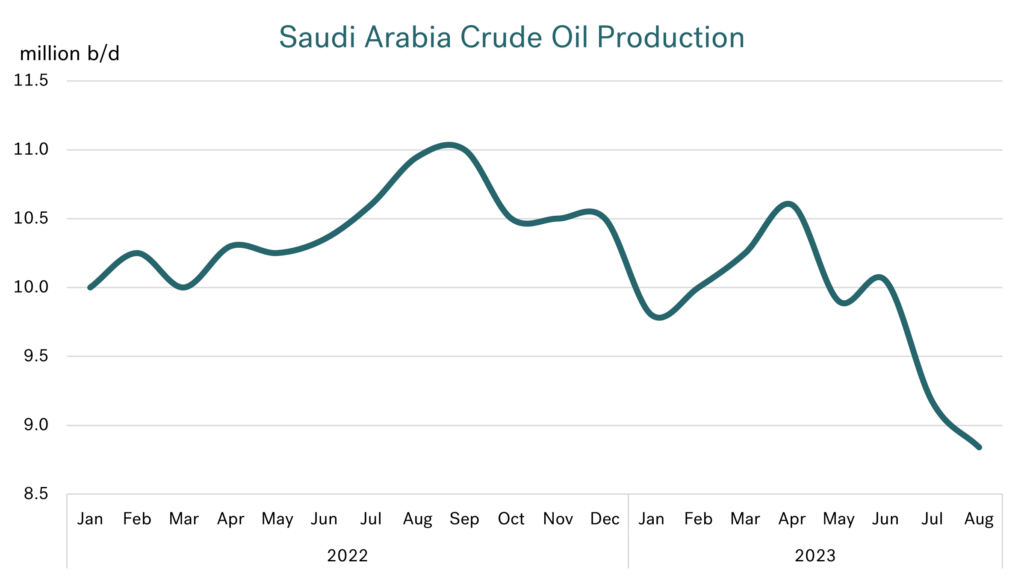

On the supply side, it is what’s happening to Saudi oil production

Saudi Arabia’s stated policy is aimed at supporting a market with less volatility, and more sustainable and predictable outcomes. As part of this strategy, the country had reduced crude output by 0.5 million b/d in line with the overall OPEC+ agreement, and then made a further 1 million b/d cut over the second half of this year. The net result is that Saudi crude production has fallen sharply over the past few months and is currently some 1.5 million b/d lower than average 2022 levels (8.9 million b/d in August vs an average of 10.4 million b/d last year). This lower level of output is expected to be maintained through to the end of the year.

Source: Integr8 Fuels

Source: Integr8 Fuels

Looking at alternative crude supplies, US production crude production is near record highs and higher oil prices has incentivised even greater investment in US shale oil. However, the problem here is Saudi cuts are instantaneous and any rise in US shale production from new investment takes months. Hence, current signals are for a potential tightness in supply over the rest of this year, before an expected 1 million b/d hike in January as Saudi crude output climbs back towards 10 million b/d.

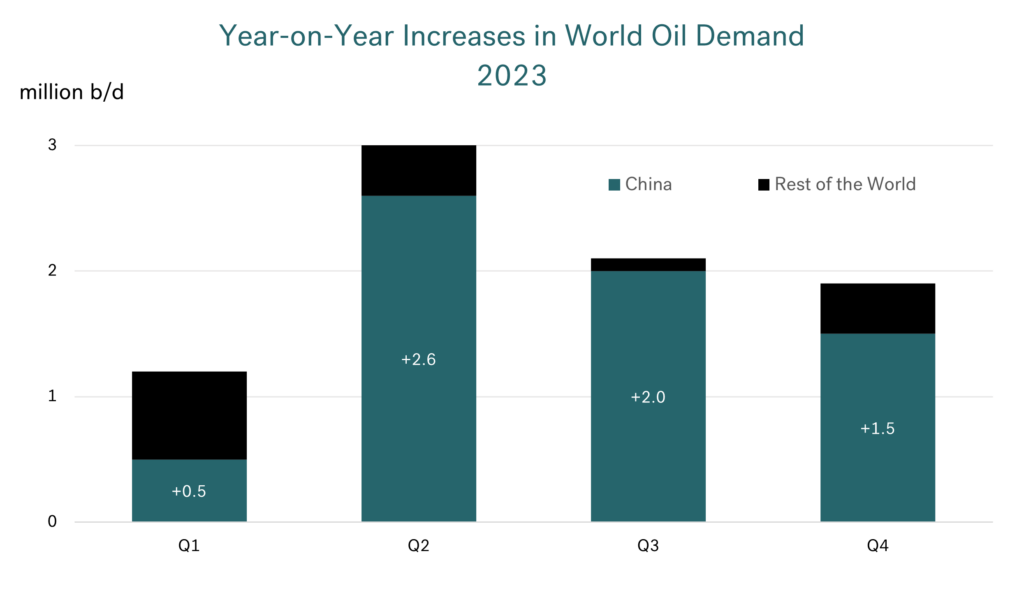

On the demand side it is all about China, China, China

Fundamentals on the demand side also point to higher oil prices. As mentioned, increases in global oil demand are running at 2-3 million b/d (year-on-year), and these are big numbers. However, they are almost entirely based on what is happening in China; product demand developments elsewhere are minimal, and even falling in Europe and projected to start falling in the US next year

The reason for current very high year-on-year growth rates in China is that the country was still largely in lockdown through 2022, and the easing has only taken place this year. This is much later than almost all other countries worldwide, where the post-pandemic ‘boom’ took place in 2022, not 2023. Therefore, it is more-or-less China alone that is driving up oil demand this year.

