News 6th Sep, 2024

East of Suez Market Update 6 Sep 2024

Busan

Daesan

Fujairah

Onsan

Singapore

Ulsan

Yeosu

Zhoushan

HSFO

LSMGO

VLSFO

Prices in East of Suez ports have moved in mixed directions, and HSFO availability remains good across several South Korean ports.

Changes on the day to 17.00 SGT (09.00 GMT) today:

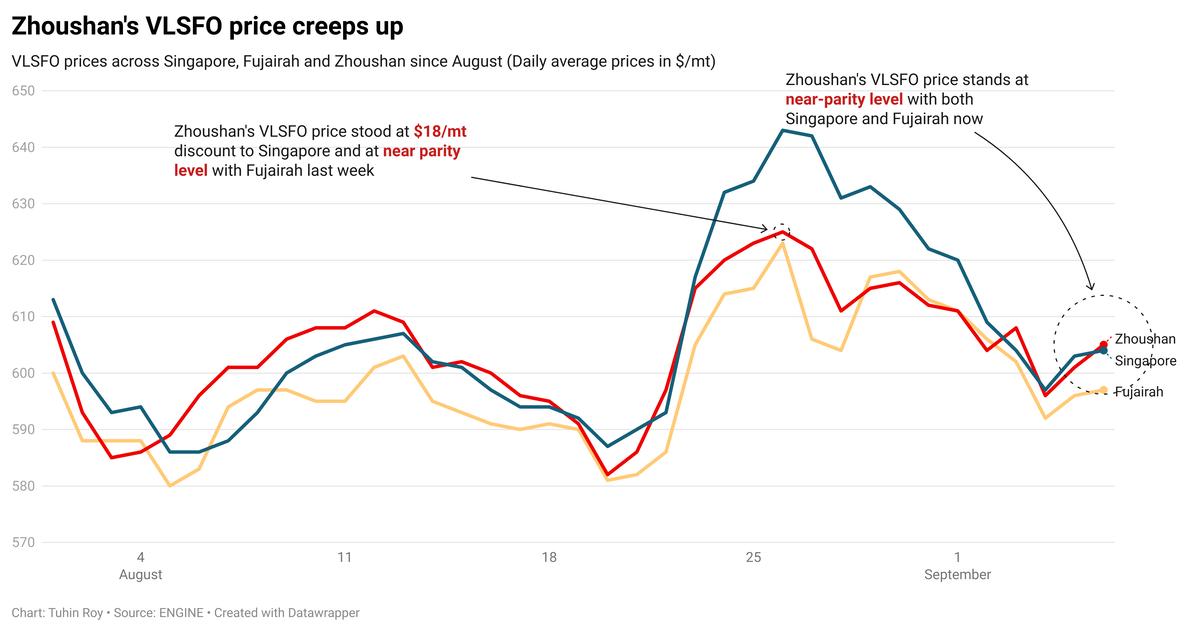

- VLSFO prices up in Zhoushan ($6/mt), Fujairah ($3/mt), and down in Singapore ($2/mt)

- LSMGO prices up in Fujairah ($2/mt), and down in Zhoushan ($7/mt) and Singapore ($6/mt)

- HSFO prices unchanged in Fujairah, and down in Singapore ($4/mt) and Zhoushan ($3/mt)

Zhoushan's VLSFO price has increased slightly by $6/mt over the past day, while prices in Fujairah and Singapore have remained mostly stable. A few higher-priced deals in Zhoushan, within a narrow range of $9/mt, have contributed to the benchmark's rise. As a result, Zhoushan's previous marginal discount to Singapore has disappeared and now stands at near-parity level. Zhoushan’s VLSFO price is now close to parity with Fujairah.

Despite weak bunker demand, prompt availability of all grades in Zhoushan has tightened, with most suppliers advising lead times of 5-7 days.

In southern South Korean ports, VLSFO and LSMGO availability remains tight, with many suppliers suggesting lead times of up to 11 days, though some can accommodate orders within as few as three days. HSFO availability has improved, with lead times dropping from around 11 days last week, to 4-6 days now.

In western South Korean ports, lead times for VLSFO and LSMGO grades have increased to 6-10 days from about seven days last week, while HSFO lead times have shortened to 3-5 days.

Brent

The front-month ICE Brent contract has moved $0.58/bbl lower on the day, to trade at $72.74/bbl at 17.00 SGT (09.00 GMT).

Upward pressure:

Brent’s price found some support after eight members of the Organization of the Petroleum Exporting Countries and its allies (OPEC+) collectively decided to postpone the gradual easing of production cuts that was scheduled to begin in October.

OPEC+ members, including Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria, Oman, and the UAE, have decided to extend the ongoing output cut of 2.2 million b/d for two more months. The group now plans to gradually unwind the production cuts beginning 1 December and continuing until November 2025.

“This [OPEC’s announcement] was not surprising, considering the pressure oil prices have been under in recent months,” ANZ Bank’s senior commodity strategist Daniel Hynes remarked.

On the demand side, Brent found some support after the US Energy Information Administration (EIA) reported a sizeable decline in crude inventories. Commercial crude oil inventories in the US dropped by 6.87 million bbls to touch 418 million bbls on 30 August, according to the EIA.

A drop in crude stocks is considered a positive indication of oil demand growth in the world’s largest oil consuming nation, according to market analysts. Yesterday’s EIA inventory report “was fairly constructive,” two analysts from ING Bank noted.

Downward pressure:

The global oil market’s sentiment is still negative as demand growth concerns from top oil consumers, China and the US, have outweighed any signs of supply tightness.

“Oil prices are giving into weak demand concerns out of China,” Price Futures Group’s senior market analyst Phil Flynn remarked.

Manufacturing Purchasing Managers' Index (PMI) readings in China and the US came in at 49.1% and 47.2% in August, respectively. A PMI reading below 50 indicates weak economic health and a contraction in the manufacturing sector. It also highlights demand growth concerns, ultimately weighing down on prices of commodities like oil.

Brent’s price has “taken a beating after breaking below key technical levels, with China demand concerns, weak global refinery margins,” analysts from Saxo Bank noted.

By Tuhin Roy and Aparupa Mazumder

Please get in touch with comments or additional info to news@engine.online

Provided by

Latest articles from the region

Contact our Experts

With 65+ traders in 13 offices around the world, our team is available 24/7 to support you in your energy procurement needs.