News June 24, 2026

As Oil Markets Stabilise, Singapore VLSFO Remains the Outlier

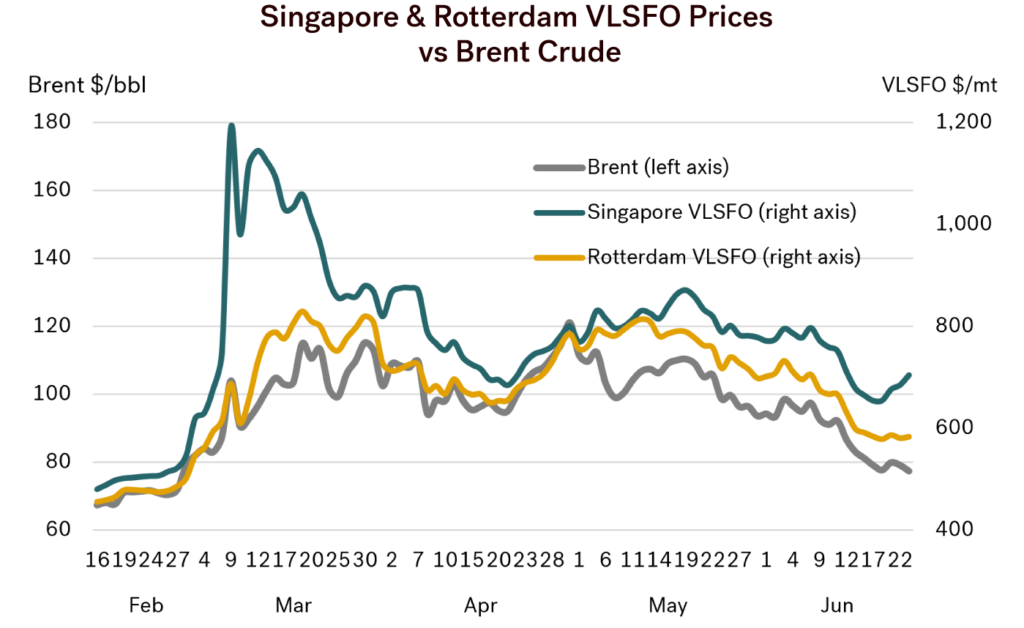

Crude prices close to their ‘lows’

A US-Iran MoU is in place and negotiations are underway. The path was never going to be smooth, and Israeli attacks on Lebanon at the very start of the process highlight the challenges ahead. However, the initial talks on ending the war and allowing future nuclear inspections are encouraging. The latest Brent and WTI crude futures markets appear to have more or less priced in a conclusion to the war and the reopening of the Strait of Hormuz. Prices may fall a little further on positive headline news, but from here the downside potential looks relatively limited.

Front-month Brent was trading at around $77/bbl at the time of writing, down from $105/bbl just over a month ago and a peak of $124/bbl at the end of April. We have come a long way from those highs, and there was never an expectation that prices would return to the monthly average Brent levels in the $60s seen during the 11 months from April 2025 to February 2026.

Source: Integr8 Fuels

Where are we with Singapore and Brent VLSFO pricing?

At this stage it appears that Rotterdam VLSFO prices are largely tracking the decline in front month Brent, but with a slight premium versus crude. There may be some room for this to ease a bit more, but not by much. To take Rotterdam VLSFO prices much lower we will need another drop in crude prices.

The situation in Singapore is different. Singapore VLSFO prices were falling, but have then risen over the past few days and are now at a very strong premium to crude. It may take a while, but this premium is expected to erode as oil markets stabilise and ‘get back to normal’. There seems to be more room for Singapore VLSFO to fall than for Rotterdam.