Source: Integr8 Fuels

Clearly there is a risk of weaker demand than forecast in many countries but if we are looking for a big price impact from the demand side, then it is more likely to be stories about China that are going to drive prices up or down.

Market tightness in Q3 & Q4, but potentially changing going into 2024

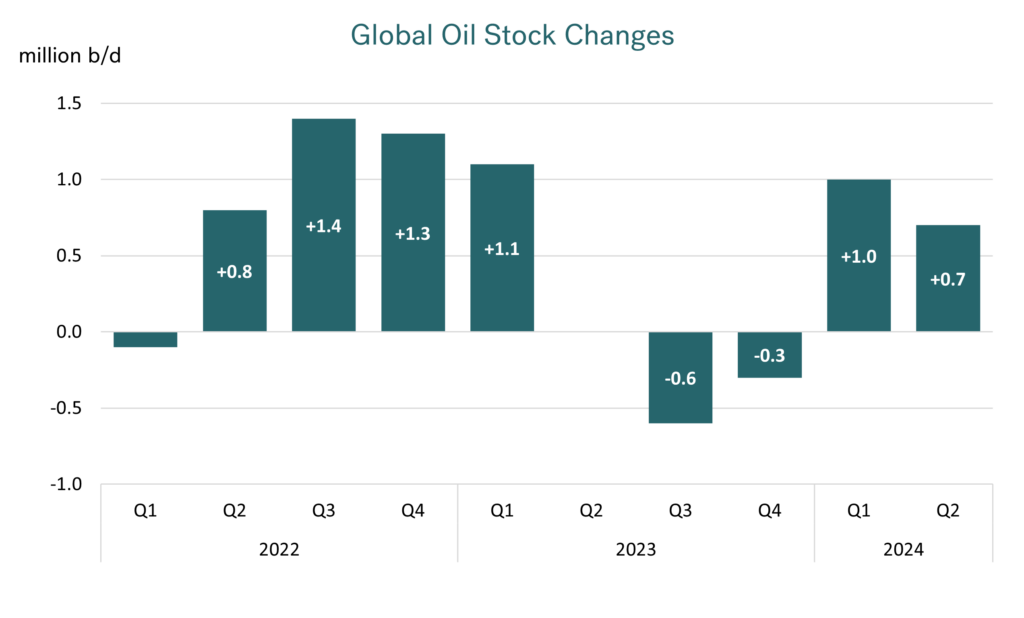

Bringing together these more extreme developments in supply and demand, the graph below illustrates global fundamentals on a quarterly basis. The key for us is that global oil supply exceeded demand through most of 2022 and in the first quarter of this year, resulting in an ongoing global stock build. However, we have just been through a turning point, where demand is exceeding supply in Q3 this year and this is expected to be repeated in Q4, leading to stock draws.

Source: Integr8 Fuels

It is not until the start of next year that we see a reversal and another turning point is envisaged. It is at this stage; Saudi Arabia says it will lift its voluntary 1 million b/d cutbacks. At the same time year-on-year growth in oil demand is expected to ease back to around 1 million b/d. So, at the start of next year oil supply is projected to exceed demand once again, reverting us back to a world of stock builds.

Summarising by looking at the global stock build/stock draw positions, we can see the exceptional times we are currently in; Having moved to a position of stock draws in Q3 and projected for Q4 this year. In addition, the tightness in global stocks lies with oil products, and not crude oil. This has been driven by high product demand and exacerbated by several unplanned refinery outages this year.

Source: Integr8 Fuels

Going into next year the position looks like reversing again, going back to a fundamental global stock build.

What’s next?

Given the fundamentals, these developments explain the wave of price rises we have seen in September.

Looking ahead over the rest of this year and into 2024, on the demand side China is the main story. Of course, Chinese demand could be higher than currently projected, in which case Brent crude could easily pass the $100/bbl ‘barrier’, along with Singapore VLSFO going above $700/mt. However, the chatter at the moment is about weakness in the Chinese economy. If this translates to lower oil demand, then it will be a sign ‘to sell’, and prices for us all would come down. This is clearly the story to watch on the demand side.

The supply side seems more predictable – When Saudi Arabia announces the additional cutbacks will be eased (or there are strong indications of this), then oil prices are likely to fall. A reversal of the Russian ban on diesel and gasoline exports could also have a bearish impact.

Timing is everything in all these developments, and the extent of any fall in prices may still be dependent on how tight oil product stocks are at the time and what stocks look like doing in the near term.

Being precise on price movements is difficult, but we know prices never wait for the fundamentals to be borne out; Markets react on news, changes, and psychology. If the fundamentals do play out as shown in this report, then prices are more likely to fall before the end of the year, in anticipation of weaker fundamentals going into 2024. Let’s see what happens….

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com

Posted by

Integr8 Research

Latest articles

Contact our Experts

With 65+ traders in 13 offices around the world, our team is available 24/7 to support you in your energy procurement needs.