How the market is now looking at Brent crude futures

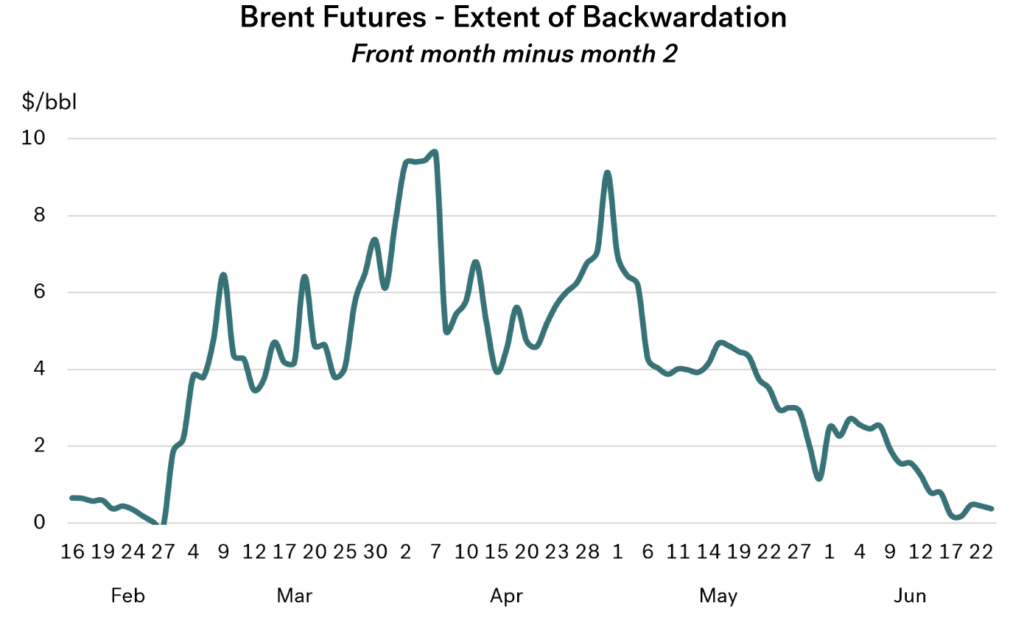

Obviously, war, uncertainty and the loss in supply have driven the whole oil price complex much higher. At the same time, pressures in physical supplies and also in near month futures prices have created a more extreme level of backwardation in price structures. This reflects the immediate tensions, and the sentiment at any given stage. In the graph below we have illustrated this by showing the price premium for front month Brent futures versus the second month price.

This shows the level of backwardation in this market climbed from less than $1/bbl just before the war, to anywhere between $4-10/bbl during March and April. Since then, backwardation has eased as expectations moved towards a peace agreement. Now it looks like an agreement will soon be in place, and backwardation has reverted back to pre-war levels. In fact, there is only around $0.40/bbl backwardation each month through to June next year. This is a very flat outlook, and not a sign of huge pressure.

Also, although it is not a forecast, and only the level at which people are prepared to trade, the current futures price for Brent a year ahead (June 2027 contract) is at $73/bbl, which is only $4/bbl below current prices.

Source: Integr8 Fuels

Given limited room for crude, how much further can VLSFO prices fall?

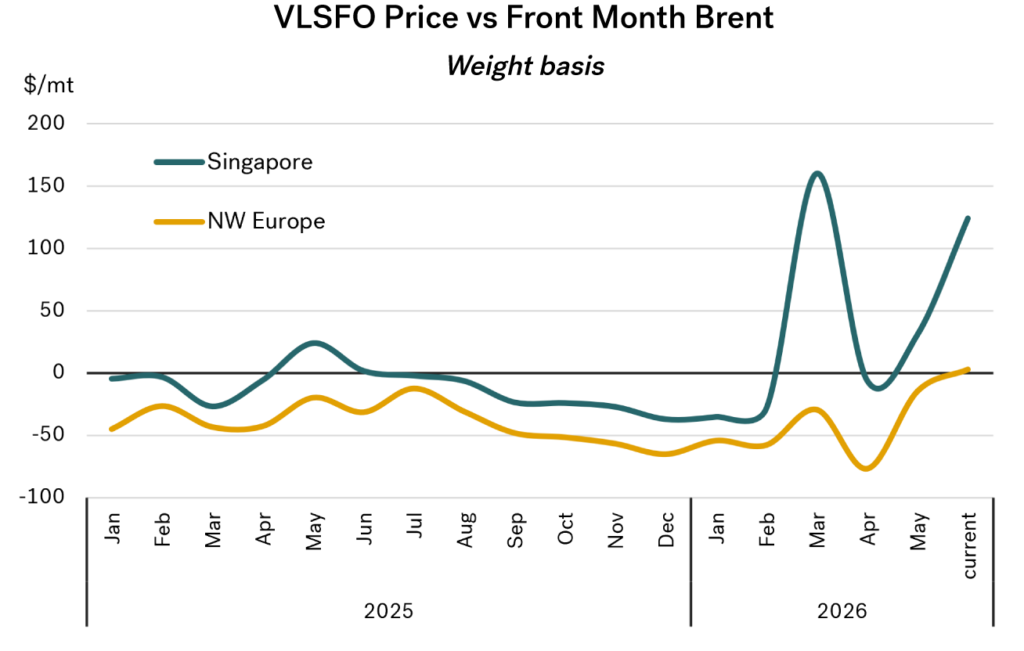

In last month’s report we highlighted the pressures on refining and the massive hike in overall margins that this war has triggered. The graph below takes this one step further, looking at VLSFO prices versus front month Brent. The measurement is adjusted to a weight basis and shown in terms of $/mt.

Source: Integr8 Fuels

This shows Singapore VLSFO prices had been running at around $25/mt below Brent equivalent, but at the start of the war surged to a $150/mt premium to crude. Although there was then a dip, current Singapore VLSFO prices have again increased, and are now $125/mt above Brent.

In contrast, Rotterdam VLSFO prices have moved from a typical $50/mt discount to Brent to a near equivalence today. This does show the disproportionate pressures that hit the Singapore VLSFO market at the start of the war, and also today. It also illustrates there is far more room for Singapore VLSFO prices to fall than for Rotterdam prices.

Assuming a complete (or near complete) opening of the strait of Hormuz takes place, these price relationships can be expected to ease as we get back to a more ‘normal’ flow of crude and product exports from the Middle East.

It is unlikely to be immediate, but even if crude prices were to remain at close to current levels, we would expect Singapore VLSFO prices to fall by around $125-150/mt over time, and Rotterdam prices by around another $25-50/mt as product premiums diminish.

So, even without any further fall in crude prices, once trade via the strait normalises, and international markets become more balanced, we could see Singapore VLSFO at $550-575/mt, and Rotterdam prices just below $550/mt.

A basic guide to consider future VLSFO pricing

There are always caveats around such statements. The starting point is that a strong and successful peace agreement would need to be in place, along with the free flow of traffic through the Strait.

There are a wide range of views on crude oil prices for the rest of this year. Some commentators are still carrying relatively high Brent forecasts at well above $85/bbl, although these are likely based on expectations formed before the latest round of US-Iran agreements and negotiations. Other commentators are looking for Brent to fall back into the $60s, driven by a rapid build-up in global oil inventories and lower expectations for oil demand following the war.

A more balanced view, however, is perhaps aligned with Goldman Sachs, which sees Brent trading in the $70–75/bbl range further out.

This feels like a good place to start the analysis. It is always easier to begin with a working assumption and then assess how the market evolves from there. This approach allows us to adjust price views as negotiations progress (or stall), as the practical realities of reopening the Strait of Hormuz unfold, and as the level of confidence in any agreement becomes clearer.

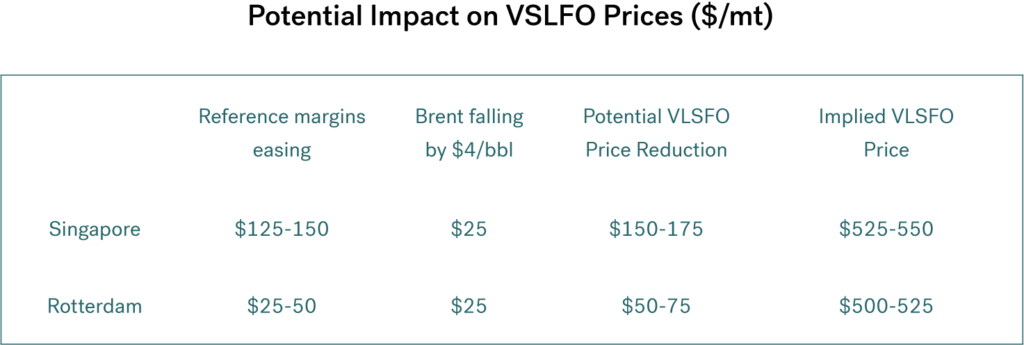

Using expectations that VLSFO prices will ease relative to crude, and that crude prices could edge down by a further $4/bbl over the rest of this year and into next, we could be looking at Singapore VLSFO prices around $150–175/mt lower than current levels, and Rotterdam VLSFO around $50–75/mt lower.

Source: Integr8 Fuels

The conclusions look good; we just need reality to follow suit!

This scenario could look quite favourable, but it does rely on a number of positive assumptions embedded within the price outlook. The most useful way to frame it is to keep the two elements separate. First, are markets likely to rebalance fairly quickly? If so, we would expect product prices to ease and refinery margins to come down. Second, could crude prices fall further? This could happen if the US and Iran are able to reach a more durable agreement through ongoing negotiations, potentially bringing an end to the conflict and even, in time, easing sanctions on Iran.

For now, we can only wait and see.

Steve Christy

Research Contributor

E: steve.christy@integr8fuels.com

Posted by

Elaina Cameron

Latest articles

Contact our Experts

With 65+ traders in 13 offices around the world, our team is available 24/7 to support you in your energy procurement needs.